A missed payment rarely tells the full story.

The customer may have forgotten, faced a failed payment, or simply missed the reminder. In other cases, the bill may be competing with more urgent expenses.

The Federal Reserve’s 2025 survey found that 16% of U.S. adults did not pay all of their bills in full in the prior month. That is why effective payment reminder services need to do more than follow a fixed schedule.

Different customers respond to different channels, timing, and payment options. The right next step can also change as the account ages. Modern first-party recovery brings those signals together. It uses account data, AI-driven best action, segmentation, omnichannel outreach, and self-service to guide each account toward resolution.

This guide explains how that approach works and what to look for in a modern payment reminder service.

Contents

- 1 What Are Payment Reminder Services?

- 2 Why A Fixed Payment Reminder Cadence Is Not Enough

- 3 What A Robust Payment Reminder Platform Should Do

- 4 Automated Payment Reminders Should Respond to Behavior

- 5 Self-Service Is Part of the Recovery Strategy

- 6 When Should a Human Agent Step In?

- 7 Manual Reminders vs Basic Automation vs Omnichannel Recovery

- 8 What To Look for in a Payment Reminder Service

- 9 Compliance Needs to Be Built into the Workflow

- 10 Why Managed Payment Reminder Services Can Outperform Another Standalone Tool

- 11 How FCS Approaches Payment Reminders and First-Party Recovery

- 12 Move Beyond Sending More Reminders

- 13 FAQs

- 13.1 1. How long does it take to launch a managed first-party payment reminder program?

- 13.2 2. What happens if an account remains unpaid after first-party outreach?

- 13.3 3. How often should a payment reminder strategy be reviewed?

- 13.4 4. Can payment reminder services handle sudden increases in account volume?

- 13.5 5. What should businesses prepare before outsourcing payment reminder services?

- 13.6 6. Can payment reminder services work with existing billing and CRM systems?

What Are Payment Reminder Services?

Payment reminder services help businesses recover upcoming, missed, and overdue payments through structured first-party outreach. Modern services go beyond scheduled reminders by combining account data, segmentation, omnichannel communication, behavioral signals, self-service payment options, and human escalation.

At the simplest level, a payment reminder service sends an email or text when a balance becomes due. A mature first-party recovery service does much more, such as:

- Identify accounts that need attention.

- Segment customers based on payment and engagement behavior.

- Determine the appropriate channel and next action.

- Coordinate email, SMS, chat, phone, and self-service.

- Adjust outreach when a customer responds or account status changes.

- Escalate complex accounts to a live agent.

In short, automated payment reminders eliminate the need to send messages manually. A robust first-party recovery program solves a larger problem: deciding who needs attention, what should happen next, and how to make resolution easier.

Why A Fixed Payment Reminder Cadence Is Not Enough

A typical reminder sequence can look reasonable in the following ways:

- Send an email before the due date.

- Send another when the payment becomes overdue.

- Follow up again a week later.

- Call if there is still no payment.

The problem is that every account follows roughly the same path.

Consider four accounts that are seven days overdue:

- One customer clicked the payment link but did not complete payment.

- One ignored several emails but has previously responded to SMS.

- One regularly pays late without needing agent support.

- One has a high balance and no engagement.

Putting all four into the same sequence wastes opportunities. The first customer may need an easier return to the payment page. The second may need a channel change. The third may require different timing. The fourth may need earlier human intervention.

A fixed cadence sees days past due. But a stronger first-party strategy sees the account, customer behavior, and the most appropriate next action.

What A Robust Payment Reminder Platform Should Do

The value of a payment follow-up service is not determined by how many reminders it sends. It is determined by how effectively it moves accounts toward resolution in the following ways:

1. Use connected account data

Effective outreach starts with current information. Hence, the platform or service should be able to work with relevant data such as:

- Balance and payment status.

- Due date and delinquency stage.

- Previous payments or failed payment attempts.

- Communication history.

- Customer engagement.

- Payment-plan status.

- Disputes or account notes.

Without connected data, outreach can quickly fall out of sync. A customer who has already paid may still receive a reminder, while someone on a payment plan may continue getting overdue notices. An agent may also call without knowing the customer has just engaged digitally.

A robust system uses current account activity to keep every interaction aligned with the account’s actual status.

2. Segment accounts before deciding how to contact them

Not every overdue account belongs in the same workflow. Segmentation groups accounts that require different treatment based on factors such as payment history, delinquency stage, responsiveness, balance, or engagement. Here is an example:

| Account situation | Potential treatment |

| Recent failed payment with digital engagement | Quick follow-up with a direct payment path |

| Emails ignored but previous SMS engagement | Change the channel |

| Active payment plan | Suppress standard overdue reminders |

| High-balance account with no response | Consider earlier agent-assisted outreach |

| Dispute or hardship signal | Route to a specialist workflow |

The objective is not to create dozens of static lists. It is to ensure the treatment reflects what is currently known about the account. First Credit Services (FCS) uses a digital collections approach designed to support more personalized engagement rather than one-size-fits-all outreach.

3. Use AI-driven best action instead of blindly following the calendar

Traditional automation asks, “What message is scheduled next?”

AI-assisted decisioning asks: What is the best next action based on what we know now?

That may mean sending an SMS, changing the timing, directing the customer to self-service, pausing outreach, or routing the account to an agent. The value of AI here is not simply writing a payment reminder but helping determine the treatment strategy.

For example, repeatedly emailing someone who responds to SMS is automated, but not intelligent. Once a customer starts resolving the account, the original sequence should also adapt. That is why a mature platform uses account and engagement signals to determine what happens next.

4. Coordinate channels as one recovery journey

Having email, SMS, phone, and chat does not automatically create an omnichannel strategy. A business can use four channels and still deliver four disconnected experiences.

Multichannel outreach means several channels are available. Omnichannel outreach ensures that these channels work together. For example:

- A customer receives an email.

- They open it but do not pay.

- The next action reflects that engagement.

- They later click an SMS payment link.

- Unnecessary phone follow-up is suppressed.

- If they request help, an agent receives the relevant account context.

The customer should not have to start over when the channel changes. That coordination reduces duplicate outreach, conflicting messages, unnecessary calls, and poor visibility into what is actually moving accounts toward payment.

Automated Payment Reminders Should Respond to Behavior

Automation still matters. The key is how intelligently it responds.

Basic automation follows a fixed rule:

Invoice overdue by seven days → send email.

More advanced automation combines triggers with account status and engagement:

Payment missed → identify the segment → choose the treatment → monitor the response → determine the next action.

Suppose a customer ignores the first message, opens the second, clicks the payment link, and leaves before completing payment. Those actions provide useful information. The next step should not necessarily be the same as the one scheduled before any of those interactions occurred.

This is where an invoice reminder service or dunning reminder service becomes part of a broader first-party recovery strategy. The system is no longer simply sending overdue payment notifications. It uses customer behavior to inform what happens next.

Self-Service Is Part of the Recovery Strategy

Even well-timed outreach can fail if paying is difficult.

Customers should not have to search for account details, find the right payment page, call during business hours, or wait for an agent to complete a simple transaction. Every extra step adds friction.

That convenience matters. A 2024 Federal Reserve payments study found that 58% of consumers had used digital wallets in the previous 12 months. It shows the continued shift toward flexible, digital payment options.

Because of this reason, the modern payment reminder service should connect outreach directly to resolution. Depending on the program, customers may be able to:

- Review their balance.

- Pay immediately.

- Choose a payment plan.

- Accept an eligible offer.

- Schedule a callback.

- Start a chat.

FCS supports a white-labeled experience that moves customers from a digital message into a personalized payment journey under the client’s brand. The portal is not separate from the reminder strategy, but the resolution layer behind it.

When Should a Human Agent Step In?

A strong digital strategy does not mean every account stays digital. Human support should step in when it adds value.

That may be when digital outreach gets no response, the customer raises a dispute, a hardship discussion is needed, or the account requires more attention. However, the key is coordination.

Agents should see the customer’s previous digital interactions before making contact. Once the issue is resolved or the account is updated, the digital workflow should be adjusted accordingly. That is what turns automated reminders and agent support into one connected first-party recovery operation.

FCS provides first-party collection services that combine digital engagement with agent support while operating as an extension of the client’s brand.

Manual Reminders vs Basic Automation vs Omnichannel Recovery

Businesses generally have three approaches:

| Model | How it works | Main limitation |

| Manual follow-up | Internal staff contact accounts individually | Difficult to maintain at scale |

| Basic reminder automation | Messages follow predefined triggers and schedules | Often remains static and channel-specific |

| Omnichannel first-party recovery | Data, segmentation, decisioning, channels, self-service, and human support work together | Requires technology and operational expertise |

Basic automation may be enough for a small volume of straightforward invoices. But at higher volumes, the challenge changes.

The question is no longer: Can we send the reminder?

It becomes:

- Are we contacting the right accounts?

- Are we repeating ineffective actions?

- Are channels coordinated?

- Is customer behavior changing the strategy?

- Can customers resolve balances immediately?

- Are complex cases reaching the right people?

That is why larger organizations often need more than another invoice reminder tool.

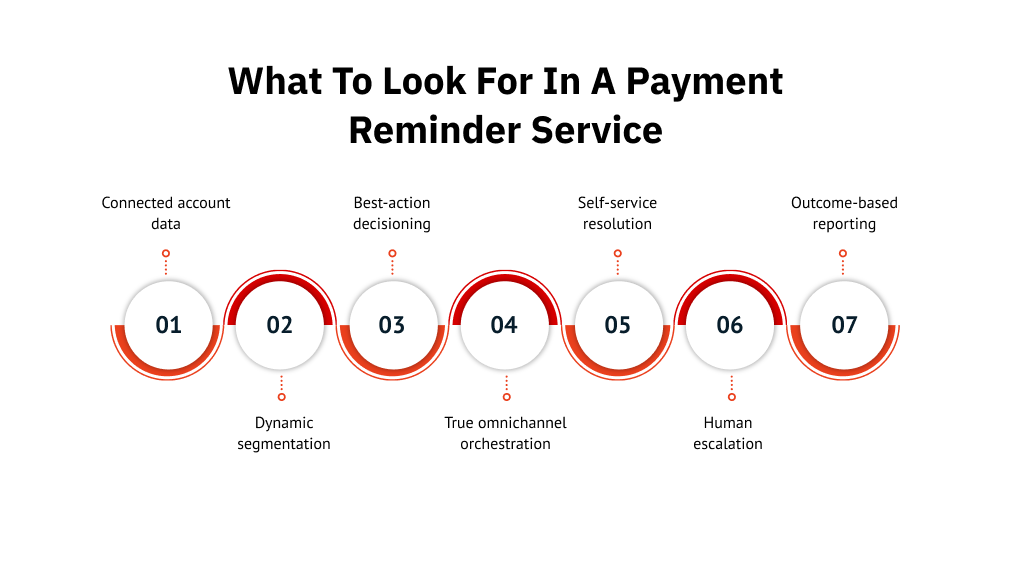

What To Look for in a Payment Reminder Service

The important question is not how many reminder templates a provider offers. It is whether the recovery infrastructure can adapt as accounts and customer behavior change. Here is what to consider:

1. Connected account data

First, the service should work with your relevant systems, so outreach reflects current account information. Ask how data moves between systems and how account updates affect outreach.

2. Dynamic segmentation

Next, determine whether different accounts receive different treatment based on payment behavior, delinquency stage, responsiveness, and engagement.

3. Best-action decisioning

Then, look at what happens after a customer interacts. Does the original sequence continue, or can the treatment adapt?

4. True omnichannel orchestration

Email, SMS, phone, chat, and self-service should work as one coordinated journey. Ask how the provider prevents duplicate or conflicting outreach.

5. Self-service resolution

Customers should also have a mobile-friendly way to take available actions without unnecessary agent involvement.

6. Human escalation

When digital outreach is not enough, there should be a clear path to agent support. Ask when accounts are escalated and whether agents receive the context of previous interactions.

7. Outcome-based reporting

Finally, do not judge performance by message volume alone. Useful reporting should show:

- Recovery performance.

- Payment conversion.

- Engagement by channel.

- Roll rates.

- Self-service activity.

- Agent escalation.

- Performance by segment or treatment.

The goal is to understand what actually moved accounts toward resolution.

Compliance Needs to Be Built into the Workflow

Adding more channels can improve reach, but it also increases operational and compliance complexity. The applicable rules may depend on the organization’s role, the type of debt, the communication method, and the jurisdiction.

That is why compliance needs to be built into the workflow from the start.

An effective recovery program should manage:

- Communication preferences.

- Consent and revocation were applicable.

- Opt-out handling.

- Account status changes.

- Disputes and special workflows.

- Communication records and audit trails.

- Applicable federal and state requirements.

As portfolios grow and more channels are added, these controls need to work across the entire recovery journey, not in separate systems.

FCS integrates these safeguards into its broader recovery approach. It combines operational controls, documentation, and oversight to support compliant customer engagement. Learn more about its debt collection compliance practices.

Why Managed Payment Reminder Services Can Outperform Another Standalone Tool

Buying software and running a recovery operation are not the same thing. A platform can provide automation, but someone still needs to:

- Integrate the data.

- Build segmentation logic.

- Design workflows.

- Set escalation rules.

- Coordinate channels.

- Monitor performance.

- Adjust the strategy.

- Handle exceptions.

For organizations with mature internal teams, owning that work may make sense. However, for high-volume organizations with limited capacity, a managed model can remove much of the operational burden.

The edge is clear:

A software vendor gives you a system to operate. A managed payment follow-up service combines the technology with the people and processes needed to run the program.

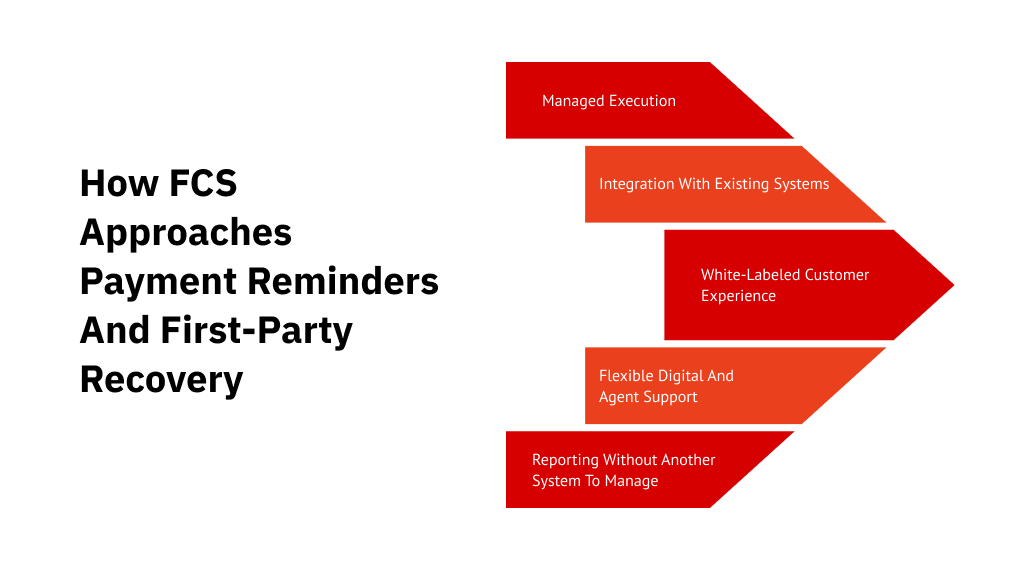

How FCS Approaches Payment Reminders and First-Party Recovery

FCS approaches first-party recovery as a managed service rather than another platform for internal teams to operate.

Its Unified Consumer Engagement Platform (UCEP) sits behind the recovery program, while FCS handles the day-to-day execution. That includes integration, workflow setup, outreach management, reporting, and ongoing program adjustments.

The model adds value in several ways:

1. Managed execution

Clients do not need to log into UCEP or manage campaigns themselves. FCS runs the program on their behalf, which can reduce the operational burden on internal billing and collections teams.

2. Integration with existing systems

Depending on the client’s environment, data can flow through APIs, SFTP, or other agreed methods. This allows the recovery program to work with existing systems rather than requiring a full replacement.

3. White-labeled customer experience

For first-party programs, communication and the payment experience can remain under the client’s brand. Customers move from outreach into a personalized portal without an obvious third-party handoff.

4. Flexible digital and agent support

Customers can resolve straightforward balances through self-service. On the other hand, calls and chats can be routed to either client teams or FCS agents based on the operating model.

5. Reporting without another system to manage

Clients receive reporting and dashboards based on the available data while FCS continues to operate the underlying platform.

Move Beyond Sending More Reminders

When a customer ignores a reminder, the answer is not always to send more of the same. They may need a different channel, better timing, an easier way to pay, or human support. That is where modern payment reminder services become more effective.

Instead of relying on a fixed cadence, they combine account data, AI-driven best action, segmentation, omnichannel outreach, self-service, and agent support to guide each account toward resolution. For high-volume organizations, this means moving beyond overdue payment notifications and building a more responsive first-party recovery strategy.

Discuss with FCS to explore a managed, omnichannel approach built around your customers, account volumes, and existing systems.

FAQs

1. How long does it take to launch a managed first-party payment reminder program?

Implementation time depends on the complexity of the data, integrations, workflows, and staffing model. For FCS, a first-party program typically takes 30 to 60 days to launch once requirements and data flows are defined.

2. What happens if an account remains unpaid after first-party outreach?

Accounts that remain unresolved may move into a later-stage recovery process based on the organization’s policies and account criteria. A defined handoff process helps preserve account history and prevents the customer from restarting the journey with no context.

3. How often should a payment reminder strategy be reviewed?

A payment reminder strategy should be reviewed regularly using recovery, engagement, payment, and escalation data. The goal is to identify where customers are dropping off and adjust workflows, timing, channel use, or treatment rules accordingly.

4. Can payment reminder services handle sudden increases in account volume?

Yes, provided the service is designed to scale. A managed model can be especially useful when account volumes rise faster than internal teams can handle, since digital workflows and additional agent support can be adjusted without rebuilding the entire process.

5. What should businesses prepare before outsourcing payment reminder services?

Businesses should be ready to provide relevant account data, system access requirements, communication rules, brand guidelines, escalation criteria, and reporting needs. Clear onboarding requirements help the provider design workflows that fit the existing receivables process.

6. Can payment reminder services work with existing billing and CRM systems?

Yes, depending on the provider and system setup. Integration can allow account updates, payment activity, and customer interactions to flow into the recovery process. This helps keep outreach aligned with current account status without requiring businesses to replace their existing systems.