Early delinquency is the point where businesses still have options.

The account is overdue, but the customer may still respond, pay, ask a billing question, or agree to a payment plan. But that window closes quickly.

The New York Fed’s Q3 2025 report found that 4.5% of outstanding U.S. consumer debt was in some stage of delinquency, with transitions into early delinquency increasing for credit cards. For high-volume businesses, that means longer follow-up queues, higher roll-rate risk, and more pressure on recovery teams.

Most early delinquencies are still recoverable. They become harder to resolve when outreach starts late, uses the wrong channel, or sends the same generic message to every account.

Early-stage debt collection helps businesses intervene sooner with timely reminders, account segmentation, digital payment options, dispute routing, and soft collections.

This guide explains what early-stage debt collection is, how it works, and how to measure performance.

Contents

- 1 What is Early-Stage Debt Collection?

- 2 Early-Stage vs. Mid-Stage vs. Late-Stage Collections

- 3 Why Early-Stage Collections Yield Higher Recovery Rates

- 4 The Most Common Reasons Early-Stage Collections Fail

- 5 How Early-Stage Debt Collection Works: The Core Workflow

- 6 First-Party vs. Third-Party Early-Stage Collections

- 7 Compliance Considerations in Early-Stage Collections

- 7.1 FDCPA at the Early Stage

- 7.2 Regulation F and Digital Communication

- 7.3 Industry-Specific Compliance Layers

- 7.4 How to Measure Early-Stage Collection Performance

- 7.5 1. Roll-Rate Reduction

- 7.6 2. Early Cure Rate

- 7.7 3. Promise-to-Pay Completion Rate

- 7.8 4. Channel Response Rate

- 7.9 5. Cost Per Recovered Dollar

- 7.10 6. Escalation Prevention Rate

- 8 When to Outsource Early-Stage Collections?

- 9 Act Earlier While Accounts are Still Recoverable

- 10 FAQs

- 10.1 1. How is early-stage debt collection different from pre-collection services?

- 10.2 2. Why do recovery rates decline as accounts age?

- 10.3 3. What industries use early-stage debt collection most?

- 10.4 4. What channels work best for early delinquency outreach?

- 10.5 5. What compliance rules apply to early-stage debt collection?

- 10.6 6. How do businesses know if their early-stage collections program is working?

What is Early-Stage Debt Collection?

Early-stage debt collection is recovery outreach for recently overdue accounts. It usually happens within the first 1 to 90 days past due, before charge-off or third-party escalation.

The focus is not on aggressive recovery but on account resolution. Early-stage collection services use payment reminders, digital payment options, payment-plan offers, dispute routing, and customer-friendly collections. These tools help customers resolve balances while the account is still fresh.

How Early-Stage Fits into the Broader Collections Lifecycle

Early-stage debt collection sits inside a larger delinquency lifecycle:

| Pre-delinquency → early stage collections → mid-stage collections → late-stage collections → charge-off → third-party placement |

This sequence matters because recovery difficulty, cost, and customer responsiveness change as accounts age. A customer who is 10 days past due may need a reminder or a payment link.

On the contrary, a customer who is 90 days past due may require stronger documentation, escalated outreach, and a different recovery strategy. The early stage is where intervention is usually least expensive and most likely to preserve the customer relationship.

Early-Stage vs. Mid-Stage vs. Late-Stage Collections

The approach to collections changes significantly depending on how far an account has aged, such as:

| Stage | Days Past Due (DPD) Range | Primary Goal | Typical Approach | Recovery Difficulty |

| Pre-delinquency | 0 DPD | Prevention | Due-date reminders, payment nudges | Very low |

| Early stage | 1 to 30 DPD | Soft resolution | Omnichannel outreach, payment links, dispute capture | Low |

| Mid stage | 30 to 60 DPD | Account retention | Escalated follow-up, payment plans, stronger messaging | Moderate |

| Late stage | 60 to 90+ DPD | Pre-charge-off recovery | Intensive outreach, pre-charge-off review | High |

| Charge-off or third-party | 90 to 180+ DPD | Maximum recovery | Third-party placement, legal review where applicable | Very high |

The key window is usually between the due date and the first 60 days past due. This is when the effort-to-return ratio is strongest. After that, the customer may be harder to reach, disputes may be harder to validate, and more accounts may need formal escalation.

The right collection strategy should match the account’s stage. Treating accounts too aggressively can damage relationships, while treating serious delinquencies too lightly can weaken recovery.

Why Early-Stage Collections Yield Higher Recovery Rates

Early intervention works because most early delinquencies are still fixable. Here’s why:

Most Early Delinquencies Are Caused by Friction, Not Refusal

Many accounts go past due because of an expired card, a missed reminder, a billing question, a failed autopay, or a short-term cash flow issue.

That distinction matters.

A customer who forgot to update a payment method needs a payment update link. A customer who does not understand a balance needs clarification. A customer facing temporary financial pressure may need a payment plan. Treating all three as unwilling-to-pay accounts creates unnecessary friction.

Early intervention collections work best when outreach helps identify the reason behind non-payment and routes the customer to the right next step.

The Financial Case is Straightforward

The longer an account sits unresolved, the more expensive it becomes to manage.

The PYMNTS’ 2025 report mentions that 81% of businesses need to contact a customer between one and four times just to collect on a single overdue invoice. That shows how quickly late payments can turn into repeated follow-ups, manual effort, and operational strain.

That points to a common operational issue: many late payments are not only customer problems. They are process problems.

Early-stage delinquency management helps businesses reduce that gap by creating a repeatable workflow for outreach, resolution, and escalation.

Early Resolution Protects the Customer Relationship

In many industries, the debtor is also an active customer. That is true in healthcare, fitness, consumer lending, utilities, subscriptions, and auto finance.

Early stage outreach should feel like service, not pressure. The tone should be clear, professional, and easy to act on. When handled well, early account recovery gives the customer a way to resolve the issue without feeling pushed into a collections experience too soon.

The Most Common Reasons Early-Stage Collections Fail

Early-stage collections usually fail for operational reasons, not because the concept is weak. The challenges show up in the following common ways:

1. Outreach Starts Too Late

Internal AR teams often wait too long before the first meaningful follow-up. In some businesses, accounts reach 45 to 60 days past due before outreach becomes consistent.

By that point, the simplest resolution window may already be gone. The customer may no longer remember the bill clearly, may have ignored multiple statements, or may have moved from temporary delay into deeper delinquency.

2. Phone-Only Contact Limits Reach

Phone calls still matter, but they cannot be the only strategy.

Many customers do not answer unknown numbers. Others prefer text, email, chat, or portal-based resolution. If the phone is the only channel, unreachable customers may keep aging even when they would have responded to a different contact method.

3. No Account Segmentation

A first missed payment at 8 days past due should not follow the same workflow as a repeat delinquency at 55 days past due.

Segmentation should consider:

- Days past due

- Balance size

- Account history

- Prior payment behavior

- Previous disputes

- Channel engagement

- Risk of escalation

Without segmentation, outreach becomes generic. Generic outreach wastes effort on low-risk accounts and misses high-risk accounts that need faster intervention.

4. Payment Friction Goes Unresolved

A customer may be willing to pay but still fail to complete payment because the process is difficult.

Common blockers include:

- Expired cards

- Broken payment links

- Unclear invoices

- No mobile payment option

- No payment-plan path

- Long hold times for agent support

- Unresolved billing questions

Early-stage debt collection should remove friction, not only remind customers that a balance exists.

5. Internal Teams Lack Consistent Bandwidth

High account volume makes manual follow-up difficult.

Even strong AR teams can fall behind when they are managing disputes, inbound calls, payment promises, reporting, and repeated follow-ups simultaneously. Early-stage collections require consistency, and that is often where internal teams feel the most pressure.

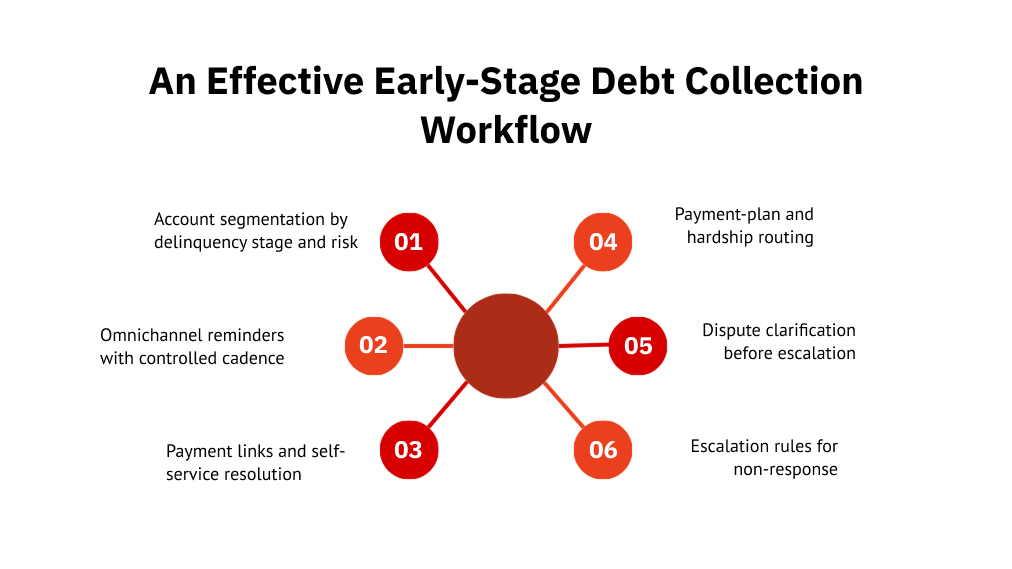

How Early-Stage Debt Collection Works: The Core Workflow

Early-stage collection services work best when they follow a defined workflow from account intake to resolution or escalation. Here’s what the process looks like:

1. Account Segmentation by Risk and Delinquency Stage

Before outreach begins, accounts should be grouped by risk and likelihood of resolution.

A strong segmentation model looks at:

- Days past due

- Balance size

- Payment history

- Customer type

- Prior response behavior

- Dispute status

- Preferred channel

- Previous payment-plan activity

This segmentation guides the cadence, tone, channel mix, and resolution option. A low-balance first miss may need a light-touch reminder. On the other hand, a repeat delinquency with prior broken promises may need faster escalation.

2. Structured Omnichannel Outreach Cadence

Early-stage collections should coordinate SMS, email, phone, chat, and digital portals. These channels should not operate as disconnected reminders.

A strong cadence may look like this:

| Timing | Outreach Example |

| Before due date | Payment reminder or autopay confirmation |

| 1 to 7 DPD | Email or SMS with payment link |

| 8 to 15 DPD | Follow-up reminder with self-service options |

| 16 to 30 DPD | Agent-assisted outreach or payment-plan |

| 31 to 60 DPD | Stronger follow-up and dispute review |

| 60+ DPD | Pre-charge-off recovery or escalation review |

For instance, platforms such as FCS’s Unified Consumer Experience Platform (UCEP) support AI-driven, omnichannel early-stage workflows as a managed service for high-volume AR operations.

This helps businesses move from scattered reminders to a coordinated recovery workflow where every outreach step has a clear purpose, channel, and next action.

3. Self-Service Payment and Digital Resolution Tools

Early-stage collection should make resolution easy. Hence, customers should be able to:

- Pay in full

- Update expired payment details

- Accept a payment plan

- Confirm a promise to pay

- Ask a billing question

- Start chat

- Schedule a callback

Mobile-accessible portals and digital payment links reduce inbound volume because customers can resolve the account without waiting for an agent.

4. Payment Plan, Hardship, and Dispute Routing

Not every early delinquency has the same cause. Some customers need installment options, whereas others need a due date change. Others need a billing dispute reviewed before they will pay.

A strong workflow identifies those paths early.

Capturing disputes early also protects downstream recovery. If the account later moves into third-party collections, clean documentation helps reduce confusion, duplicate work, and compliance exposure.

5. Escalation Logic for Non-Responsive Accounts

Every early-stage program needs defined exit rules.

Those rules should answer:

- When does soft outreach stop?

- When does the account move to first-party escalation?

- When should it move to third-party collections?

- Which accounts need manual review?

- Which accounts should pause because of a dispute?

Without clear escalation logic, unresolved accounts sit idle and continue aging.

First-Party vs. Third-Party Early-Stage Collections

Businesses often hear both terms when researching early delinquency collections. The difference affects branding, compliance, tone, and customer experience. Let’s explore more in detail:

What are First-Party Early-Stage Collections

First-party early-stage collections happen under the creditor’s own brand. The customer sees communication from the business they already know, even when an outsourced partner manages outreach on the creditor’s behalf.

This model works well when customer retention matters. For example, a fitness brand recovering missed membership dues may want outreach to feel like account support, not collections. First-party outreach is usually softer, brand-sensitive, and focused on early account recovery.

What are Third-Party Early-Stage Collections

Third-party collections involve an outside collector contacting consumers under the collector’s own identity.

Even when the account is still relatively early in the delinquency lifecycle, FDCPA requirements are relevant if a third-party debt collector is involved. Disclosures, validation notices, communication controls, and opt-out management need to be built into the workflow from the first contact.

Hybrid and Managed Service Models

Many programs use a hybrid model. Early outreach remains first party, and unresolved accounts transition to third-party collections after a defined threshold.

This structure helps businesses preserve a softer recovery experience early while still maintaining an escalation path for accounts that do not resolve.

Compliance Considerations in Early-Stage Collections

Early-stage collections are not exempt from regulatory requirements. Even soft collections and digital payment reminders need controls around timing, consent, frequency, documentation, and consumer rights.

FDCPA at the Early Stage

The FDCPA governs third-party debt collectors and prohibits harassment, misrepresentation, improper timing of contact, and certain communication practices.

If an outsourced third-party collector contacts consumers, FDCPA compliance matters from the first outreach. The account does not need to be late-stage for compliance obligations to apply.

Regulation F and Digital Communication

Regulation F adds important controls around call frequency, electronic communication, validation notices, and opt-outs.

Early-stage cadence design should account for these rules. A workflow that sends repeated reminders without channel governance may create risk, even if the tone is soft.

Industry-Specific Compliance Layers

Some industries carry additional requirements, such as:

- Healthcare programs may need HIPAA-aware workflows.

- Consumer lending and fintech may involve state-level licensing, UDAAP considerations, and strict documentation.

- Fitness and subscription businesses need TCPA controls for SMS and recurring outreach.

As per Consumer Financial Protection Bureau (CFPB) regulations, servicers must establish or attempt live contact with a delinquent borrower by the 36th day of delinquency and, in many cases, provide written notice by the 45th day.

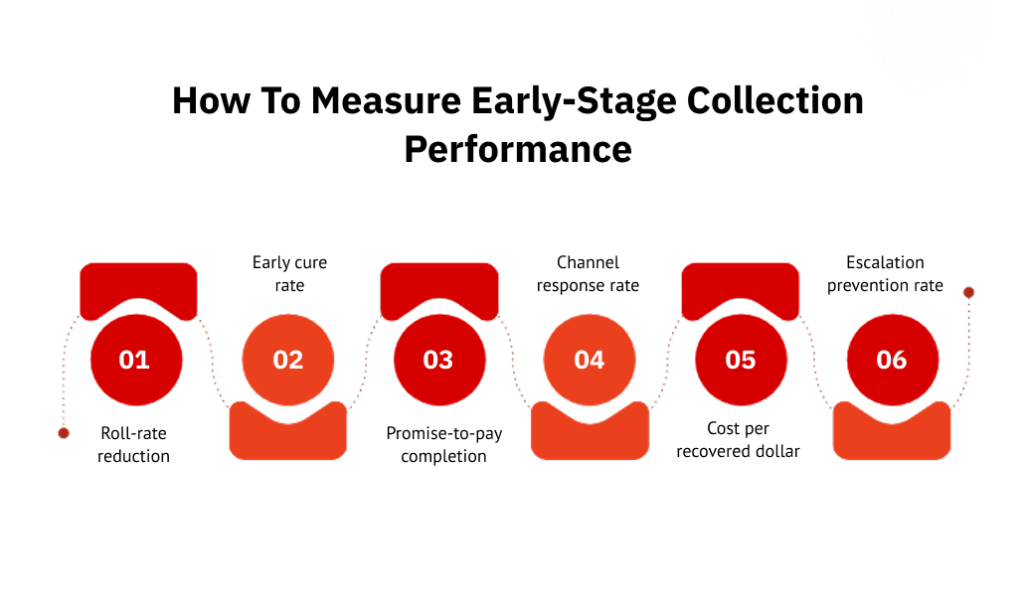

How to Measure Early-Stage Collection Performance

Early-stage collection performance should be measured by whether accounts resolve earlier, roll rates decline, and fewer accounts require late-stage or third-party escalation.

Contact volume alone is not enough. A team can make many calls and still fail to improve recovery. Here’s what you should consider:

1. Roll-Rate Reduction

Roll rate shows how many accounts move from the current to 30 DPD, from 30 to 60 DPD, and from 60 to 90 DPD. This is one of the most important early delinquency management metrics because it shows whether accounts are aging into more serious stages.

2. Early Cure Rate

Early cure rate measures the number of accounts that return to good standing during the early-stage window. A rising cure rate usually means outreach is reaching the right customers with the right resolution options.

3. Promise-to-Pay Completion Rate

A promise to pay is only useful if the customer follows through. If promise-to-pay volume is high but completion is low, the problem may be payment friction, unrealistic payment dates, or lack of follow-up.

4. Channel Response Rate

SMS, email, phone, portal, and chat should be measured separately. This helps businesses identify which channels work best by customer type, account stage, and balance size.

5. Cost Per Recovered Dollar

Early-stage outreach should be compared against the cost of third-party placement or legal escalation. If early intervention lowers cost per recovered dollar, it gives the business a strong case for investing earlier in the lifecycle.

6. Escalation Prevention Rate

This metric tracks how many accounts avoided charge-off, third-party placement, or late-stage recovery because early outreach resolved them first.

When to Outsource Early-Stage Collections?

Many businesses start with internal AR teams handling early-stage follow-up. Outsourcing becomes relevant when account volume, channel complexity, compliance needs, or staffing limits make consistent outreach difficult.

It may make sense to outsource when:

- Delinquency volume rises faster than internal teams can manage.

- Phone-only outreach yields low response rates.

- Payment plans create too much manual follow-up.

- Accounts regularly move past 60 DPD before meaningful contact happens.

- Internal teams struggle to coordinate SMS, email, phone, chat, and portal-based outreach.

- Compliance requirements demand consent management, dispute routing, audit trails, and documented workflows.

- The business needs first-party or third-party flexibility based on account stage and recovery strategy.

In these cases, a managed early-stage collections partner can help businesses standardize outreach, improve account coverage, and reduce the risk of missed follow-ups across high-volume portfolios.

Act Earlier While Accounts are Still Recoverable

Early-stage debt collection works best when businesses treat delinquency as a recoverable moment, not a waiting period before formal collections.

The recovery window narrows quickly. The cost of waiting compounds through lower response rates, higher internal workload, and more accounts moving into late-stage recovery.

A strong early-stage program uses segmentation, omnichannel outreach, digital account resolution, payment plans, dispute routing, and clear escalation rules to resolve more accounts before they age.

Want to know how FCS helps turn early-stage delinquency into faster resolution through managed collections and personalized outreach?

FAQs

1. How is early-stage debt collection different from pre-collection services?

The terms overlap. Pre-collection often refers to outreach before formal collections, while early-stage debt collection can include structured recovery activity once an account becomes newly delinquent.

2. Why do recovery rates decline as accounts age?

Older accounts are harder to resolve because customers are harder to reach, documentation gaps increase, disputes become more complex, and payment intent often weakens.

3. What industries use early-stage debt collection most?

Common users include healthcare, auto finance, consumer lending, fintech, utilities, subscriptions, and fitness businesses with recurring payments or high account volumes.

4. What channels work best for early delinquency outreach?

The best channel depends on the customer segment. Strong programs usually combine SMS, email, phone, chat, and self-service portals rather than relying on one channel.

5. What compliance rules apply to early-stage debt collection?

FDCPA, Regulation F, TCPA, HIPAA, state licensing rules, and industry-specific requirements may apply depending on the account type, channel, and whether a third party is involved.

6. How do businesses know if their early-stage collections program is working?

Track roll-rate reduction, early cure rate, promise-to-pay completion, channel response, cost per recovered dollar, and escalation prevention rate.