First-party collections are when the original creditor recovers unpaid debt under its own name. The work is handled by an internal team or by an outsourced partner that operates under the brand. It runs early in delinquency (typically days 1 to 120), protects the customer relationship, and is regulated mainly by TCPA, FCRA, and state laws, not the FDCPA.

Most finance leaders have a story about a collection agency that recovered the money and lost the customer. The calls were too aggressive, the tone was wrong, and the customer was lost.

That story is why first-party collections exist. The Federal Reserve Bank of New York reports that 3% of U.S. consumer debt moved into serious delinquency (90 or more days past due) in Q3 2025, up from 1.68% a year earlier. Most of it is still recoverable.

This guide covers the models, the vendors, and the right way to pick one.

Contents

- 1 How First-Party Collections Work

- 2 How to Pick the Right First-Party Collections Model

- 3 Two Compliance Rules Every First-Party Operation Needs to Know in 2026

- 4 Top 5 First-Party Collections Comparison at a Glance

- 5 The 5 Best First-Party Collections Companies for Finance Leaders in 2026

- 6 What to Look for in a First-Party Collections Platform

- 7 Why First Credit Services is Built for First-Party Collections at Scale

- 8 FAQs

- 8.1 1. How long does it take to implement a first-party collections program?

- 8.2 2. Do first-party collections affect a customer’s credit report?

- 8.3 3. Can first-party collections be used for B2B accounts?

- 8.4 4. What’s the difference between first-party collections and accounts receivable management?

- 8.5 5. How is the cost of first-party collections calculated?

- 8.6 6. Can first-party collections be combined with a third-party agency in the same program?

How First-Party Collections Work

First-party collections recovers unpaid debt under the creditor’s own brand using automated digital outreach, structured phone contact, and self-service payment options. The work moves through four phases tied to account age and recovery probability. The example below uses a 120-day window, which is common in retail finance and healthcare. Some creditors stop at 60 or 90 days; others extend to 180 days depending on industry, account value, and policy.

What a 120-Day First-Party Program Can Look Like

Days 1 to 30 (digital reminders): Outreach typically runs two to four touches per week across email, SMS, and in-app messages, with each reminder referencing the actual invoice number, due date, and balance. Recovery rates are highest in this window because most missed payments are accidental, caused by expired cards, billing emails routed to spam, or recent address changes.

Days 30 to 60 (structured outreach): Phone calls join the digital rotation, and agents offer concrete options including payment plans of 90 to 180 days, partial payments, autopay enrollment, and updated payment methods. TCPA call-time rules, Regulation F’s 7-in-7 limit, and stricter state caps like Massachusetts 940 CMR 7.04 become operationally binding in this phase.

Days 60 to 90 (full recovery push): Outreach is coordinated across every channel, and self-service portals handle the majority of conversions while live agents take disputes, hardship cases, and negotiations. Most accounts that will resolve at all resolve in this window, because recovery probability drops sharply after day 90.

Days 90 to 120 (escalation decision): Unresolved accounts get reviewed for one of three paths: continue first-party for high-value or relationship-sensitive accounts, hand to a third-party agency under FDCPA, or sell the portfolio.

Healthcare often extends to 180 days for patient balances, while subscription and BNPL businesses compress the timeline to 60 days because product access can be revoked sooner.

Picking the right operating model is what most finance teams get stuck on.

How to Pick the Right First-Party Collections Model

First-party collections run on one of three operating models, and the model decision comes before the vendor decision.

Managed Service (BPO)

The creditor outsources the entire collections operation to an external agency whose staff runs every call, email, and customer interaction under the creditor’s brand. It delivers a fully staffed collections function without hiring agents, buying software, or building a compliance program.

Best fit: finance teams without in-house collections, and mid-market or enterprise creditors with high volumes where brand consistency outweighs per-account cost.

Standalone Platform (SaaS)

The creditor licenses software and runs collections in-house, with the platform handling automation, routing, and reporting while internal staff manage every customer interaction. The creditor retains full control over data, scripts, and contact.

Best fit: organizations with an in-house collections team that needs better tooling, and creditors with the technical and regulatory capacity to run the operation themselves.

Hybrid

One partner delivers both the team and the platform as a product, not just an internal tool. The creditor’s collections team gets visibility into the platform’s workflows, reporting, and segmentation logic, in addition to the outsourced operations. The contract bundles staffing, platform access, and compliance into a single agreement.

Best fit: creditors that want outsourced agents and direct visibility into the platform running them, especially organizations transitioning from a purely manual or purely outsourced setup.

Three Questions That Settle the Choice

- Is there an in-house collections team worth keeping? If yes, a standalone platform gives existing staff better tools. If not, a managed service or hybrid brings the team along with the technology.

- Is brand consistency a board-level concern? If yes, rule out a pure platform, where in-house turnover erodes tone over time. A managed service or hybrid holds the brand more reliably.

- How exposed is the portfolio to state-level compliance enforcement? If California, Massachusetts, or New York consumers are in the mix, a managed service or hybrid model with built-in state compliance is the safer default. A standalone platform leaves the compliance burden on the in-house team, which is a real exposure given the Rosenthal Act and Massachusetts 940 CMR 7.04 reach into first-party operations.

Two Compliance Rules Every First-Party Operation Needs to Know in 2026

First-party operations touching California consumers or small business customers now face third party-level compliance exposure. California’s Rosenthal Act applies to original creditors, not just third-party agencies, and as of July 1, 2025, Senate Bill 1286 extended Rosenthal coverage to commercial debts of $500,000 or less owed by individuals or guarantors.

Massachusetts creditors making collections calls or texts are capped at two contacts per seven days. Under Massachusetts AG Regulation 940 CMR 7.04, creditors cannot initiate more than two phone or text communications in any seven-day period, which is stricter than Regulation F’s federal 7-in-7 rule.

Top 5 First-Party Collections Comparison at a Glance

The table below compares each vendor on the six factors that actually drive a first-party collections decision. Each entry below the table goes deeper into positioning, watchouts, and best fit.

| Vendor | Model | First-party + third-party in one contract | Proprietary platform | Self-service payment portal | Industry depth |

| First Credit Services | Hybrid | Yes | UCEP | Yes | Healthcare, financial services, auto finance, fintech, telecom, retail, utilities |

| InDebted (with Receeve) | Hybrid | Limited (digital focus) | Collect + Receeve | Yes | Fintech, BNPL, neobanks, digital lenders |

| TrueAccord | Hybrid (digital-led) | Yes (Retain + Recover) | HeartBeat | Yes | Consumer credit, lending, e-commerce, subscription |

| IC System | Managed | Yes | None (internal tools) | Limited | Healthcare, retail, education, government, telecom, utilities |

| Southwest Recovery Services | Managed | Yes | None | Limited | SMB across healthcare, property mgmt, retail, fintech |

The 5 Best First-Party Collections Companies for Finance Leaders in 2026

Now that the comparison is out of the way, here’s a closer look at how each vendor operates, where it leads, and where it falls short.

1. First Credit Services

First Credit Services is a hybrid BPO collection agency that recovers first-party and third-party debt under a single contract, powered by UCEP (Unified Consumer Engagement Platform), its in-house AI-driven engagement system.

Creditors get outsourced agent operations, an omnichannel engagement platform, and full state and federal compliance coverage from one vendor.

Key features

- UCEP, a proprietary AI-driven first-party engagement platform built and operated in-house

- First-party and third-party recovery delivered under a single contract and a single brand

- HIPAA-compliant healthcare revenue cycle management

- 30+ years of operational tenure across financial services, healthcare, fintech, auto finance, telecom, retail, and utilities

Pros

- One vendor for both first-party and third-party recovery

- Proprietary platform built specifically for first-party workflows

- Multi-industry compliance program covering FDCPA, Regulation F, TCPA, HIPAA, and state-level rules

Cons

- BPO-led model, so agent training and QA reviews carry more weight than in a SaaS-only setup

- Less suited for fully digital-native portfolios that want zero voice contact

Pricing: Custom, based on portfolio size, account age, and industry.

Best for: Mid-market and enterprise creditors in healthcare, financial services, fintech, auto finance, telecom, retail, and utilities that want outsourced execution paired with an AI platform under one contract.

Talk to a First Credit Services strategist to know more!.

2. InDebted (with Receeve)

InDebted is an enterprise hybrid collections partner that pairs AI-led managed services with a white-label first-party SaaS platform. Creditors can either outsource the operation through Collect or run first-party recovery in-house using Receeve, the platform InDebted acquired in December 2024.

Key features

- Two-product setup: Collect for AI-driven managed services and Receeve for in-house teams running their own first-party platform

- White-label SaaS option lets internal teams run first-party operations without contracting a managed service.

- Verified enterprise client base, including Klarna and Snap Finance

Pros

- Genuine hybrid offering with both BPO and SaaS layers

- Built natively for fintech and BNPL operating models

- Strong AI and ML segmentation across digital channels

Cons

- Voice-heavy legacy portfolios may find the platform under-tuned for that operating model.

- The US-based compliance footprint is newer than long-established US BPOs

Pricing: Custom enterprise pricing.

Best for: Enterprise fintech, BNPL providers, neobanks, and digital lenders.

3. TrueAccord

TrueAccord is a digital-first collections platform built around HeartBeat, its patented machine learning engine, which personalizes outreach timing, channel, content, and offer for every consumer in real time. Creditors get one of the highest self-service resolution rates in the category, along with built-in Regulation F compliance automation.

It operates two products: Retain for pre-charge-off first-party recovery and Recover for post-charge-off third-party collections.

Key features

- HeartBeat, a patented machine learning engine that personalizes outreach timing, channel, content, and offer in real time

- 20+ million consumer engagement journeys feeding the ML model

- “Code-based compliance” approach with built-in Regulation F automation

- Two-product split: Retain for pre-charge-off and Recover for post-charge-off

Pros

- Strongest ML-driven personalization in the category

- Very low overhead per account

- High self-service resolution rate

Cons

- Built for high-volume consumer portfolios, not high-touch B2B

- Voice-heavy operations sit outside the design

Pricing: Custom, with separate models for Retain and Recover.

Best for: Consumer credit, lending, e-commerce, and subscription businesses with high account volume.

4. IC System

IC System is a managed-service collection agency that recovers consumer and commercial debt under the creditor’s brand. Creditors get a long-running compliance and ethics record, broad US industry coverage, and a contingency-fee pricing model.

Key features

- BBB-accredited since 1992 with an A+ rating and repeated BBB Torch Award for Ethics recognition

- The broadest US industry footprint on this list, covering healthcare, retail, education, government, telecommunications, commercial, utility, and financial services

- Online client portal for account submission and status tracking

Pros

- One of the longest-tenured collection agencies in the US

- Strong ethics record and BBB standing

- Industry coverage spans both consumer and commercial sectors

Cons

- The technology stack is dependable, but not built to compete on AI or ML depth.

- Self-service payment options are limited compared to platform-led vendors

Pricing: Contingency-fee model.

Best for: Risk-averse mid-market and SMB creditors that prioritize tenure and ethics over technology depth.

5. Southwest Recovery Services

Southwest Recovery Services is a regional managed-service BPO that recovers debt across SMB and lower mid-market portfolios, with contingency-only pricing on every service line. Creditors get first-party, third-party, revenue cycle management, skip tracing, and asset location under one contract with no upfront cost.

Key features

- “No recovery, no fee” contingency-only pricing across every service line

- Service mix unusual for a regional BPO: first-party, third-party, revenue cycle management, skip tracing, and asset location under one roof

- Twelve regional offices across seven states with on-shore agents

Pros

- Contingency-only pricing removes upfront cost risk

- Hands-on regional partner relationship

- Broader service breadth than most regional agencies

Cons

- Smaller scale than national enterprise BPOs

- No proprietary first-party platform

- Limited fit for enterprise creditors with very large AR portfolios

Pricing: Contingency fee; no upfront cost.

Best for: SMB and lower mid-market creditors across healthcare, property management, retail, and fintech that want a regional partner.

The five vendors above approach first-party collections differently, which is exactly why a structured evaluation matters. Here’s what to actually look at when shortlisting.

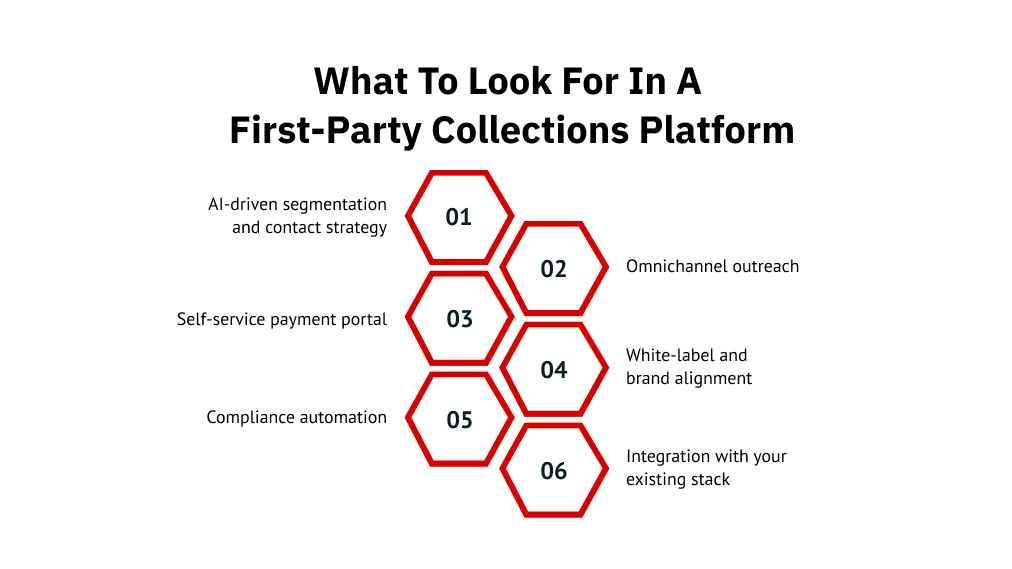

What to Look for in a First-Party Collections Platform

Picking a first-party collections vendor often comes down to a sales call. These six criteria help cut through that.

- AI-driven segmentation: The platform should pick contact timing, channel, and message using payment history, channel response rates, and time-of-day engagement, not a fixed cadence. Rule-based outreach burns 2x to 3x the touchpoints for the same recovery.

- Omnichannel outreach: Voice, SMS, email, IVR, mail, and self-service portal coordinated as one journey. Voice-only operations underperform because 80% of Americans don’t answer cellphone calls from unknown numbers, according to the Pew Research Center.

- Self-service payment portal: Customers should be able to pay any balance, set a payment plan, and accept a settlement 24/7 without an agent. Self-service costs roughly one-tenth of agent-assisted recovery and converts higher because customers prefer it.

- White-label and brand alignment: Email domain, caller ID, and payment portal subdomain all match the creditor’s brand. Lose any of the three, and first-party becomes third-party with extra steps.

- Compliance automation: Built-in guardrails for Regulation F’s 7-in-7 rule, TCPA consent windows (8 a.m. to 9 p.m. local), state caps (Massachusetts 2-in-7, California Rosenthal Act, NY DFS), and validation notice templates. TCPA settlements have crossed $75 million per case.

- Integration with the finance stack: Two-way sync with the AR system, billing, CRM, and ERP (NetSuite, SAP, Salesforce, HubSpot) via API, not SFTP exports. Set up under 30 days is healthy; over 60 days means the platform is bolted on.

Most vendors meet two or three of these. A handful meet four or five. First Credit Services is one of the few that builds all six into a single contract through UCEP, which is the practical case for evaluating it alongside any other shortlist vendor.

Why First Credit Services is Built for First-Party Collections at Scale

First-party collections in 2026 aren’t a single decision. It’s an operating model that has to hold up across regulatory shifts, channel preferences, and customer expectations that change every quarter.

First Credit Services brings 30+ years of running collections under regulated industries, an in-house platform built specifically for first-party workflows, and the operational discipline to stay current as Regulation F, state-level rules, and consumer behavior keep moving.

The question worth asking isn’t “which vendor is cheapest.” It’s “which vendor will still be the right fit when the regulatory floor shifts again.”

FAQs

1. How long does it take to implement a first-party collections program?

Managed-service programs typically launch in 30 to 60 days, covering agent training, system integration, and brand-alignment review. Platform-only deployments launch in 15 to 30 days if the in-house staff is already trained.

2. Do first-party collections affect a customer’s credit report?

Only if the original creditor reports the delinquency to a bureau. The first-party agency does not report separately. Reporting timing and method stay with the creditor.

3. Can first-party collections be used for B2B accounts?

Yes. B2B programs use longer recovery windows, higher-touch voice outreach, and account managers who handle disputes with the customer’s finance team. The brand-extension principle applies the same way.

4. What’s the difference between first-party collections and accounts receivable management?

Accounts receivable management covers the full AR lifecycle from invoicing to payment. First-party collections is one phase focused on recovering accounts aged 30 to 120 days past due.

5. How is the cost of first-party collections calculated?

Managed-service vendors charge a contingency fee, a percentage of what they recover. Platform vendors charge a SaaS subscription by account volume or seats. Hybrid vendors blend both based on portfolio size and account age.

6. Can first-party collections be combined with a third-party agency in the same program?

Yes. A single hybrid vendor can run both stages, so accounts transition without re-onboarding. This closes data gaps, keeps compliance consistent, and shortens the time between escalation and renewed outreach.