")

Every collection touchpoint now carries more compliance weight.

As per the Consumer Financial Protection Bureau (CFPB)’s 2024 report, debt collection complaints nearly doubled in 2024, rising from roughly 109,900 the year before to about 207,800. For teams recovering balances at scale, that increase is hard to ignore. It signals closer scrutiny from regulators, consumers, and plaintiff attorneys.

Debt collection compliance is no longer just about knowing the law. It is about making sure every call, text, email, disclosure, dispute response, and vendor action follows it. That is where many programs break. Not in policy documents, but in day-to-day execution across teams, channels, and workflows.

This guide explains the five federal laws governing collections, the requirements that matter most in daily operations, the common gaps that pose risk, and what to evaluate before outsourcing collections.

Contents

- 1 What Debt Collection Compliance Means (and Why It Matters Now)

- 2 The Five-Layer Regulatory Framework

- 3 Core Compliance Requirements in Practice

- 4 Where Compliance Programs Most Commonly Break Down

- 5 Compliance in an Outsourced Collections Program

- 6 Building a Compliance-Monitoring Routine

- 7 Choosing a Collections Partner That Builds Compliance In

- 8 FAQs

- 8.1 1. What is the difference between FDCPA and Regulation F?

- 8.2 2. What is the 7-in-7 rule in debt collection?

- 8.3 3. What must a Regulation F validation notice include?

- 8.4 4. Does FDCPA compliance apply to first-party collections?

- 8.5 5. What are the penalties for FDCPA violations?

- 8.6 6. What should you look for in a debt collection partner’s compliance program?

What Debt Collection Compliance Means (and Why It Matters Now)

Debt collection compliance is the structured practice of following the federal and state laws that govern how, when, and through which channels you can contact consumers, disclose debt information, handle disputes, and report account data. It is not a policy binder. It is a live control system that has to work under real volume, across every channel, agent, and workflow.

It matters more now because the activity that draws complaints is the same activity that draws enforcement. The CFPB’s 2025 report states that about 45% of debt collection complaints involved a debt the consumer said they did not owe, the most common complaint type since 2013.

That gap between what gets collected and what is actually owed is where compliant collection practices either protect you or expose you.

The Cost of Non-Compliance

The penalties are not abstract; they compound at the portfolio scale.

- Fair Debt Collection Practices Act (FDCPA): As per FDCPA guidelines, individual lawsuits can result in up to $1,000 in statutory damages per action, not per violation, along with actual damages and the consumer’s attorney fees. For class actions, statutory damages are capped at the lesser of $500,000 or 1% of the debt collector’s net worth.

- Telephone Consumer Protection Act (TCPA): According to the Legal Information Institute’s text of 47 U.S.C. § 227, the federal statute behind the TCPA, a person may recover $500 per violation, with damages increasing up to three times that amount for willful or knowing violations.

A $1,000 individual claim looks small. The attorney fees attached to it do not, and they are why a technical slip can cost far more than the balance you were chasing.

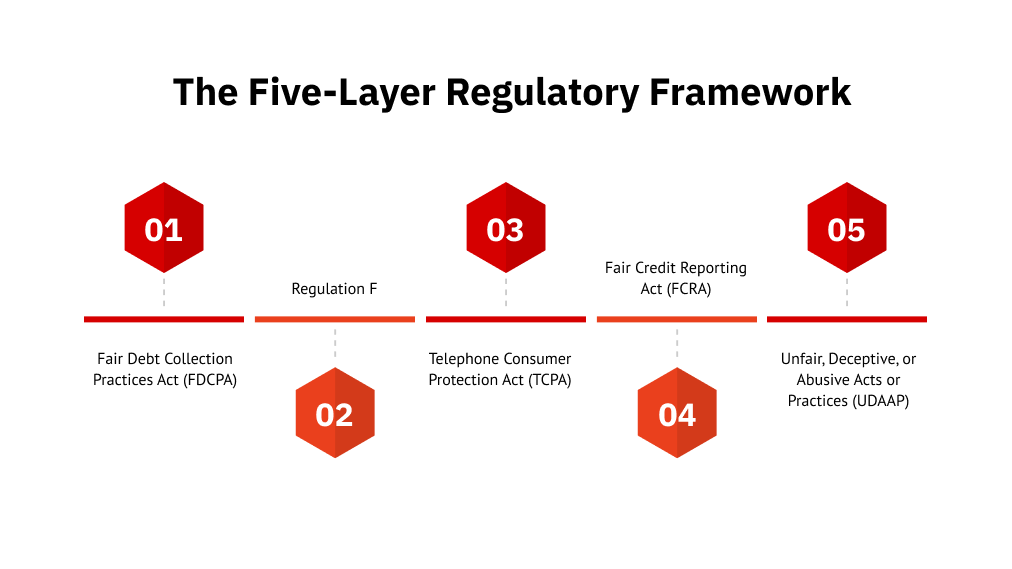

The Five-Layer Regulatory Framework

Five federal laws shape almost every collections decision you make. They overlap, but each carries its own obligations and its own enforcer. Satisfying one does not satisfy the others.

Here is how the five debt collection regulations line up.

| Law | Who It Covers | Core Obligation | Enforced By |

| FDCPA | Third-party collectors of consumer debt | No harassment, deception, or unfair practices | CFPB, FTC, private suits |

| Regulation F | Same “debt collector” definition as FDCPA | Modern-channel rules, call frequency limits, validation notice | CFPB |

| TCPA | Anyone placing automated calls or texts to mobiles | Prior express written consent for automated contact | FCC, private suits |

| FCRA | Furnishers reporting account data to bureaus | Accurate reporting, dispute verification | CFPB, FTC |

| UDAAP | Any provider (broad catch-all) | No unfair, deceptive, or abusive acts or practices | CFPB |

1. FDCPA: The Foundation

Start with the law; everything else builds on it. FDCPA compliance is the floor.

The FDCPA, enacted in 1977, governs third-party debt collectors recovering consumer debts. It prohibits harassment, deception, and unfair practices across every channel. It does not cover original creditors collecting their own debts, unless they collect under a different name. That carve-out is why first-party and third-party programs are subject to different compliance expectations.

2. Regulation F: FDCPA Modernized

The FDCPA predates email, texting, and self-service portals. Regulation F is how the CFPB brought those channels into the collection rulebook.

Regulation F compliance adds the modern-channel layer. The CFPB’s 2021 rule applies the FDCPA to email, SMS, and online portals. It also introduced the 7-in-7 rule, which generally limits collectors to seven call attempts about a debt within seven days and restricts calls for seven days after a live conversation about that debt. The rule also introduced the model validation notice, Model Form B-1, and consent requirements for electronic communication that lean on the e-SIGN Act.

It uses the same definition of debt collector as the FDCPA, so first-party creditors are not covered unless they operate under a separate name.

3. TCPA: Consent for Every Digital Touch

Reg F sets the rules for collections messaging. The TCPA sets the rules for whether you can dial or text at all.

The TCPA governs automated calls, prerecorded messages, and texts to mobile numbers. Before you send an automated collection text, you need prior express written consent, and it has to be separate from your other terms. Reassigned numbers are the quiet risk.

According to the FCC’s reassigned numbers database, around 35 million numbers are disconnected and reassigned each year, roughly 100,000 a day. Consent does not travel with the number. Hence, checking the FCC’s reassigned numbers database before you dial gives you a safe harbor. Skipping it leaves your auto dialer exposed.

4. FCRA: What You Report and How

Contacting the consumer is one obligation. Reporting the account is another.

The Fair Credit Reporting Act (FCRA) governs how you furnish account information to the credit bureaus. The moment a consumer challenges accuracy, your dispute verification duties begin. This is where teams get caught: FDCPA and FCRA are separate obligations.

You can handle a dispute correctly under the FDCPA and still violate the FCRA if the credit reporting side never hears about it.

5. UDAAP: The Catch-All Enforcement Layer

Even a program that checks every box above is not fully in the clear.

The Unfair, Deceptive, or Abusive Acts or Practices (UDAAP) is the CFPB’s broadest lens. You can meet every Regulation F requirement and still draw exposure here. Settlement framing, AI-driven personalization, and aggressive digital sequencing are increasingly read through a UDAAP lens. It is the rule with the least bright line and the most discretion, which is exactly what makes it hard to plan around.

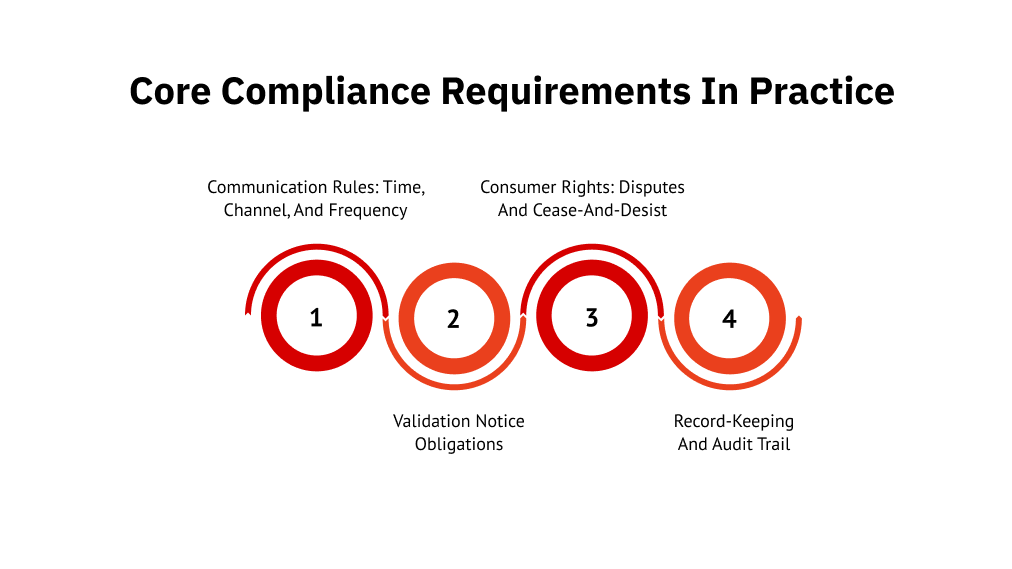

Core Compliance Requirements in Practice

The framework tells you which laws apply. The day-to-day work lives in four areas, and this is where most programs either hold or crack.

1. Communication Rules: Time, Channel, and Frequency

Start with when and how often you can reach someone. These are the communication limits that auditors check first.

- No contact before 8am or after 9pm in the consumer’s local time zone.

- The 7-in-7 rule: no more than 7 calls to a consumer about a debt within 7 consecutive days, and no calls for 7 days after you reach them by phone.

The trap is treating the 7-in-7 ceiling as a quota. Seven is the maximum, not the target. Auditors flag the quota mindset more than almost anything else, because it quietly turns a hard limit into a daily habit.

2. Validation Notice Obligations

Before you press for payment, the consumer has a right to know what they owe.

You must provide a validation notice at or within five days of first contact. It has to state the amount owed, the creditor, and the consumer’s dispute rights. Regulation F’s Model Form B-1 provides a safe harbor when used correctly. During the validation window, nothing in your outreach can overshadow or contradict those rights.

3. Consumer Rights: Disputes and Cease-and-Desist

Consumer rights are not passive. They change what you are allowed to do next.

According to 15 U.S.C. § 1692g, a consumer has 30 days to dispute the debt in writing, and you must pause collection until the debt is verified. A written cease-and-desist request has to be honored. After it, you can only confirm receipt or note specific legal action. Documenting the request and your response is the evidence record if a complaint is ever filed.

4. Record-Keeping and Audit Trail

Every rule above is only as good as your ability to prove you followed it.

Regulation F requires you to retain records evidencing compliance from the start of collection activity until three years after the last activity. Call recordings carry the same three-year window. The most common finding in a CFPB supervisory examination is an audit trail gap: an undocumented opt-out, a missing consent log, an incomplete call record. The activity was fine. The proof was not.

Where Compliance Programs Most Commonly Break Down

Most violations are not failures of legal knowledge. They are failures of execution, and they cluster in predictable places.

Operational Failures vs. Knowledge Failures

The gap is rarely the law. It is the system running underneath it.

Teams know they cannot text without consent. They still get caught when a misconfigured autodialer fires against a stale list, or a manual opt-out process does not scale. A single misconfigured SMS campaign can produce hundreds of TCPA violations in a day. The dollar math compounds before anyone notices.

Three Patterns That Account for Most Enforcement Exposure

Three failure patterns recur, such as:

- Treating the 7-in-7 ceiling as a permitted call quota instead of a hard limit.

- Honoring TCPA opt-outs at the account level but not at the individual consumer level.

- Running FDCPA and FCRA as separate programs, so a dispute handled correctly on the collections side never reaches credit reporting.

Each one is an operational fix, not a legal one. First Credit Services builds these checks into the workflow itself. Thus, opt-outs, frequency caps, and dispute handoffs are enforced as the account moves, rather than being caught in an audit after the fact.

Compliance in an Outsourced Collections Program

Outsourcing collections does not outsource the risk. It reshapes it.

What Changes When You Outsource

The first thing to understand is where liability actually lands.

Your third-party collector is legally a debt collector under the FDCPA, and their violations create direct exposure for your brand. Client-side duties do not transfer. Vendor due diligence, written agreements with compliance representations, and ongoing monitoring stay with you.

Under the Dodd-Frank Act, the CFPB can supervise service providers, which means your partner’s compliance posture becomes part of your own examination risk.

What to Evaluate in a Vendor’s Compliance Program

That shared exposure is why vendor evaluation is a compliance task, not a procurement one. Use this as a checklist.

- Licensing and bonding are verified in every operating state, including under state debt-collection laws such as the California Rosenthal Act.

- Documented FDCPA, Regulation F, TCPA, and FCRA policies, not just certificates on a wall.

- Call monitoring and QA: what share of interactions get reviewed, and how escalations are handled.

- Audit trail depth: Can they produce documentation for any consumer interaction within 24 to 48 hours?

- Data security: SOC 2 Type II, PCI DSS, and HIPAA, where healthcare accounts are involved.

Membership in a body like ACA International signals professional standards, but treat it as a floor, not proof. For each policy, ask for the workflow behind it.

FCS’s Compliance Approach

FCS builds compliance controls into operational workflows instead of bolting on a separate compliance overlay. Its digital debt collection platform, the Unified Consumer Engagement Platform (UCEP), documents interactions in real time and orchestrates channels in accordance with consent and frequency rules as accounts move. UCEP connects to your existing billing system rather than replacing it.

Across first-party collections and third-party collections, the same controls travel with the account, so opt-outs and dispute handoffs do not get lost at the seams. With more than three decades in regulated recovery and contingency-based pricing, FCS handles compliance as part of the service, not as your monitoring burden.

Evaluating a recovery partner? See how FCS folds debt collection compliance into every stage of outreach, from first contact through escalation.

Building a Compliance-Monitoring Routine

Compliance is not a launch task. It is routine, and the teams that stay clear of trouble treat monitoring as an ongoing operation.

Four Monitoring Practices That Reduce Exposure

Four practices catch most problems before they become findings.

- Monthly audit of call logs against the 7-in-7 rule across all active accounts.

- Quarterly TCPA consent review, scrubbed against the reassigned numbers database.

- Annual third-party vendor audit with documented findings and remediation timelines.

- Weekly complaint management review across the CFPB complaint database and your internal logs.

When to Revisit Your Compliance Framework

Beyond the routine, certain changes should trigger a fresh review.

- You add a channel to your outreach sequence, such as SMS or chat.

- Your portfolio shifts. Adding healthcare accounts, for example, pulls HIPAA into scope.

- A state updates its rules. California, New York, and Texas are the most active, and state debt collection laws often move faster than the federal ones.

Choosing a Collections Partner That Builds Compliance In

The five-layer framework, FDCPA, Regulation F, TCPA, FCRA, and UDAAP, is the part you can learn. Staying compliant is the harder part because failures stem from execution: a stale consent record, an opt-out that did not propagate, or a dispute that never reached credit reporting.

The right partner does not just know the rules. It builds them into every workflow, so compliance is enforced as accounts move instead of being reconstructed during an examination.

Build recovery on a compliant foundation. Talk to FCS about a collections program with compliance designed into every channel and stage.

FAQs

1. What is the difference between FDCPA and Regulation F?

The FDCPA is the 1977 law governing third-party collectors. Regulation F is the CFPB’s 2021 rule applying it to modern channels like email and SMS, adding call frequency limits and a model validation notice.

2. What is the 7-in-7 rule in debt collection?

Under Regulation F, a collector cannot make more than 7 calls to a consumer about one debt within 7 consecutive days, and cannot call again for 7 days after reaching them by phone.

3. What must a Regulation F validation notice include?

It must state the amount owed, the creditor’s name, and the consumer’s dispute rights, and reach the consumer at or within five days of first contact. Model Form B-1 provides a safe harbor.

4. Does FDCPA compliance apply to first-party collections?

Generally no. The FDCPA covers third-party collectors, not original creditors collecting their own debts, unless the creditor uses a different name. First-party programs still face TCPA, FCRA, UDAAP, and state obligations.

5. What are the penalties for FDCPA violations?

Up to $1,000 in statutory damages per lawsuit, plus the consumer’s attorney fees and any actual damages. Class actions are capped at the lesser of $500,000 or 1% of the collector’s net worth.

6. What should you look for in a debt collection partner’s compliance program?

Verified state licensing, documented FDCPA, Regulation F, TCPA, and FCRA policies, call monitoring, fast audit trail retrieval, and data security like SOC 2 Type II and Health Insurance Portability and Accountability Act (HIPAA). Ask for the workflow, not just the certificate.