Ten years ago, debt collection looked like this: a list of overdue accounts, a team of agents, and a phone that rang all day. It was slow, it was manual, and honestly, it kind of worked.

Today, account volumes have tripled. Customers do not pick up unknown numbers. Agents are buried under backlogs. And that same manual process is now quietly bleeding revenue every single month.

The businesses winning at collections right now are not the ones with the biggest teams. They are the ones who stopped relying on people to remember things and built systems that never forget.

Automated debt collection triggers outreach the moment a payment fails, segments accounts by priority, and gives customers a fast, frictionless way to resolve the issue without an agent involved at every step.

The gap is no longer small. As of 2024, organizations using automated debt collection tools are seeing collection cycles move up to 48% faster than those relying on manual processes, and over 63% of financial organizations have already made the switch, as per Market Growth Reports.

This guide breaks down how automated debt collection works, what it delivers, and how to know if it is time to make the shift.

Contents

- 1 What is Automated Debt Collection?

- 2 What Are the Benefits of Automated Debt Collection?

- 3 How Automated Debt Collection Works

- 3.1 Step 1: Import Account Data and Segment the Portfolio

- 3.2 Step 2: Trigger the Collections Workflow Automatically

- 3.3 Step 3: Send Payment Reminders Across the Right Channels

- 3.4 Step 4: Let Customers Resolve the Issue Through Self-Service or Assisted Support

- 3.5 Step 5: Record Outcomes, Update Systems, and Optimize the Next Action

- 4 Automated Debt Collection vs Manual Collections

- 5 Key Components of Automated Debt Collection Software

- 6 What to Look for in Debt Collection Automation Software

- 7 Is Automated Debt Collection Right for Your Business?

- 8 Final Thoughts

- 9 FAQs

What is Automated Debt Collection?

Automated debt collection is the use of software, AI, and workflow automation to recover overdue payments through rules-based reminders, account prioritization, digital communication, and self-service payment options.

Instead of relying on manual follow-up alone, businesses use automated systems to trigger outreach, segment accounts, monitor engagement, and route complex cases to human agents only when genuinely needed.

Why It Matters Right Now

Consumer debt in the US hit a record high of $17.7 trillion as of Q2 2024, as per the Federal Reserve Bank of New York press release, while pandemic-era savings were fully depleted by March of the same year.

At the same time, customer expectations have shifted. People expect digital, convenient, and non-intrusive interactions even when resolving a missed payment.

Manual processes cannot keep up with that combination of rising volume and rising expectations. Businesses still relying on agent-led follow-ups are not just slower; they are structurally disadvantaged compared to those using automated workflows.

What Counts as Automation in Collections

Modern automated debt collection is really four layers working together:

- Workflow automation that triggers reminders, escalates dunning sequences, and decides what happens next based on customer behaviour

- Deciding that segments are accounted for by risk, balance, or delinquency stage, and picking the right channel and timing

- Digital engagement that delivers payment links through SMS, email, or self-service portals where customers can pay, set up plans, or update payment methods

- Human escalation for the cases that need a conversation, not a script

When all four layers connect cleanly, you get a recovery system that is faster, cheaper, and noticeably less stressful for the customer on the other end.

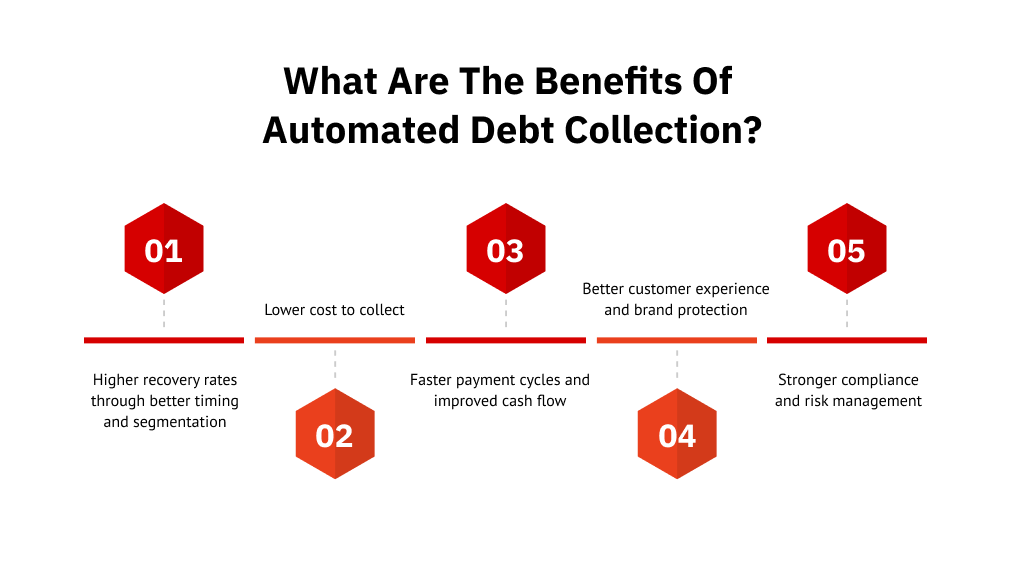

What Are the Benefits of Automated Debt Collection?

Automated debt collection helps you recover more revenue with less manual effort. The lift comes from better timing, consistent follow-up, and a payment experience that does not make customers work to pay you.

1. Higher Recovery Rates Through Better Timing and Segmentation

The biggest reason recovery rates improve with automation is precision, not volume. By segmenting accounts based on delinquency stage, payment history, risk level, and communication behaviour, every account gets the right outreach at the right time. High-priority accounts are not buried under low-value ones. Early-stage accounts get engagement before they escalate. And outreach happens the moment a trigger fires, not three days later when someone remembers.

The results reflect this. McKinsey research shows that AI and generative AI applied to collections can lift recovery rates by around 10% while reducing operating costs by up to 40%, a combination that changes the economics of collections significantly. For recovery operations leaders managing thousands of accounts monthly, that shift changes what’s possible without adding headcount.

2. Lower Cost to Collect

Every call, reminder, and status check costs the agent time. Automation strips out the routine work: fewer manual touches per account, fewer agent hours on low-complexity cases, fewer missed follow-ups that let accounts go cold, and higher portal payment completion.

For most teams, this is where the math starts working. Cost-to-collect drops while recovery holds steady or improves. This is usually the number that gets CFOs and billing operations leads to pay attention, because it’s the one metric that shows up directly on the P&L

3. Faster Payment Cycles and Improved Cash Flow

The longer an account sits without meaningful outreach, the harder it becomes to recover. With automation, reminders go out the moment a payment fails. Payment links land in the right channel within hours. Self-service portals let customers resolve at midnight on a Sunday.

For businesses managing high account volumes across recurring billing cycles, this has a direct impact on days’ sales outstanding and monthly cash flow.

4. Better Customer Experience and Brand Protection

Customers who receive aggressive, repetitive, or poorly timed outreach do not just ignore it. They remember it. In competitive industries, a collections experience that feels intrusive can undo brand equity built elsewhere.

Done well, automated collections feel nothing like traditional recovery. Respectful tone, convenient for the customer, flexible enough to offer payment plans without a phone call, and consistent across every account.

| Did you know? Some managed service providers take this further by operating entirely under the client’s brand. The customer never sees a third-party name, never gets transferred to an unfamiliar company, and never feels like their account has been ‘sent to collections.’ The entire experience stays within the brand relationship they already trust. |

5. Stronger Compliance and Risk Management

Manual collection processes are inherently inconsistent, and each gap in scripts, contact rules, or opt-out handling is a potential liability.

Automation addresses this at the process level with standardized templates, system-enforced contact frequency rules, and full communication logs retained for every account.

| CFPB complaint volumes in debt collection nearly doubled year-over-year, rising from roughly 109,900 in 2023 to 207,800 in 2024, a sharp signal that regulatory scrutiny is intensifying, as per the CFPB 2024 Annual Report. CFPB 2024 Annual Report. |

For compliance teams, this is not just a regulatory checkbox. It is the difference between defensible operations and reactive damage control.

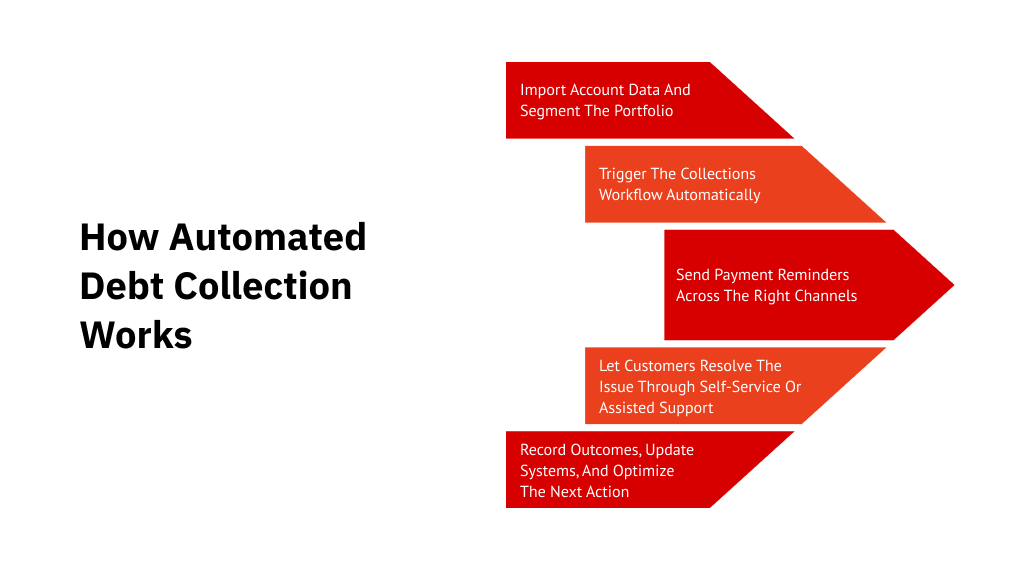

How Automated Debt Collection Works

At a practical level, automated debt collection works by connecting overdue accounts to workflow rules. The system decides who to contact, when, through which channel, and what to do next based on customer behaviour, payment status, and business policy.

You can think of it as a five-step loop.

Step 1: Import Account Data and Segment the Portfolio

Automation starts with clean, connected data pulled from your CRM, ERP, billing platform, or payment processor. The fields that matter most are account balance, days past due, payment history, customer profile, contact preferences, risk level, and dispute history.

Not every overdue account should follow the same workflow. Accounts are typically grouped by:

- Delinquency stage

- Account value

- Likelihood to pay

- Communication behaviour

- Industry or product type

The biggest split is pre-charge-off versus post-charge-off. Pre-charge-off accounts get customer-first treatment focused on resolution and retention. Post-charge-off accounts follow recovery-focused workflows with stricter compliance and a more structured tone. Skipping this step is the most common reason automation projects underperform.

Step 2: Trigger the Collections Workflow Automatically

Once accounts are segmented, the system kicks in based on triggers like an overdue invoice, a failed renewal, an ACH decline, a missed promise-to-pay, or a skipped instalment.

When a trigger fires, the system enrolls the account into a workflow, assigns a cadence, sets escalation rules, picks the channel priority, and inserts the right payment link. Most modern platforms blend rule-based logic with AI-assisted next-best-action models. Rules give consistency. AI optimizes within them.

Step 3: Send Payment Reminders Across the Right Channels

Multichannel means sending messages on different channels. Omnichannel means each message builds on the last, channel switches reflect behaviour, and timing feels intentional.

Experian found that 73% of customers contacted through digital channels for overdue accounts made at least a partial payment, compared with 50% contacted through traditional channels. Digital-first approaches also delivered a 25% increase in resolutions and 15% lower collections cost.

This is exactly why platforms like FCS’s UCEP lead with digital channels and use AI to pick the best time and channel for each consumer. UCEP can run as a standalone digital collections engine or be paired with live agent outreach, depending on what the portfolio needs

Step 4: Let Customers Resolve the Issue Through Self-Service or Assisted Support

Once a customer engages, the system should make resolution as simple as possible. That means giving them access to their outstanding balance, a one-click payment option, an instalment plan they can set up without speaking to anyone, or a settlement offer they can accept immediately.

For hardship cases, disputes, complaints, and sensitive accounts, the system hands off to a human agent with full context of every prior interaction already visible.

Step 5: Record Outcomes, Update Systems, and Optimize the Next Action

Every interaction feeds back into the system and shapes what happens next. Payments close workflows instantly. Promises to pay pause reminders until the due date. Unresponsive accounts trigger escalation automatically.

At the portfolio level, the system continuously tracks which channels, send times, and message variants are driving the best recovery outcomes. Over time, this turns collections from a static follow-up process into a performance system that improves with every cycle.

Automated Debt Collection vs Manual Collections

Manual collections still work for small portfolios and high-touch accounts. But once volume grows beyond what your team can cover consistently, the gaps start compounding. Follow-ups slip. Outreach becomes uneven. Reporting depends on whoever remembered to update the spreadsheet.

Automation does not replace your team. It changes what your team spends time on. The system handles scale and consistency. People handle empathy, judgment, and exceptions.

Side by Side: Automated vs Manual Collections

| Manual Collections | Automated Collections | |

| Trigger speed | Depends on agent availability | Instant, event-based |

| Portfolio coverage | Limited by team capacity | Full portfolio, no accounts missed |

| Outreach consistency | Variable across agents | Standardised across every account |

| Channel mix | Primarily phone-led | Omnichannel, behaviour-driven |

| Compliance controls | Policy-dependent, inconsistent | System-enforced, auditable |

| Reporting | Manual, retrospective | Real-time, automated |

| Scalability | Requires headcount growth | Scales without proportional cost increase |

| Human involvement | Every touchpoint | Complex cases and exceptions only |

Where Human Agents Are Still Essential

Anyone who tells you automation can run end-to-end recovery without humans is selling you something. The cases that need a person are usually the ones that move the most money or carry the most risk.

Human agents remain essential for hardship assessments where rigid rules would do more harm than good, disputes that need investigation across multiple records, negotiations that fall outside standard policy, complaint handling and escalations, vulnerable consumers who need a careful conversation, and high-balance or sensitive accounts where one wrong message creates a real problem.

Automation handles the volume. Agents handle the complexity. The two should not compete for the same accounts.

Key Components of Automated Debt Collection Software

Not all platforms are built the same. The “How It Works” section above covers the process. This section is about what separates a platform that runs well from one that creates new problems.

1. Workflow Automation Engine

The difference between a good engine and a mediocre one is flexibility. Can it handle branching logic based on customer behaviour, not just account age? Can your team adjust escalation paths without filing engineering tickets every time? If changing a workflow requires developer support, the engine is too rigid.

2. AI and Predictive Decisioning

AI only adds value if it is learning from your data. Look for propensity-to-pay scoring, contact timing optimisation, and channel selection based on actual engagement patterns. Ask how the model trains, how often, and on what data. If the answer is vague, the AI probably is too.

3. Integrations With CRM, Billing, and Payments Infrastructure

A collections platform operating in isolation creates duplicate data and outreach based on outdated information. The question is not “do you integrate with X” but “how current is the data sync?” If account statuses update with a delay, your workflows are making decisions on stale information.

4. Compliance Controls and Audit Trails

Compliance needs to be embedded in how the system operates, not layered on after. Message frequency rules, opt-out management, communication logs, and policy guardrails should prevent non-compliant outreach before it happens. CFPB Regulation F governs communication practices, disputes, and record retention. If you are evaluating third-party collections partners, ask for certifications, not assurances.

What to Look for in Debt Collection Automation Software

If you are starting to evaluate platforms, here is a quick baseline. A strong collections automation platform should cover all of the following without requiring heavy customization or third-party add-ons:

- Workflow builder with trigger-based logic and branching rules

- Omnichannel messaging across email, SMS, voice, and digital portals

- AI-based account segmentation and contact prioritization

- Self-service payment portal with instalment and settlement options

- Promise-to-pay tracking and automated follow-up sequencing

- CRM, billing, and payment gateway integrations

- Compliance controls, including opt-out management and contact frequency rules

- Real-time analytics with segment and channel-level reporting

- Full audit logs across every account and communication

If a platform cannot deliver these out of the box, the gaps will show up as manual workarounds, compliance risks, or recovery inefficiencies down the line.

| For industries like healthcare and financial services, also look for specific certifications. First Credit Services, for example, holds HIPAA, PCI DSS Level 1, and SOC 2 Type II, which is the kind of baseline you should expect from any partner handling sensitive consumer data. |

Is Automated Debt Collection Right for Your Business?

Automation is not the right move for every business. If you have a small portfolio, simple payment terms, and a collections team that can handle the volume by hand, you may not need a platform yet. The signs that you do need one usually show up gradually, then all at once.

The trigger points look different depending on where you operate.

- In healthcare, it might be a growing pile of patient balances post-insurance with no scalable way to follow up compliantly.

- In auto finance or consumer lending, it could be delinquency rates climbing while your internal team maxes out on outbound calls.

- For subscription and fitness businesses, the problem often shows up as involuntary churn from failed payments that nobody catches fast enough.

The common thread is the same: volume has outpaced what manual processes can handle

Signs You Have Outgrown Manual Collections

- A growing volume of overdue accounts that your team cannot keep up with

- Missed follow-ups are slipping through because nobody owns them

- Inconsistent outreach, where some customers get five reminders and others get none

- Agent productivity is flatlining even as you add headcount

- Reporting that depends on someone manually pulling spreadsheets

- Too many reminders are going out at the wrong time or through the wrong channel

- Cost-to-collect rising faster than recovery

- No self-service option for customers who want to pay outside business hours

- Recovery rates are declining as the portfolio ages, even though customer behaviour has not changed

If three or more of these sound familiar, the case for automation is probably already made. The remaining question is how you get there.

Most businesses buy a platform rather than building one. The compliance, channel orchestration, and integration work involved is harder than it looks and takes longer than most teams expect.

Some go a step further and partner with a managed service provider who brings the platform, the agents, and the compliance framework together under one roof, which tends to be the fastest path for businesses that need recovery results without operating another system internally.

Many managed service providers also work on a contingency basis, meaning you only pay when they actually recover. That changes the risk profile significantly compared to licensing a platform with fixed costs regardless of performance

Final Thoughts

The point of automated debt collection is not speed for its own sake. It is building a recovery process that is consistent, customer-friendly, and able to scale without breaking.

Structured workflows replace reactive follow-ups. Digital self-service makes paying easier. And your team gets to focus on the cases where their judgment actually moves the needle.

If your current process still depends on spreadsheets and manual outreach, automation is no longer optional. It is how modern recovery operations work.

The goal is not just to collect more payments. It is to build a system that protects customer relationships while hitting the numbers your finance team needs.

Looking for a partner who brings the platform, the agents, and the compliance framework together?

Talk to First Credit Services about how UCEP can fit into your recovery process.

FAQs

1. Can automated debt collection be customized for different customer segments?

Yes. Most platforms allow workflows to be tailored based on factors like payment history, balance size, risk level, delinquency stage, and communication preferences. This ensures each customer receives relevant outreach rather than a generic reminder that treats every overdue account the same way.

2. Can automated debt collection work for both B2B and B2C businesses?

Yes. In B2B, automation manages invoice follow-ups and ageing accounts across longer payment cycles. In B2C, it supports subscription recovery, consumer lending, and high-volume digital outreach.

3. How long does it take to implement automated debt collection software?

Most platforms can be deployed within a few weeks to a couple of months. Timelines move faster when connecting with standard CRM, billing, and payment systems that the platform already supports.

4. Does automated debt collection reduce the need for internal collections teams?

It reduces manual workload significantly, but does not eliminate the need for people. Human agents remain essential for disputes, hardship cases, and complex negotiations.

5. How secure are automated debt collection systems?

Modern platforms follow strict security standards, including data encryption, role-based access controls, and compliance with financial regulations. This is especially critical in collections where systems handle sensitive customer data and payment information.

6. What metrics should you track to measure success in automated debt collection?

The metrics that matter most are recovery rate, days sales outstanding, payment conversion rate by channel, cost to collect, portfolio coverage, and customer engagement rates across outreach touchpoints.