If your collection strategy still depends heavily on phone calls, a large part of your audience may never even pick up. Unknown numbers feel risky, calls are easy to ignore, and consumers now expect payment reminders to be as simple as the digital experiences they use every day.

That shift is hard to overlook. Google’s 2025 report found that 60% of Americans typically reject or ignore calls from unknown numbers, while 83% expect unknown callers to be scammers or telemarketers.

For businesses, this changes the recovery equation. Faster payment recovery still matters, but the way teams reach consumers matters just as much. A phone-only model can miss customers who would respond faster through SMS, email, chat, or a self-service payment portal.

Omnichannel debt collection addresses that gap by connecting every touchpoint into one coordinated recovery journey. It helps businesses use customer behavior, account status, consent, and delinquency stage to decide the right next step.

In this guide, we will look at how omnichannel debt collection works, how it differs from multichannel outreach, and how to build a strategy that improves recoveries while maintaining customer trust.

Contents

- 1 What is an Omnichannel Debt Collection?

- 2 What an Effective Omnichannel Debt Collection Model Looks Like

- 3 Compliance Guardrails for Omnichannel Debt Collection

- 4 Which Channel Works Best at Each Delinquency Stage

- 5 What Results Can Businesses Expect from Omnichannel Debt Collection?

- 6 Omnichannel ARM Strategy: What Businesses Need Before Implementation

- 7 Key Metrics to Track in Omnichannel Debt Collection

- 8 When Should You Move to an Omnichannel Debt Collection Partner?

- 9 Move from Outreach to Resolution

- 10 FAQs

- 10.1 1. Why are businesses moving toward omnichannel collections strategies?

- 10.2 2. How do consumers benefit from omnichannel debt collection?

- 10.3 3. What channels are commonly used in omnichannel debt collection?

- 10.4 4. Which delinquency stage benefits most from digital outreach?

- 10.5 5. How does AI improve omnichannel debt recovery?

- 10.6 6. Is omnichannel debt collection compliant with FDCPA and Regulation F?

What is an Omnichannel Debt Collection?

Omnichannel debt collection is a connected digital collections model. It brings SMS, email, voice, chat, IVR, and self-service portals into one coordinated recovery strategy.

Instead of sending the same reminders to every account, omnichannel outreach adjusts based on consumer behavior, consent, timing, and delinquency stage.

A customer who opens an email but does not pay may receive an SMS reminder next. If they start a payment plan, future outreach should reflect that progress. If they raise a dispute, the account should be moved to the correct workflow immediately.

That is what makes modern omnichannel debt recovery different from disconnected outreach. Every interaction becomes part of the same account history. Recovery teams get a clearer view of the consumer journey, while consumers get a smoother path to resolution without repeated or conflicting messages.

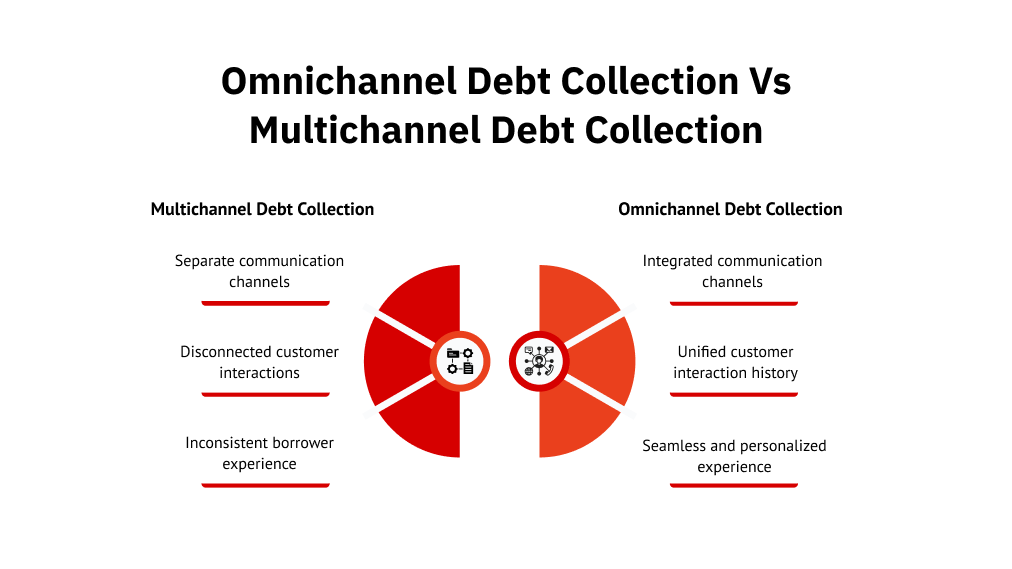

Omnichannel Debt Collection vs Multichannel Debt Collection

Multichannel debt collection uses several channels, such as phone, email, SMS, letters, and payment portals, but these channels often operate independently. The system may not connect what happened before or what should happen next.

Omnichannel debt collection connects every interaction into one recovery journey. For example, if a consumer ignores a call but clicks an SMS payment link, the system can pause unnecessary calls, send a payment-plan reminder, or route the account to an agent if the payment is not completed.

This matters because consumers want a clear path to resolution, not repeated messages across disconnected channels.

What an Effective Omnichannel Debt Collection Model Looks Like

An effective omnichannel debt collection model integrates data, outreach logic, payment access, compliance controls, and human support into a single workflow.

Without that connection, channels operate in silos, customers receive duplicate reminders, and agents lack context. A strong model prevents this by making every channel part of one recovery journey in the following ways:

1. Unified Consumer Data Across Channels

Omnichannel collections only work when consumer data is connected across payment status, contact preferences, communication history, consent records, disputes, promise-to-pay activity, and account notes.

When systems are disconnected, consumers may receive duplicate reminders, outdated balance information, or messages that do not reflect recent actions. Unified data eliminates these gaps by giving teams a shared view of each account and enabling more accurate, timely, and compliant outreach.

2. Behavioral Analytics and Next-Best-Channel Decisions

A mature omnichannel customer engagement collection model uses behavior to guide outreach.

If a consumer opens emails but pays only through SMS links, the system should prioritize SMS for payment nudges. If another consumer usually responds after work hours, the outreach sequence should reflect that pattern within compliant communication windows.

Channel preferences also vary by generation and message type. A 2025 SimpleTexting survey found that 61% of consumers preferred text messages for appointment confirmations, while 53% preferred email for customer service-related communication.

This matters in omnichannel payment recovery because not every customer wants the same type of communication. Behavioral analytics helps businesses move away from fixed call schedules and toward next-best-channel decisions based on actual engagement.

3. Stage-Based Outreach by Delinquency Age

The delinquency stage should shape the outreach strategy. Early-stage accounts often need simple reminders, payment links, and flexible self-service options. Later-stage accounts may require dispute handling, hardship conversations, settlement options, or agent support.

This is where FCS’s Unified Consumer Experience Platform (UCEP) model fits naturally. It supports engagement based on delinquency stage, response patterns, and customer behavior, helping FCS coordinate digital-first collections outreach and escalate to human support when needed.

4. Frictionless Payment Experiences

The best omnichannel debt collection model reduces the gap between communication and action.

If a consumer receives an SMS or email reminder, the payment link should take them directly to a secure, mobile-friendly portal where they can review the balance, choose a payment plan, make a payment, or accept a settlement offer.

Every extra step creates a drop-off. A smoother payment journey improves response rates, speeds up resolution, and makes repayment feel easier for the consumer.

Compliance Guardrails for Omnichannel Debt Collection

Omnichannel outreach gives businesses more ways to reach consumers, but it also increases compliance complexity.

Each channel must follow the right rules. Communication frequency, consent, disclosure language, dispute handling, opt-outs, and documentation must remain consistent across SMS, email, phone, chat, and portals.

That is why debt collection compliance cannot sit outside the omnichannel collections strategy. It must be built into the workflow from the start.

1. Fair Debt Collection Practices Act (FDCPA) and Regulation F Communication Rules

Omnichannel debt collection does not remove FDCPA or Regulation F obligations. It makes consistent controls more important across every channel.

Businesses need clear rules for when communication happens, what disclosures are required, how disputes are handled, and how consumer preferences are recorded. If a consumer disputes a debt via email, that update should flow into phone, SMS, chat, and portal workflows as well.

This matters even more when multiple teams or vendors are involved. Without shared controls, one channel may follow the right process while another creates compliance risk.

2. Telephone Consumer Protection Act (TCPA) and Consent for SMS Collections

SMS can be a powerful channel for early-stage collections, but it requires careful consent management and a clearly documented SMS policy.

Businesses should document how consent was captured, when SMS can be used, what messages can be sent, and how opt-outs are honored. If a consumer replies “STOP,” that preference should be updated across the entire communication workflow.

A compliant SMS strategy treats every text as a regulated communication, not just a quick reminder.

3. Audit Trails Across Every Interaction

Audit trails are essential in omnichannel debt recovery because every interaction can affect compliance, customer experience, and dispute resolution.

The Consumer Financial Protection Bureau’s 2025 report stated that it received approximately 207,800 debt collection complaints in 2024. This shows why accurate documentation matters.

In a managed model, platforms like FCS’s UCEP help coordinate outreach across channels while keeping activity aligned with FDCPA, Regulation F, TCPA, and other applicable compliance requirements. This gives businesses better control over both recovery performance and compliance risk.

Which Channel Works Best at Each Delinquency Stage

Not every channel works the same way across the collections lifecycle. A customer who is a few days late may only need a quick reminder, while a long-overdue account may require documentation, a payment discussion, or human support.

That is where omnichannel debt collection becomes useful. Instead of relying on a single method, businesses can match each channel to the customer’s delinquency stage, urgency level, and preferred way to respond. The goal is simple: make repayment easier without overwhelming the consumer.

1. SMS Collections

Best for: Early-stage delinquency, usually 1–30 days overdue

SMS works well when the consumer may have simply missed a payment. It is useful for payment reminders, due-date alerts, brief account updates, and secure payment links.

Because text messages are quick and convenient, SMS can help drive faster action before accounts move deeper into delinquency. However, businesses must carefully manage TCPA consent, opt-outs, and message frequency.

SMS should not operate as a standalone channel. It should connect with payment portals, email follow-ups, and account status updates to keep the consumer journey consistent.

2. Email Debt Recovery

Best for: Early to mid-stage delinquency, usually 15–60 days overdue

Email works better when the consumer needs more context. It gives businesses room to share account details, payment options, receipts, documentation, and settlement information.

It also gives consumers a written record, which is useful when they need to review the balance before taking action. Email pairs well with SMS because a text can prompt action, while an email provides the details needed to make a decision.

3. Voice and Digital Collections

Best for: Mid to late-stage delinquency, usually 45+ days overdue

Voice still plays an important role in omnichannel collections, especially when accounts move into more complex third-party collections workflows.

Phone conversations work well for disputed balances, hardship situations, high-value accounts, and complex repayment discussions.

In a modern collections model, voice should not be the default for every account. Digital outreach handles routine reminders and self-service payments, while agents focus on cases that require human support.

4. Chat and Self-Service Payment Portals

Best for: All delinquency stages, especially early and mid-stage accounts

Chat and self-service portals help consumers resolve accounts without calling an agent. A consumer can receive an SMS reminder, click a secure payment link, review the balance, choose a payment option, and complete repayment on their own.

This is especially valuable in white-labeled first-party collections. FCS supports this model by keeping the recovery experience under the client’s brand, so consumers do not feel like they have been handed off to a separate agency.

That brand continuity helps protect trust while making repayment simpler and more convenient.

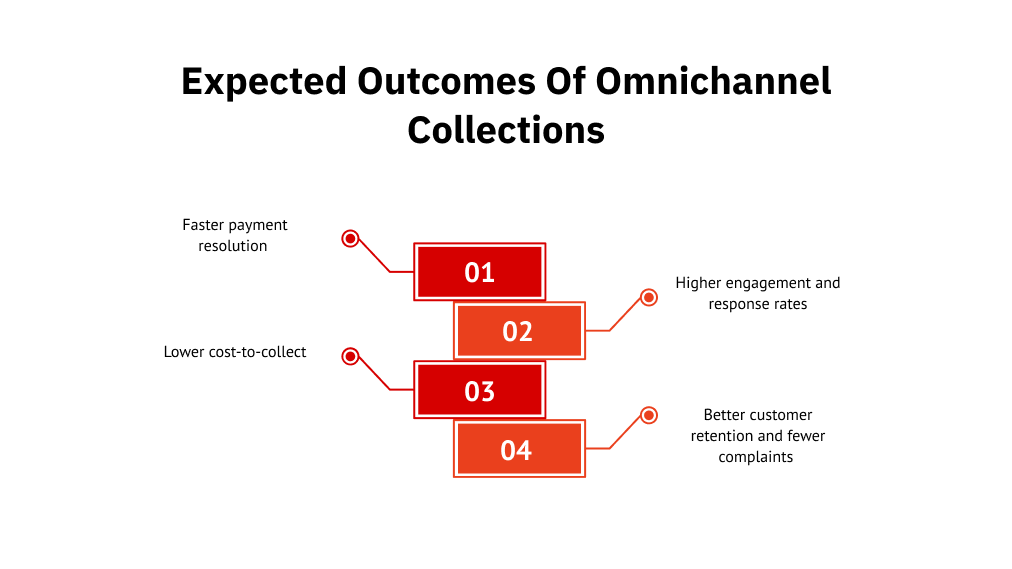

What Results Can Businesses Expect from Omnichannel Debt Collection?

Omnichannel debt collection should be measured by outcomes, not just the number of channels available. The real value is whether it improves recovery, reduces manual workload, and creates a better consumer experience.

When done well, omnichannel collections move teams from reactive follow-up to coordinated recovery, giving them better control over engagement, payment resolution, and compliance visibility.

1. Faster Payment Resolution

Omnichannel engagement reduces recovery delays by giving consumers a faster path to payment.

Instead of relying only on outbound calls, businesses can use SMS reminders, email follow-ups, secure payment links, chat, and self-service portals to make repayment easier. This matters because NMI 2026 research found that 52% of consumers prefer secure, one-click online checkout.

In early-stage delinquency, missed payments often come from forgetfulness, failed cards, or temporary cash-flow issues. A direct payment path here can speed up resolution and reduce unnecessary follow-ups.

2. Higher Engagement and Response Rates

Consumers respond differently across channels. Some prefer SMS, whereas others rely on email. Some need a phone call only when the account becomes more complex.

A coordinated omnichannel collections strategy adapts to these preferences instead of using the same sequence for every account. With behavioral analytics and AI-driven sequencing, teams can decide when to reach out, which channel to use, and what message to send. It helps improve response quality without increasing unnecessary outreach.

3. Lower Cost-to-Collect

Digital-first collections outreach helps reduce cost-to-collect by lowering dependency on agent-heavy workflows.

Self-service payments, automated reminders, AI-assisted prioritization, and digital portals allow teams to manage more accounts without increasing manual workload at the same pace. Agents can then focus on disputes, hardship cases, complex negotiations, and higher-risk accounts.

The WiFi Talents 2026 report states that automation can reduce the cost per dollar collected by 15%, while cloud migration can lower collection agency IT overhead by 30%. This shows why connected digital workflows can make recovery operations more scalable.

4. Better Customer Retention and Fewer Complaints

Collections can damage customer relationships when communication feels aggressive, repetitive, or disconnected. Omnichannel debt collection helps reduce that risk by making repayment easier, more relevant, and less intrusive.

This matters across the industries FCS serves, including healthcare, fintech, subscriptions, utilities, and financial services. In these sectors, recovery performance must be balanced with long-term trust.

White-labeled first-party engagement can support that balance by keeping the experience under the client’s brand while still using a structured recovery model.

5. How AI-Driven Sequencing Impacts Recovery Metrics

AI-driven sequencing helps collections teams adjust outreach based on engagement behavior, payment history, channel response, and delinquency stage.

If a consumer responds better to SMS than email, the system can prioritize SMS reminders. If another consumer needs more detail, email may become a stronger channel.

FCS’s UCEP applies this adaptive outreach by coordinating digital engagement, self-service payments, and human escalation. This creates a more responsive omnichannel payment recovery strategy.

Omnichannel ARM Strategy: What Businesses Need Before Implementation

An omnichannel ARM strategy requires more than communication tools. Businesses need connected data, clear governance, consent controls, segmentation rules, and enough execution capacity to manage outreach consistently.

Without these foundations, adding more channels can create more confusion instead of better recovery.

1. Connected CRM, Billing, and Payment Systems

Omnichannel ARM depends on timely data from CRM systems, billing platforms, payment gateways, and servicing tools.

When these systems are disconnected, teams may contact consumers after payment, send duplicate reminders, or miss key account updates. A connected data layer helps outreach reflect the real account status and gives teams a clearer view of every interaction.

2. Channel Governance and Consent Management

Businesses need clear rules for how each channel is used. This includes when SMS, email, voice, or chat can be used, how opt-outs are handled, how communication limits are enforced, and which disclosures are required.

Consent should not sit in a disconnected spreadsheet. It should be part of the workflow, so every outreach decision reflects the consumer’s current preferences and reduces compliance risk.

3. Segmentation Rules and AI Decisioning

Segmentation helps teams match the right outreach strategy to the right account.

Businesses should segment accounts by delinquency age, balance size, risk level, channel preference, payment history, prior engagement, and dispute status. AI can strengthen these decisions, but only when the data and recovery strategy are clear.

For example, a low-balance early-stage account may be best suited for SMS and self-service, while a high-value disputed account may need agent review.

4. Internal Execution vs Managed Omnichannel Recovery

Software can support omnichannel workflows. However, businesses still need the bandwidth to manage integrations, campaign logic, compliance rules, reporting, disputes, payment follow-ups, and channel optimization.

This is where managed debt collection services can help. FCS combines UCEP, digital engagement, first-party recovery, and execution support within a unified model.

FCS manages the platform, outreach logic, communication flow, and recovery execution on the client’s behalf. This gives businesses the benefits of omnichannel recovery without requiring their internal teams to run another system.

Key Metrics to Track in Omnichannel Debt Collection

Measurement shows whether omnichannel collections are improving recovery, customer experience, and compliance outcomes. Instead of only tracking messages sent, businesses should measure whether outreach helps consumers respond, pay, dispute, or resolve accounts faster.

1. Recovery Performance Metrics

These metrics show whether the omnichannel collections strategy is improving payment outcomes:

- Payment resolution rate

- Response rate by channel

- Promise-to-pay conversion rate

- Right-party contact rate

- Payment-plan completion rate

- Cost-to-collect

- Average days to resolution

- Self-service payment completion rate

Track these metrics by channel and delinquency stage. The goal is not to declare one channel the winner. It is to understand which channel works best in each account context.

2. Experience and Compliance Metrics

Omnichannel collections should also improve consumer experience and reduce compliance risk. Useful metrics include:

- Complaint rate

- Dispute rate

- Opt-out rate

- Repeat contact rate

- Customer satisfaction

- Time to resolve disputes

- Compliance adherence by channel

- Documentation completeness

These metrics help businesses understand whether outreach remains respectful, consumer-friendly, and compliant.

When Should You Move to an Omnichannel Debt Collection Partner?

At some point, improving collections is no longer just about adding another tool. It becomes a question of whether your team has the structure, visibility, and execution support to consistently manage recovery.

A managed debt collection partner may make sense when:

- Phone-heavy outreach is no longer working because consumers are ignoring calls but responding to SMS, email, or self-service portals.

- Internal teams are stretched across digital outreach, reporting, compliance controls, and follow-ups.

- Compliance risk is increasing because opt-outs, consent records, documentation, and communication rules are hard to track.

- Customer experience is becoming a recovery issue, driven by complaints, damaged trust, and increased churn.

Move from Outreach to Resolution

A stronger collections strategy does not simply contact customers more often. It removes the friction that slows repayment, gives teams clearer visibility into each account, and uses digital channels with purpose.

For businesses, that means fewer disconnected follow-ups, better use of agent time, and a recovery experience that feels easier for customers to act on. The next step is to choose a model that can support both performance and compliance as account volumes grow.

Want to know how FCS can turn disconnected outreach into measurable recovery outcomes?

FAQs

1. Why are businesses moving toward omnichannel collections strategies?

Because phone-only outreach is less effective. Omnichannel collections help businesses reach consumers through preferred channels, reduce manual follow-ups, and improve recovery experiences.

2. How do consumers benefit from omnichannel debt collection?

Consumers get easier ways to resolve missed payments through preferred channels, secure payment links, repayment options, and fewer repeated conversations.

3. What channels are commonly used in omnichannel debt collection?

Common channels include phone, SMS, email, chat, IVR, self-service portals, WhatsApp, and mobile apps. The best strategies connect them into one coordinated journey.

4. Which delinquency stage benefits most from digital outreach?

Early-stage delinquency, usually 1–30 days overdue, benefits most. SMS, email, and payment links can help consumers resolve missed payments quickly.

5. How does AI improve omnichannel debt recovery?

AI helps prioritize accounts, choose the right channel, personalize messages, and predict repayment behavior based on engagement patterns and delinquency stage.

6. Is omnichannel debt collection compliant with FDCPA and Regulation F?

Yes, when proper controls are in place. Businesses need consent tracking, communication rules, disclosures, dispute workflows, opt-out handling, and audit trails across channels.