Patients now owe more of every medical bill than ever, and providers keep losing ground on the part they cannot afford to write off. The KFF’s 2025 Employer Health Benefits Survey found that 34% of covered workers face a single-coverage deductible of $2,000 or more.

So a large and growing share of each bill is owed by the patient before insurance pays a cent. That makes patient balance collections a distinct workstream, not a footnote to payer follow-up.

This guide shows revenue cycle leaders how to recover self-pay balances earlier and more compliantly, without straining the patient relationship. It covers when to collect, how to stay compliant, which metrics matter, and when an early-out partner earns its keep.

What are Patient Balance Collections?

Patient balance collections is the recovery of the patient-responsibility portion of a bill after insurance adjudicates. That portion includes deductibles, copays, and coinsurance. It is the self-pay balance the patient owes directly, separate from any coverage provided by the payer.

This is a different job from payer or claims follow-up. Payer collections seek payment from insurers through claim edits, appeals, and rework of denials. Patient responsibility collections chase money from people, one balance at a time.

The two used to blur together. They do not anymore. When patients owed a sliver of the bill, providers folded it into general billing. Now that patients are often the third-largest payer, medical balance collections needs its own strategy, tone, and metrics. Treating it as an afterthought is how recoverable revenue quietly becomes bad debt.

Why Patient Balances are Harder to Collect Than Ever

Patient balances are harder to collect because the money now sits with people who did not expect the bill, moves slowly through AR, and pays back at a lower rate than payer dollars. Three forces are driving that shift, such as:

- Plan design: High-deductible plans have shifted patients into a primary payer role, resulting in larger self-pay balances across more accounts. When a patient believes insurance covers everything, a bill for the deductible does not feel like an obligation. It feels like a mistake, and mistakes get ignored.

- Speed: Patient dollars are slow dollars. J.P. Morgan’s 2025 report found that 71% of providers say it takes more than 30 days to collect payment after a patient encounter. Phone-only outreach and the slow three-paper-bill cycle make that worse. Statement fatigue sets in, and the patient tunes out.

- Yield: Patients are paying less than they owe, even on the simplest balances. The Cleveland Clinic’s 2025 report mentions that more than half of its copays went unpaid in 2024. If a fixed, known copay goes uncollected at that rate, larger deductible and coinsurance balances fare worse. Self-pay balance collections is where that leakage happens.

AR aging makes all three worse. Collection probability decays as an account ages. A recent balance often needs one clear reminder and an easy way to pay. A balance sitting past 90 or 180 days needs more contact attempts, more documentation, and returns far less.

The exact decay curve varies by specialty and payer mix, but the direction never does: the longer a balance sits, the less of it you get back. This is why healthcare revenue cycle leaders are moving the whole effort earlier.

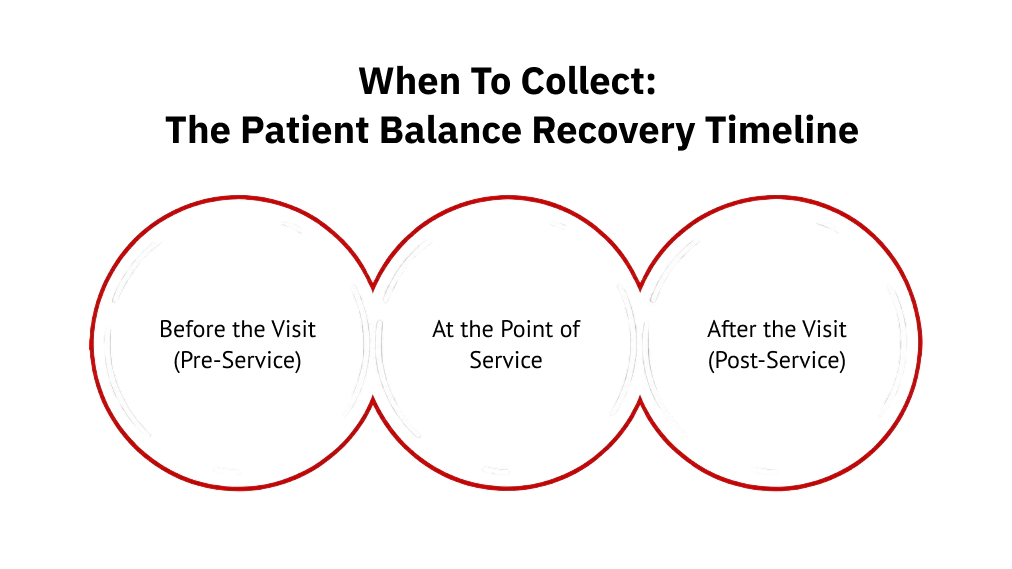

When to Collect: The Patient Balance Recovery Timeline

The best patient balance recovery strategy is a timing strategy. Money you collect early never enters AR, never ages, and never turns into a write-off. The goal is to shift as much of the balance as possible to the front of the encounter and then use fast digital follow-up for whatever remains. Here is how that plays out across three moments.

1. Before the Visit (Pre-Service)

The pre-service window is the highest-leverage moment you have. Run eligibility and benefits checks so patient responsibility is known before the patient arrives. Then act on it.

- Send a clear cost estimate so the balance is no surprise.

- Offer card-on-file enrollment with documented consent.

- Collect deposits or prepayments on known, plannable costs.

Money collected here never enters AR. It is the cheapest dollar you will ever recover.

2. At the Point of Service

The front desk is your second-best moment. Collect known balances and copays at check-in, or through a digital or mobile check-in flow that lets patients pay before they sit down.

Give staff a short, empathetic script for discussing what is owed. The tone matters as much as the ask. Upfront transparency here reduces billing surprises later, which means fewer disputes and fewer angry calls after the statement lands.

3. After the Visit (Post-Service)

Whatever is left after the visit is where most providers still lose ground, usually because they default to paper. Do not. Lead with a digital-first sequence.

- Send text and email reminders with one-tap payment links.

- Route patients to a self-service portal for autopay and payment plan setup.

- Replace the slow three-paper-bill cycle with shorter, coordinated digital sequences.

Every extra statement cycle is you financing your own receivables. A tight digital sequence resolves balances in days, not months.

Building a Patient-Friendly Recovery Process

Patient-friendly recovery is not the soft option. It is an effective one. Patients pay balances they understand, from providers who make paying easy, in a tone that does not feel threatening.

Start with the bill itself. Use plain language, show the service and the amount owed, and back it with price transparency. A patient who understands the charge is far more likely to pay it. A confusing bill just generates a phone call or silence.

Then remove the friction. Offer flexible payment plans and a clear path to financial assistance for patients who qualify. Many patients want to pay but cannot clear the full balance at once. A $600 balance split into manageable monthly payments recovers far more than a single demand that goes unpaid.

Finally, meet patients where they are. Use self-service and omnichannel outreach across text, email, and the portal, on the patient’s channel of choice. This is patient payment recovery that reads as account support, and it is the core of a good patient financial experience.

| Pro Tip:Keep early outreach under your own brand. When patient balance recovery runs through brand-aligned, first-party collections, patients experience reminders and payment links as part of your billing office, not as a third-party handoff. That protects the relationship while the balance is still recoverable. |

Staying Compliant: HIPAA, Regulation F, and Credit Reporting

Patient balance collections sits inside three overlapping rules, and getting any of them wrong turns a recovery program into a liability. This is often the least understood part of the workflow, so it is worth being specific.

Start with the Health Insurance Portability and Accountability Act (HIPAA). Payment and outreach messages should never expose protected health information. A reminder can reference a balance and a due date. It should not name a diagnosis, a procedure, or a provider specialty in a way that reveals the nature of care. Keep PHI out of the collection workflow entirely.

Next is Regulation F, which applies the Fair Debt Collection Practices Act (FDCPA) to the collection of balances. It sets limits on contact frequency, defines required disclosures, and governs how and how often you can reach a patient. Build those contact-cadence and disclosure rules into your outreach sequences from the start, not as an afterthought.

Then there is credit reporting, which changes sharply and confuses many teams.

| Did you know?The Consumer Financial Protection Bureau (CFPB) finalized a rule in January 2025 to remove medical debt from most credit reports. However, the U.S. District Court of the Eastern District of Texas vacated that rule in July 2025. |

Thus, it is no longer in effect. The major bureaus still apply their earlier CFPB voluntary limits: paid medical collections and balances under $500 are removed from reports. Some states add their own restrictions on top of that.

The practical takeaway: assume the rules will keep shifting and run outreach that stays compliant regardless of the reporting landscape. A compliance-aware collections approach is not optional in healthcare. It is the baseline for protecting recovery, patients, and the organization.

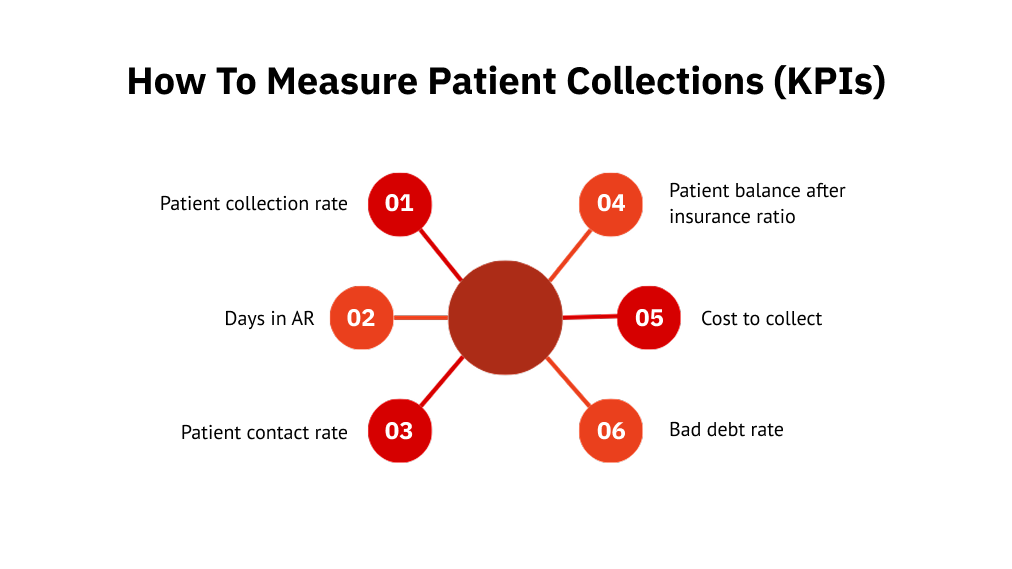

How to Measure Patient Collections (KPIs)

You cannot fix what you do not measure, and patient collections has its own metrics separate from payer performance. The table below gives the core KPIs, how each is calculated, and a directional target. Treat the benchmarks as starting points; healthy ranges vary by specialty, payer mix, and patient population.

| Metric | Formula | Directional Target |

| Patient collection rate | Patient dollars collected / patient dollars owed | Higher is better; track the trend month over month |

| Days in AR | Total AR / average daily net patient revenue | Commonly targeted under 40 to 50 days |

| Patient contact rate | Accounts reached / accounts attempted | Rises with omnichannel outreach |

| Patient balance after insurance ratio | Patient responsibility / total net patient revenue | Watch the trend; it is climbing industry-wide |

| Cost to collect | Collection cost / total dollars collected | Often benchmarked around 2 to 4 percent |

| Bad debt rate | Written-off patient balances / net patient revenue | Lower is better; rising bad debt signals a timing problem |

The pattern to watch is the relationship between them. If days in AR and bad debt are both climbing while your contact rate stays flat, the problem is almost always timing and channel, not effort.

Common Mistakes That Quietly Kill Recovery Rates

Most lost patient revenue does not come from hard cases. It comes from small process gaps that repeat across thousands of accounts. These are the ones that do the most damage:

- Waiting until post-service to mention cost, so the balance is a surprise.

- Relying on paper-only statements that patients ignore.

- Offering no payment plans, so patients who cannot pay in full pay nothing.

- Following up inconsistently, so accounts age with no clear next step.

- Ignoring compliance on outreach cadence, which turns recovery into risk.

Each one is easy to fix on its own. Together, they are the difference between recovering most of what patients owe and writing off the rest.

In-House vs Outsourced Early-Out Recovery

At some point, the question stops being how to collect and becomes who should. Early-out recovery is a patient-friendly follow-up on balances before they charge off, run either by your team or a partner. Deciding between the two comes down to capacity and math.

When an Early-Out or EBO Partner Makes Sense

A few trigger signs tell you the in-house model is running out of room:

- Self-pay volume is rising faster than your staff can keep up with.

- Balances are aging for more than 90 days before anyone reaches the patient.

- Follow-up is inconsistent, with no reliable sequence or cadence.

The deciding factor is the cost-to-collect math. When chasing balances in-house costs more than a contingency partner would recover, the case makes itself. An early-out or EBO recovery adds capacity, consistency, and compliance support without forcing you to give up control of the patient relationship.

First-Party vs Third-Party Patient Recovery

Match the model to the stage of the balance, not the other way around.

First-party or early-out recovery is brand-aligned and patient-friendly. It runs under your name, before write-off, so the patient experience stays intact. This is the right model for recent balances where the relationship still matters.

Third-party recovery runs under the agency’s name after write-off for older, harder-to-recover balances. It is recovery-focused rather than relationship-focused. Use it when early-stage outreach has run its course. The point is to keep both stages connected, so unresolved accounts move forward without rebuilding context at every handoff.

What to Look for in a Recovery Partner

Once you decide to bring in a partner, the evaluation should start with compliance and end with fit. Screen every service provider against the same short list:

- Compliance posture first: HIPAA, PCI DSS, SOC 2, a signed BAA, and Regulation F-aware outreach.

- Omnichannel reach and a patient-experience fit that will not damage your brand.

- Transparent, outcome-aligned pricing and clear reporting visibility.

This is where First Credit Services fits for healthcare teams. It runs early-out and first-party patient recovery entirely under the client’s brand, so patients only ever see your name.

Outreach runs through the Unified Consumer Engagement Platform (UCEP). It is an AI-driven, omnichannel, self-service payment layer that FCS operates on your behalf. UCEP connects to your existing billing system rather than replacing it. Consumers land on a white-labeled portal from a text or email link, then view the balance, pay, or set up a payment plan without calling an agent.

The compliance floor is built in: HIPAA-aware workflows, PCI DSS Level 1, and SOC 2 Type II. Pricing is contingency-based, so you pay when FCS recovers. Balances that age past early-out move into third-party recovery within a single connected lifecycle, so no account falls through the cracks between vendors.

Turn Patient Balances into a Faster, Friendlier Recovery Process

Patient balances are won early, protected by a patient-friendly process, and lost when they sit. Collect before and at the visit, follow up digitally and fast, and stay compliant through every shifting rule. Considering bringing in an early-out partner the moment the cost-to-collect math tips.

Want to recover more patient balances without straining the relationship? FCS runs early-out and first-party patient recovery under your brand, with omnichannel outreach and a compliance-first model.

Discuss with the team about a patient balance recovery program built for your revenue cycle.

FAQs

1. What is a patient balance in medical billing?

A patient balance is the portion of a medical bill the patient owes after insurance pays. It includes the deductible, copay, and coinsurance. It is separate from the amount the insurer covers and is billed directly to the patient.

2. What is the best way to collect patient balances?

Collect as early as possible. Verify responsibility before the visit, ask for known balances at check-in, then use fast digital follow-up with reminders, one-tap payment links, and flexible payment plans. Early, patient-friendly outreach recovers far more than late paper statements.

3. How long do you have before a patient balance becomes bad debt?

There is no fixed deadline, but the probability of collection decreases as an account ages. Most balances that reach 90 to 120 days without contact are much harder to recover, which is why early-out follow-up before write-off matters so much.

4. Does HIPAA apply to patient balance collections?

Yes. Any outreach or payment workflow must protect health information. Reminders can reference a balance and due date, but should not reveal a diagnosis, procedure, or the nature of care. Keeping PHI out of collection messages is a core requirement.

5. What is early-out collection in healthcare?

Early-out collection is a patient-friendly follow-up of self-pay balances before they are charged off, often run by an extended business office partner under the provider’s brand. It adds recovery capacity while the balance is still fresh and the relationship intact.

6. Can unpaid medical bills still affect a patient’s credit?

Sometimes. The 2025 federal rule to remove medical debt from credit reports was vacated, so it is not in effect. The major bureaus still exclude paid collections and balances under $500, and some states impose additional limits, so treatment varies.