Loan delinquency management is how lenders identify overdue accounts, reach borrowers, offer repayment options, and recover missed payments before a loan defaults. It runs across the full loan lifecycle, from preventing a miss to recovering the balance after one happens.

A missed payment is not yet a default, but the longer an account ages, the lower the odds of recovery. At the start of 2026, 4.8% of outstanding consumer debt was in some stage of delinquency, according to the Federal Reserve Bank of New York Household Debt and Credit Report Q1 2026. Every account in that pool will either cure or charge off, and how a lender works its book decides the split.

This guide is for lenders and loan servicers. By the end, you will know the full process, the metrics that prove it works, and the call most get wrong: build it in-house, buy software, or outsource.

Contents

- 1 What Is Loan Delinquency Management, and Where Does It Sit in the Loan Lifecycle?

- 2 Why Do Loans Go Delinquent, and How Do You Prevent It?

- 3 How Does the Loan Delinquency Management Process Work, Stage by Stage?

- 4 Should You Run Delinquency Management In-House or Outsource It?

- 5 Which Metrics Show Loan Delinquency Management Is Working?

- 6 How Does First Credit Services Handle Loan Delinquency Management?

- 7 Get Loan Delinquency Management Right Before Accounts Roll

- 8 FAQs

- 8.1 1. How is an outsourced loan delinquency management program priced?

- 8.2 2. How long does it take to stand up an outsourced delinquency program?

- 8.3 3. Does outsourcing delinquency management hurt the borrower relationship?

- 8.4 4. At what stage should a lender bring in a delinquency management partner?

- 8.5 5. Can a delinquency management partner integrate with our loan servicing system?

- 8.6 6. Does delinquency management affect credit bureau reporting?

What Is Loan Delinquency Management, and Where Does It Sit in the Loan Lifecycle?

Loan delinquency management is the set of processes a lender uses to identify overdue accounts, communicate with borrowers, offer repayment options, and recover missed payments before a loan moves into default. The discipline covers the whole arc of a troubled account, from the first reminder that heads off a miss to the recovery work that follows a charge-off.

That makes it broader than collections. Collections is the recovery tail, the work that starts once an account is already past due. Delinquency management includes that tail, but it also includes the reminder that stops the miss, the segmentation that decides who to call first, and the workout that keeps a hardship borrower paying. It is a system and a strategy working together. Hold that distinction. It is the seed of the build-versus-outsource decision later in this guide.

The delinquency lifecycle and DPD buckets

Loan servicing teams track delinquency in days past due, or DPD. An account moves through buckets as it ages, and the action and the recovery odds change at each one.

| Bucket (DPD) | Account status | Typical action | Recovery odds |

| Current | Performing | Pre-due reminders, autopay | Highest |

| 1 to 29 | Early delinquent | Fast, low-friction outreach; cure | High |

| 30 to 59 | Delinquent | Multi-channel contact, payment plans | Moderate |

| 60 to 89 | Seriously delinquent | Workout offers, hardship programs | Lower |

| 90+ | Pre-charge-off | Escalation, restructuring, recovery | Low |

| Charge-off | Written off | Third-party or post-charge-off recovery | Lowest |

The number that ties this table together is the roll rate. Roll rate is the share of accounts that slide from one bucket into the next. A 30-to-60 roll rate tells you how many 30-day accounts you failed to cure before they aged a month. Recovery odds fall at every step down the table, so the cheapest dollar you recover is the one you stop from rolling in the first place.

Why Do Loans Go Delinquent, and How Do You Prevent It?

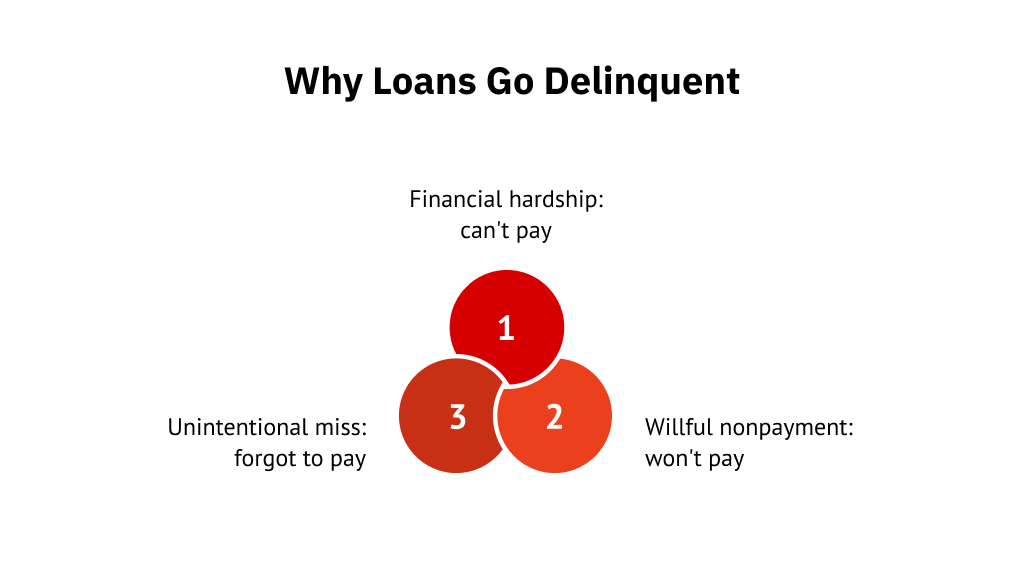

Loans go delinquent for three reasons, and the reason should set the response.

- Financial hardship. The borrower wants to pay but cannot, because of job loss, a medical event, or an income shock. This borrower needs a workout offer to get back on track.

- Willful nonpayment. The borrower can pay but is not prioritizing the obligation. This account needs structured, consistent follow-up.

- Unintentional misses. The borrower simply forgot, used an expired card, hit a non-sufficient-funds (NSF) return, or changed bank accounts. This is the cheapest delinquency to avoid, and the most common.

Prevention works on that third group before an account is ever late. A repayment reminder strategy is the lever. Pre-due-date reminders across text, email, and in-app messaging catch the expired card and the forgotten due date while the fix still takes one tap. Reaching a borrower the day before a payment is due costs a fraction of working the same account at 45 days past due.

Two more levers sit upstream of the reminder.

- Autopay and ACH (automated clearing house) enrollment at origination. Every account on autopay is one fewer account that can miss by accident. Enrollment is easiest to win at funding, while the borrower is still in your flow and before any miss happens.

- Affordability at origination. Payment-to-income checks and loan terms that do not stretch the borrower are prevention before the loan even funds. A payment a borrower can absorb is a payment that does not roll.

| Pro tipTreat unintentional misses as an operations problem and solve them with automation before a collector is ever involved. If a meaningful share of your 1-to-29 bucket clears on the first reminder, that volume should never reach a collector. Route it to automated pre-due and day-of reminders, and reserve human contact for accounts that do not self-cure. |

How Does the Loan Delinquency Management Process Work, Stage by Stage?

Once an account misses, the process moves through five stages. The goal at every stage is the same: resolve the balance and keep the borrower relationship intact.

1. Early intervention in the first days after a miss

The first contact window is short, and it matters more than any other. Reaching a borrower within days of a miss, before the account ages, lifts cure rates sharply. Speed and a clear next step beat volume of contact. One well-timed message with a one-tap path to pay does more than five aggressive calls a week later.

2. Risk segmentation and predictive scoring

Delinquent accounts vary widely in how much effort they justify. Segment the book by balance, behavior, and risk score so work lands where it pays off. Predictive scoring, driven by analytics on past payment behavior, flags the accounts most likely to roll into the next bucket. That lets agents work the highest-risk queue first and pick the right channel for each profile, instead of dialing the list top to bottom.

3. Omnichannel borrower outreach

Borrowers do not all answer the phone, and phone-only outreach forfeits curable accounts. Meet them across text, email, voice, and a self-service portal. This is where borrower delinquency management is won or lost.

- Match cadence and channel to how the borrower actually engages. A borrower who pays through a portal at 11 pm should not be getting daytime calls.

- Document consent for each channel. Channel choice is also a compliance choice, covered below.

- Give every message a direct path to resolve, so an engaged borrower never has to hunt for how to pay.

4. Repayment flexibility

Most curable accounts cure because the lender offered a realistic way to pay. Promise-to-pay arrangements, payment plans, restructuring, and hardship options turn at-risk accounts into performing ones.

Take a $1,200 auto-loan arrears spread over four months: structured, it becomes a paying account; demanded in full, it becomes a charge-off. Transparency about the options is what gets a hardship borrower to pick up and engage rather than avoid.

5. Escalation and charge-off handling

When cures fail, the account moves to structured escalation: firmer, documented outreach, then delinquent loan recovery, and, if it still cannot be resolved, charge-off. Loan default management does not end there. Post-charge-off recovery continues, often through a third-party agency working aged balances. Every step gets logged for audit, so the full history of contact and offers is defensible.

Should You Run Delinquency Management In-House or Outsource It?

This is the decision most guides skip, and it is the one that actually shapes your roll rates and your cost to collect.

What software does, and what it leaves to you

A loan delinquency management system earns its keep. It tracks DPD buckets, automates reminders, logs every contact, and gives you a dashboard. That is the system layer, and it is necessary.

Software does not collect, however. It does not make the judgment calls on a hardship file, work a dispute, staff a Saturday evening queue, or carry the compliance maturity that comes from auditing thousands of live calls. A platform runs the workflow. The collecting still depends on people, process, and channel execution. Buying software solves the tracking problem and leaves the staffing and execution problem entirely with you.

Build, buy software, or outsource

There are three honest paths, and the right one depends on your volume, your bandwidth, and your compliance exposure.

| Factor | Build in-house | License software | Outsource to a managed partner |

| Upfront cost | High (hiring, tooling, training) | Moderate (license plus your staff) | Low (often contingency-based) |

| Time to value | Slow | Fast if you already have collectors | Fast, the partner is already staffed |

| Compliance burden | You own all of it | You own all of it | Shared; partner carries execution risk |

| Scale and coverage | Limited by your headcount | Limited by your headcount | High, including nights and overflow |

| Control and oversight | Highest, fully direct | High, you run the floor | Lower, you supervise a vendor |

| Who carries execution risk | You | You | The partner |

No path wins every row. Building in-house gives you the most control and direct oversight, which matters if delinquency handling is core to how you compete. Licensing software is the fastest route for a team that already has skilled collectors and just needs the system layer.

Outsourcing shifts staffing and execution off your plate and scales without new hires, but you give up some direct oversight, and you pay a per-recovery cost. If control is your top priority and you have the people, in-house or software is the stronger call. Be honest about which one you actually are.

When outsourcing makes sense

Outsourcing earns its place under a specific set of conditions:

- High account volume that your internal team cannot work within the first-contact window.

- Thin internal bandwidth, where every collector hour is already spent.

- Heavy compliance exposure that is cheaper to rent than to build.

- A need for omnichannel and around-the-clock coverage you do not want to stand up yourself.

One nuance most lenders miss: an outsourced partner can run early-stage work under your brand, so the outreach reads as first-party to the borrower. Done well, the borrower never knows a third party is involved, and the relationship stays yours.

Which Metrics Show Loan Delinquency Management Is Working?

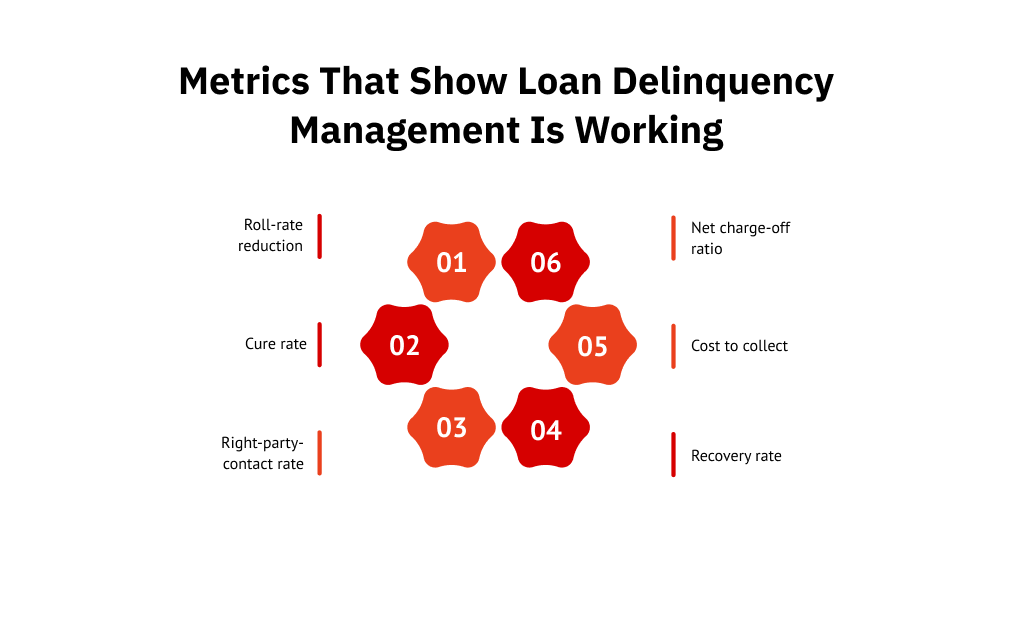

A delinquency program proves itself in numbers, whichever path you choose. Track these and lead with the first one.

- Roll-rate reduction. The share of accounts sliding from one bucket to the next. A program that quietly keeps accounts out of the 60-plus bucket is doing its most valuable work upstream, often before any of it shows up in a recovery report. Watch this first.

- Cure rate. The share of delinquent accounts brought current. It tells you whether your early-stage work is actually resolving accounts.

- Right-party-contact rate. How often you reach the actual borrower rather than a voicemail or a wrong number. Weak contact rates cap every downstream metric.

- Recovery rate. Dollars recovered against dollars owed. The headline outcome, but a lagging one.

- Cost to collect. What you spend to recover a dollar. The number that decides whether a path is sustainable.

- Net charge-off ratio. Balances written off, net of recoveries, against the portfolio. The bottom-line measure of leakage.

Benchmark your book against loan-type norms. At the start of 2026, credit card balances flowed into serious delinquency at roughly 7.1% a year and auto loans at roughly 3.0%, according to the Federal Reserve Bank of New York Household Debt and Credit Report Q1 2026. If your roll rates run well above the norm for your product, that gap is the opportunity your delinquency program exists to close.

Roll-rate reduction usually moves first. Recovery dollars catch up later. If you wait for the recovery report to tell you the program is working, you are reading the slowest signal on the dashboard.

These numbers also expose a ceiling. If your roll rates stay stuck despite the effort, the limit is usually capacity or channel reach. That is when the build-versus-outsource decision stops being theoretical. Many lenders look hardest at a managed partner right when the metrics plateau.

How Does First Credit Services Handle Loan Delinquency Management?

If the build-versus-outsource math points you toward a partner, this is where First Credit Services fits. First Credit Services runs delinquency management as a fully managed service that its own team operates end to end. It covers the full lifecycle, from first-party collections handled fully white-label under your brand, through to third-party collections on aged accounts. The borrower experience stays entirely under your brand. Pricing is contingency based, so you pay when First Credit Services collects.

The contact strategy runs on UCEP, the Unified Consumer Engagement Platform. UCEP is an omnichannel, AI-driven engagement platform that scores each account and picks the message, channel, and time most likely to resolve it, with a self-service payment portal where borrowers can set up plans and pay in one tap. It sits inside the managed service, run by First Credit Services rather than licensed to you, with reporting and dashboards shared back to your team. You can see how the digital collections platform works in practice.

The model is built for lenders across auto finance, consumer and credit-card lending, fintech, banks, and credit unions, the industries First Credit Services serves.

Get Loan Delinquency Management Right Before Accounts Roll

The economics of delinquency are simple. It is cheapest to prevent, next cheapest to fix early, and most expensive once an account has rolled into the deep buckets. The work is deliberate and systematic: prevent the unintentional miss, intervene in the first days, segment by risk, meet borrowers where they engage, offer a real way to pay, and document every step.

That leaves one real choice. Build the execution in-house, buy software and staff it yourself, or hand it to a partner who is already set up to run it under your brand. The right answer depends on your volume, your bandwidth, and your compliance exposure, and it shows up first in your roll rates.

Want to lower your roll rates without building a collections floor? Talk to First Credit Services about what a managed, first-party delinquency program built on UCEP would look like for your portfolio. You pay only when First Credit Services collects, and your borrowers stay yours.

FAQs

1. How is an outsourced loan delinquency management program priced?

Many managed partners, including First Credit Services, work on a contingency model: you pay a percentage of what is recovered, with no upfront fee. That ties the partner’s revenue to your results and keeps fixed costs off your books.

2. How long does it take to stand up an outsourced delinquency program?

Faster than building in-house, because the partner is already staffed and compliant. Timelines depend on data integration and workflow setup, but a managed partner can typically deploy trained agents and mirror your systems within a few weeks.

3. Does outsourcing delinquency management hurt the borrower relationship?

It does not have to. First-party, white-label outreach runs under your brand, so the borrower experiences it as contact from you. Done with empathetic, compliant messaging, early-stage outreach can preserve the relationship rather than strain it.

4. At what stage should a lender bring in a delinquency management partner?

There is no single rule, but earlier is usually better. Partners that handle early-stage, first-party work engage while cure odds are highest. Waiting until accounts are deep in the 90-plus bucket forfeits the most recoverable dollars.

5. Can a delinquency management partner integrate with our loan servicing system?

Yes. A capable partner connects to your servicing platform, CRM, and payment systems so account status, contacts, and payments stay in sync. Confirm integration method and reporting cadence during evaluation, since data flow drives both speed and compliance.

6. Does delinquency management affect credit bureau reporting?

Reporting obligations stay with the furnisher of record and are governed by accuracy rules. A delinquency program does not change what must be reported, but resolving accounts before charge-off can change what ends up on the borrower’s file. Confirm reporting responsibilities with counsel.