Every AR team knows the pattern. Missed payments start small, then follow-ups get delayed, disputes pile up, and aging balances begin to pressure cash flow.

The Federal Reserve’s 2025 report found that 51% of U.S. small businesses cited uneven cash flow as a significant financial challenge. When receivables are followed up late or handled inconsistently, that gap only widens.

That is where accounts receivable management makes the difference. It helps businesses track what is owed, follow up before accounts age, resolve disputes faster, and reduce days sales outstanding, or DSO.

As account volume grows, teams need a process that keeps follow-up consistent, compliant, and customer-conscious across every stage.

This guide breaks down the accounts receivable management process, common roadblocks, best practices, first-party AR support, and when outsourcing makes sense.

Contents

- 1 What Is Accounts Receivable Management?

- 2 The Accounts Receivable Management Process

- 3 Common Accounts Receivable Management Challenges

- 4 Accounts Receivable Management Best Practices

- 4.1 1. Segment Receivables by Age, Balance, And Customer Type

- 4.2 2. Use Early-Stage Reminders Before Accounts Become Severe Delinquencies

- 4.3 3. Offer Convenient Self-Service Payment Options

- 4.4 4. Keep Outreach Brand-Aligned

- 4.5 5. Create Clear Escalation Rules

- 4.6 6. Measure Performance by Lifecycle Stage

- 4.7 7. Structure Payment Plans Early

- 5 Where First-Party Accounts Receivable Management Fits

- 6 When Should Businesses Outsource Accounts Receivable Management?

- 7 How To Choose an Accounts Receivable Management Partner

- 8 Turn Receivables into Recovered Revenue, Without Losing the Customer Relationship

- 9 FAQs

- 9.1 1. Can accounts receivable management software replace a dedicated AR team?

- 9.2 2. What is a good DSO rate?

- 9.3 3. What is the difference between gross and net collections rate?

- 9.4 4. How does accounts receivable management affect borrowing capacity?

- 9.5 5. What happens to accounts receivable balances that are never collected?

- 9.6 6. How should AR teams handle customers who repeatedly miss payment plan commitments?

What Is Accounts Receivable Management?

Accounts receivable management is the process of tracking, managing, and collecting payments owed after invoices, bills, or payment obligations are issued. It covers credit policies, invoicing, reminders, dispute resolution, collections, reporting, and cash-flow forecasting.

A well-run AR process helps teams see who owes money, how old each balance is, what actions have already been taken, why payments are delayed, and what should happen next.

Accounts Receivable Management Vs Collections

Accounts receivable management covers the receivables lifecycle before an account is written off. This includes current balances, failed payments, overdue invoices, disputes, early-stage delinquency, and first-party recovery efforts.

On the other hand, collections refers to recovery activity after the account has been written off or moved out of the active AR process. These accounts are typically older, more delinquent, and may require third-party collections or specialized recovery workflows.

Here are the key differences between them:

| Area | Accounts Receivable Management | Collections |

| Main goal | Prevent avoidable aging and recover balances before write-off | Recover written-off or severely delinquent accounts |

| Timing | Before write-off, including early delinquency | After write-off or late-stage escalation |

| Focus | Billing, follow-up, disputes, payment plans, first-party outreach, reporting | Recovery, negotiation, settlement, third-party escalation |

| Customer impact | Keeps resolution closer to the original customer relationship | Handles accounts that have moved beyond normal AR recovery |

| Ownership | Finance, billing, AR, revenue cycle, or first-party recovery teams | Internal recovery teams or external collection partners |

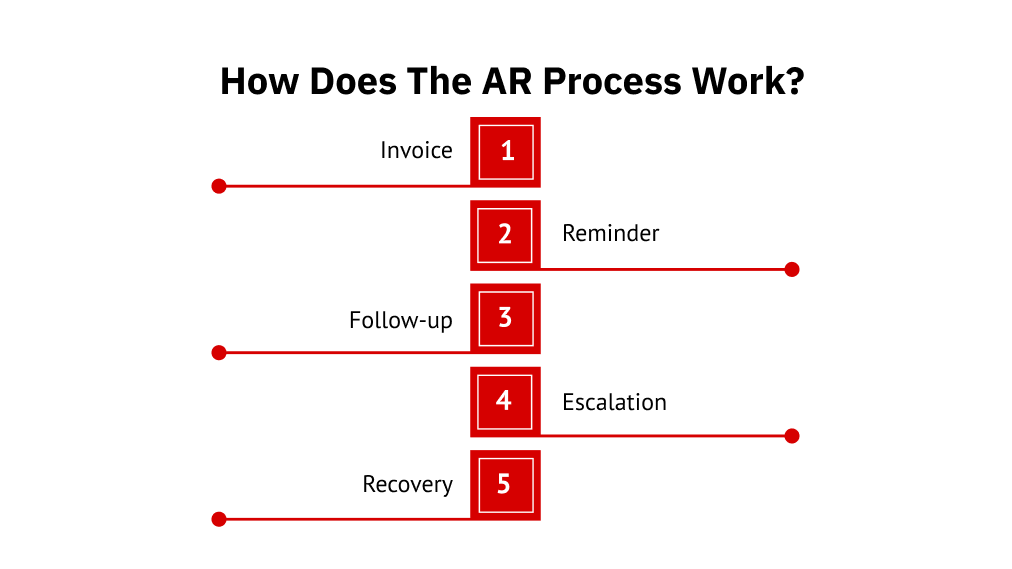

The Accounts Receivable Management Process

AR management works when every stage has an owner, timeline, trigger, and next action, such as:

1. Set Clear Credit and Payment Terms

Your AR policy should define:

- Who qualifies for credit

- Payment due dates

- Grace periods

- Late-fee rules

- Payment plan rules

- Escalation timelines

Unclear terms create disputes, whereas clear terms reduce confusion before payment becomes overdue.

2. Track Payment Status and Aging Buckets

Most AR teams track balances by aging bucket:

- Current

- 1–30 days overdue

- 31–60 days overdue

- 61–90 days overdue

- 90+ days overdue

Each bucket needs a different strategy. A recently failed payment needs a helpful reminder. On the contrary, a 120-day-overdue balance may require stronger escalation.

3. Send Payment Reminders and Follow-Ups

Payment reminders should make the next step easy. Each message should include the balance, due date, payment link, support option, and dispute path.

Use email, SMS, phone, self-service links, chat, or callback options based on customer preference and policy. At this stage, the priority is to remove friction and simplify resolution.

4. Resolve Disputes Quickly

Disputed invoices should not sit in the same queue as non-responsive accounts. They need faster routing, clear ownership, supporting documentation, and a resolution deadline.

Track the dispute reason, customer communication history, internal owner, and final decision. Unresolved disputes inflate AR and weaken cash-flow visibility..

5. Escalate Overdue Accounts

Escalation should follow rules, not team memory. A simple path may look like this:

- Internal AR reminder

- First-party collection outreach

- Payment plan or settlement option

- Third-party collections for severe delinquency or charged-off accounts

This helps you act before balances become harder to collect.

6. Report and Improve

Reporting should show where recovery slows down and what action is needed next. Track DSO, aging balance by bucket, collection rate, dispute volume, promise-to-pay conversion, payment plan completion, bad debt write-offs, and cost to collect.

The goal is to move from “who has not paid?” to “why are accounts getting stuck, and what should change?”

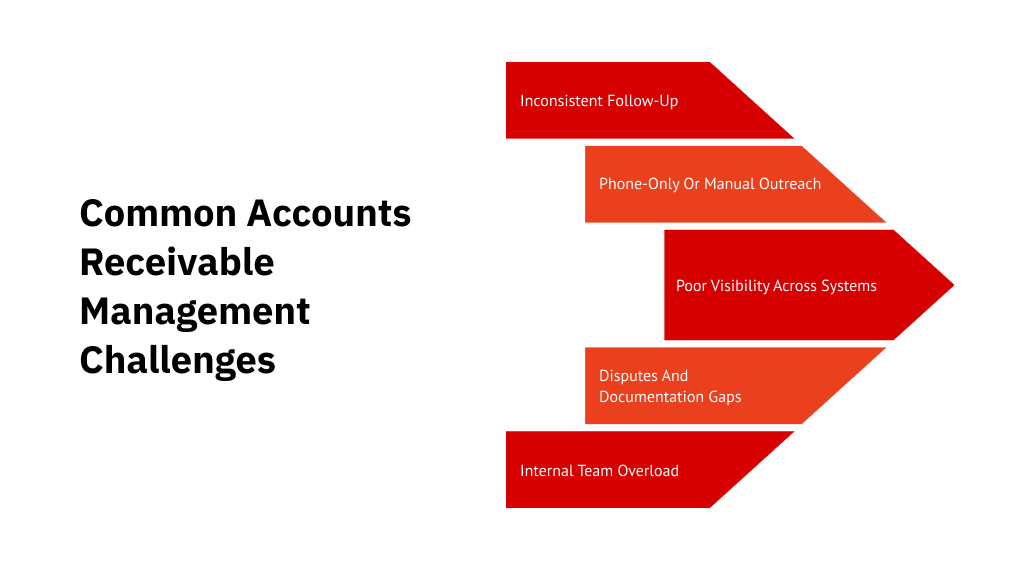

Common Accounts Receivable Management Challenges

Most AR problems come from small gaps that repeat across many accounts. The most common roadblocks are:

1. Inconsistent Follow-Up

Many teams follow up only when balances become large or old. By then, recovery is harder. Each aging bucket needs a defined sequence.

2. Phone-Only or Manual Outreach

Phone calls still matter, but phone-only recovery does not scale well. Customers may ignore unknown numbers, miss voicemails, or prefer digital options. According to the PYMNTS 2024 report, 59% of U.S. businesses said outdated methods limit their ability to manage cash flow and forecast accurately.

The fix is not to stop calling. It is to combine calls with email, SMS, self-service payment links, chat, and clear escalation workflows.

3. Poor Visibility Across Systems

AR data often sits across CRMs, ERPs, billing tools, spreadsheets, payment processors, and support systems. When data is scattered, teams miss follow-ups, duplicate outreach, or lack context during customer conversations.

4. Disputes And Documentation Gaps

Payment delays often come from missing invoices, unclear service records, incomplete account notes, or weak approval trails. When teams cannot quickly verify the balance, the account stays unresolved.

A mature AR process separates true disputes from non-payment. Disputed accounts need documentation, ownership, and resolution timelines, whereas non-responsive accounts need follow-up and escalation.

5. Internal Team Overload

AR teams often manage invoicing, reporting, disputes, payment posting, customer inquiries, and follow-up simultaneously.

As overdue accounts increase, capacity becomes an issue. Reminders go out late, disputes take longer to resolve, and high-risk accounts do not get attention soon enough.

Accounts Receivable Management Best Practices

Effective accounts receivable management starts with early action, clear prioritization, and simple resolution paths for customers. These practices help reduce aging, improve recovery, and keep follow-up customer-friendly.

1. Segment Receivables by Age, Balance, And Customer Type

Not every overdue account needs the same workflow. Segment receivables by days overdue, balance size, customer value, payment history, dispute status, and risk level.

This helps your team decide which accounts need automated reminders, personal follow-up, dispute review, payment-plan support, or escalation.

2. Use Early-Stage Reminders Before Accounts Become Severe Delinquencies

The first few weeks after a missed payment matter most. At this stage, the account is still fresh and easier to resolve.

So, early reminders should make it simple to pay, update payment details, ask a billing question, or request support. For businesses with rising early delinquencies, First Credit Services (FCS)’s first-party collection services can help extend internal AR capacity while keeping outreach brand-aligned.

3. Offer Convenient Self-Service Payment Options

Customers are more likely to respond when payment is easy. Pay-now links, mobile-friendly portals, card or ACH options, payment plans, callback scheduling, and chat reduce the effort needed to resolve a balance.

That way, customers can act when they are ready, and AR teams spend less time manually handling routine payment conversations.

4. Keep Outreach Brand-Aligned

Payment follow-up is still part of the customer experience. The tone, timing, script, and channel used during AR outreach can make or break the trust.

This is especially important in healthcare, fintech, banking, subscriptions, utilities, and fitness, where payment recovery is not the end of the relationship. The way you follow up can influence whether the customer continues care, renews a service, restores an account, or stays loyal after the balance is resolved.

5. Create Clear Escalation Rules

Escalation should not depend on manual judgment alone. It should follow a stage-based approach like this:

| Stage | Action |

| Before due date | Friendly reminder |

| 1–15 days overdue | Digital reminder with payment link |

| 16–30 days overdue | Follow-up plus support option |

| 31–60 days overdue | First-party AR collections |

| 61–90 days overdue | Payment plan, dispute review, or escalation |

| 90+ days overdue | Third-party collections or specialized recovery |

The timeline may vary by industry, but every stage should have a defined next step.

6. Measure Performance by Lifecycle Stage

Total collections do not show where accounts slow down. Track DSO, recovery rate by delinquency stage, contact rate, response rate, payment-plan completion, dispute resolution time, and bad debt write-offs.

It helps you identify whether the issue is weak follow-up, slow dispute handling, poor payment-plan design, limited digital options, or delayed escalation.

7. Structure Payment Plans Early

Payment plans help customers resolve balances when full payment is not possible. They should define the amount, frequency, start date, handling of failed payments, reminder cadence, and escalation rule.

FCS’s Unified Consumer Experience Platform (UCEP) facilitates this through a white-labeled consumer portal. Customers can view balances, choose weekly or monthly payment plans, accept offers, schedule callbacks, or start a chat, while the experience stays aligned with the client’s brand.

Where First-Party Accounts Receivable Management Fits

First-party accounts receivable management helps businesses recover overdue balances under the original brand. It is most useful when accounts are still early enough to resolve without affecting the customer relationship.

What Is First-Party Accounts Receivable Management?

First-party accounts receivable management means managing overdue payment outreach under the original business’s name. It can be handled by an internal team or by an outsourced partner acting as an extension of the brand.

It is often used for:

- Early-stage AR management

- Failed payments

- Overdue invoices

- Subscription recovery

- Healthcare billing

- Customer-friendly payment recovery

When To Use First-Party AR Collections

First-party AR collections are most useful when overdue accounts are still recoverable, and the customer relationship is worth protecting.

They work well for early-stage or pre-charge-off accounts, failed payments, overdue invoices, and customers who need flexible payment options. They also help when internal teams lack capacity or phone-only outreach is no longer enough.

How First-Party AR Management Differs from Third-Party Collections

First-party AR management usually happens earlier. Outreach happens under the original business’s brand and focuses on reminders, failed-payment recovery, payment plans, and dispute routing.

Third-party collections usually apply to severe delinquency, aged portfolios, charged-off accounts, or accounts that have moved beyond internal recovery.

How FCS Supports First-Party AR Recovery at Scale

FCS supports outsourced first-party AR management for high-volume businesses that need more than invoice follow-up.

Through UCEP, FCS brings coordinated outreach, payment options, reporting, and escalation together as a managed service, not self-serve software. Clients do not have to run campaigns or manage the platform internally.

In first-party mode, consumers interact with the client’s brand through a white-labeled experience. They can receive outreach through SMS, email, chat, phone, or portal-based workflows, then view balances, pay now, choose payment plans, accept offers, schedule callbacks, or start a chat.

This model fits mid-sized to enterprise organizations with large account volumes, multi-location operations, or complex receivables portfolios.

When Should Businesses Outsource Accounts Receivable Management?

Outsourcing does not mean losing control. It means adding capacity, workflow discipline, technology, and specialized recovery support when internal teams cannot scale consistently.

Signs Your AR Process Is Ready for Outsourcing

Consider outsourcing if:

- Delinquent accounts are growing faster than staff capacity

- Follow-ups are inconsistent

- Customers ignore phone-only outreach

- Disputes are slowing resolution

- AR teams spend too much time chasing balances

- DSO is increasing

- Failed payments are driving churn

- Compliance concerns are increasing

- Leadership needs better recovery visibility

The clearest signal is operational strain. Your team knows what should happen, but cannot execute it consistently across account volume.

What Outsourced First-Party AR Management Can Handle

An outsourced first-party AR partner can support payment reminders, failed-payment recovery, customer outreach, dispute routing, payment-plan support, account segmentation, reporting, escalation workflows, and customer-service-style recovery conversations.

The right partner should feel like an extension of your AR, billing, or revenue cycle team.

In-House AR vs. Outsourced First-Party AR Management

In-house AR gives you direct control, but it can become harder to scale as overdue accounts, disputes, and follow-ups increase. Outsourced first-party AR management adds capacity and structured recovery support while keeping outreach aligned with your brand.

Here’s how the two models compare:

| Factor | In-house AR | Outsourced first-party AR management |

| Control | Direct internal control | Shared operating model |

| Scalability | Limited by team size | Easier to scale with volume |

| Customer experience | Depends on internal bandwidth | Can be scripted and brand-aligned |

| Technology | Depends on internal tools | Partner may bring outreach, portal, and reporting workflows |

| Best fit | Lower volume or simple AR | High-volume, recurring, or multi-location receivables |

| Limitation | Can become inconsistent | Requires onboarding and clear workflows |

Many businesses keep billing and finance in-house while outsourcing early-stage outreach, failed-payment recovery, or overflow support.

How To Choose an Accounts Receivable Management Partner

The right accounts receivable management partner should improve recovery without creating brand, compliance, or reporting risk. Look beyond basic collection activity and evaluate how the partner will manage outreach, customer experience, escalation, and visibility.

1. Look For Lifecycle Support

Many businesses need early-stage recovery first, then escalation for unresolved accounts. A partner that supports both first-party and third-party recovery can reduce handoff gaps and keep accounts moving through the receivables lifecycle.

This is useful when some accounts need a soft reminder, some need payment-plan support, and others eventually need formal collections.

2. Check Brand-Alignment Capabilities

Brand alignment is critical when the customer relationship still matters. Your partner should be able to operate as an extension of your business, not as a disconnected recovery vendor.

Ask whether they can:

- Operate under your brand in first-party mode

- Use approved scripts and tone guidelines

- Reflect your brand in the payment portal

- Configure chat or phone routing

- Adjust outreach by account stage, customer type, or risk level

The goal is simple: customers should receive clear, respectful communication that feels consistent with your brand.

3. Review Digital Engagement Capabilities

Modern AR management should not depend only on phone calls. Customers need multiple ways to respond, pay, ask questions, or request support.

So, evaluate whether the provider offers SMS and email outreach, phone and chat support, self-service payment portals, payment links, payment plans, reporting dashboards, and clear escalation workflows.

4. Confirm Compliance Controls

AR outreach should be documented, auditable, and aligned with applicable rules. This is especially important in regulated industries such as healthcare, fintech, consumer lending, utilities, and financial services.

Ask how the provider manages communication records, script approvals, dispute documentation, payment plan records, escalation notes, and reporting access. FCS also emphasizes compliant recovery practices as part of its receivables and collections approach.

5. Ask About Onboarding and Reporting

Implementation quality affects recovery performance. Before choosing a partner, clarify data transfer, system compatibility, reporting, dispute resolution, payment plan tracking, and communication approvals.

Good onboarding gives both teams clear ownership, clean data, defined workflows, and better visibility from day one.

Turn Receivables into Recovered Revenue, Without Losing the Customer Relationship

Every overdue receivable creates a choice: recover it early with control or let it age into a costlier problem.

That is why accounts receivable management needs structure. Timely outreach, simple payment paths, clear escalation, and brand-aligned communication help resolve accounts before they become harder to collect.

For high-volume businesses, FCS brings that structure through managed first-party AR recovery powered by UCEP, helping teams replace scattered follow-up with coordinated recovery across digital channels, trained agents, and self-service payment options.

If rising delinquencies are putting revenue at risk, FCS can help you regain control of your AR recovery strategy. Get in touch with us.

FAQs

1. Can accounts receivable management software replace a dedicated AR team?

No. AR software can automate reminders, reporting, payment tracking, and account prioritization. Teams are still needed for disputes, sensitive conversations, exceptions, payment negotiations, and escalation decisions.

2. What is a good DSO rate?

A DSO under 45 days is generally healthy, but benchmarks vary by industry and payment terms. Retail and subscription businesses usually target lower DSO, while healthcare, lending, and B2B companies may target higher DSO.

3. What is the difference between gross and net collections rate?

The gross collection rate measures total payments collected against total billed. Net collections rate adjusts for contractual allowances, write-offs, discounts, and other non-collectible amounts to show how much collectible revenue was recovered.

4. How does accounts receivable management affect borrowing capacity?

Lenders review AR aging, DSO, and bad-debt levels to assess cash-flow quality. High overdue balances, rising write-offs, or weak collections can make the business look riskier.

5. What happens to accounts receivable balances that are never collected?

Uncollected balances are usually written off as bad debt after a set aging period. They may also be escalated to third-party collections, placed into a recovery portfolio, or handled through settlement.

6. How should AR teams handle customers who repeatedly miss payment plan commitments?

Review the plan, identify why payments were missed, and offer one realistic restructure if the account is still recoverable. Repeated broken commitments should trigger escalation rules.