")

Early-stage collections outsourcing is the practice of hiring an external partner to work pre-charge-off accounts, typically 0 to 120 days past due, under your own brand. Your customers deal with a white-labeled program and never see the partner’s name. The goal is to recover overdue revenue while the account is still curable and the relationship intact.

That window matters. According to the Federal Reserve Bank of New York Household Debt and Credit Report Q1 2025, 4.3% of consumer debt was delinquent, up from 3.6% the prior quarter. Recovery odds are highest in the first days late and fall as accounts age.

This guide covers what the model is, how it differs from third-party collections, when internal teams hit their limit, and what to evaluate in a partner.

Contents

- 1 What Is Early-Stage Collections Outsourcing?

- 2 Early-Stage vs Third-Party Collections: Why the Distinction Matters

- 3 Four Signs Your Internal Team Has Hit Its Limit

- 4 What to Look for in an Early-Stage Collections Partner

- 5 The Lifecycle Question: What Happens When Early-Stage Recovery Isn’t Enough

- 6 Industries Where Early-Stage Outsourcing Has the Highest ROI

- 7 What a Strong Early-Stage Program Looks Like in Practice

- 8 Conclusion

- 9 FAQs

- 9.1 1. What does early-stage collections outsourcing typically cost?

- 9.2 2. Will outsourced early-stage collections report accounts to the credit bureaus?

- 9.3 3. Can an early-stage partner integrate with our existing billing or CRM system?

- 9.4 4. How do we keep control of the customer experience when outreach is white-labeled?

- 9.5 5. What happens to disputes raised during early-stage outreach?

- 9.6 6. Is early-stage outsourcing worth it for smaller account volumes?

What Is Early-Stage Collections Outsourcing?

Early stage collections outsourcing means engaging an external partner to manage pre-charge-off accounts, typically 0 to 120 days past due, entirely under the creditor’s own brand. Consumers get texts, emails, and calls that carry your name and your payment portal, and never learn a third party is involved. The objective is to resolve balances before they age into the harder-to-collect, later-stage phase.

Three details define the model:

- Scope. Accounts are worked from 0 to 120 days past due, before charge-off. This is the first-party window, sometimes called early-out outsourcing.

- Brand. Every touchpoint is white-labeled: the portal URL, the email sender name, and the agent greeting all present as your business.

- Intent. The program preserves the customer relationship, not just the payment. Outreach is service-led, because the person is often still an active customer.

One point buyers miss: the first-party model carries a real but narrow regulatory advantage. Under the Fair Debt Collection Practices Act, a partner collecting in your name is generally not classified as a “debt collector,” so the strictest third-party provisions do not apply the same way. TCPA, UDAAP, and state rules still bind you.

Early-Stage vs Third-Party Collections: Why the Distinction Matters

The difference between early-stage and third-party collections is that it changes the brand your customer sees, the compliance regime you sit under, and the odds you actually recover the money. Confusing the two leads teams to escalate too early and torch relationships they could have saved.

Here is the side-by-side view.

| Model | Timing (DPD) | Brand used | FDCPA classification | Typical recovery goal | Customer relationship impact |

| Early stage (first-party) | 0 to 120, pre-charge-off | Your brand (white-label) | Generally exempt as a first-party creditor extension | Cure the account, retain the customer | Preserved; outreach is service-led |

| Third-party | Post-charge-off or escalated | Agency’s own name | Full FDCPA obligations apply | Recover what remains on an aged balance | Higher friction; relationship usually ends |

Early-stage recovery leans on probability. A customer 20 days late has usually just forgotten, changed a card, or hit a short cash gap. Reach them on the right channel, and most will resolve without any friction. A customer 200 days past charge-off is a different situation entirely, and the brand-safe, relationship-first playbook no longer applies.

The handoff point is where strategy lives. Accounts should move from first-party to third-party when the early-stage effort has genuinely run its course, not on a fixed calendar. That usually means the account has passed the pre-charge-off window, repeated compliant outreach across channels has failed, and the balance is heading for write-off. Escalating before that point sacrifices recoverable, relationship-safe accounts. Escalating too late leaves aged debt sitting past the stage where an agency can act on it.

| Pro tip: Do not set your escalation trigger by day count alone. Tie it to attempt history and channel coverage. An account that has had two calls and no digital outreach has not been worked, only touched. Escalating it wastes a recoverable balance. |

Four Signs Your Internal Team Has Hit Its Limit

Internal teams rarely fail all at once. The strain shows up as slipping metrics before anyone calls it a capacity problem. These four signs, ranked by how much revenue they put at risk, tell you the early-stage window is closing faster than your team can work it.

1. Delinquency Volume Is Outpacing Internal Capacity

This is the most expensive failure because it hits the accounts most likely to cure. Watch for two symptoms:

- DPD buckets are rising, and new delinquencies are not being touched within the first 15 to 30 days.

- Follow-up cadence is falling below your own service-level agreements, so accounts that should get three contacts in week one get one.

Every day an account sits unworked in that early window, its recovery odds drop. When volume grows faster than headcount, the newest and most curable accounts are the ones that wait.

2. Recovery Rates Are Declining Despite Consistent Effort

Your team is working just as hard, but the numbers are sliding. Two patterns confirm it:

- Right-party contact rates fall as volume scales, because a fixed-size team spreads the same effort across more accounts.

- Fewer accounts resolve without escalation, so more balances roll into later, lower-yield stages.

Flat effort against rising volume always shows up as declining yield first. Your team is doing the work. The arithmetic has simply moved against them.

3. Outreach Is Still Call-Only

If your early-stage workflow is a phone queue, you are missing most of your customers.

- There is no SMS, email, or self-service portal in the early-stage sequence.

- Younger and digital-first customers do not answer unknown calls, so a call-only program never reaches them.

Channel drives contact rate, not just customer preference. Customers who ignore the phone still open a text and click a payment link.

4. Compliance Risk Is Growing With Scale

The larger the team and the volume, the harder consistency gets, and consistency is what keeps you compliant.

- TCPA consent tracking starts breaking down at volume, and consent status gets harder to verify per account.

- Script adherence becomes harder to audit as the team grows, so variance creeps into what agents actually say.

A compliance gap does not announce itself. It sits quiet until a complaint or an exam surfaces it, and by then the exposure is already built.

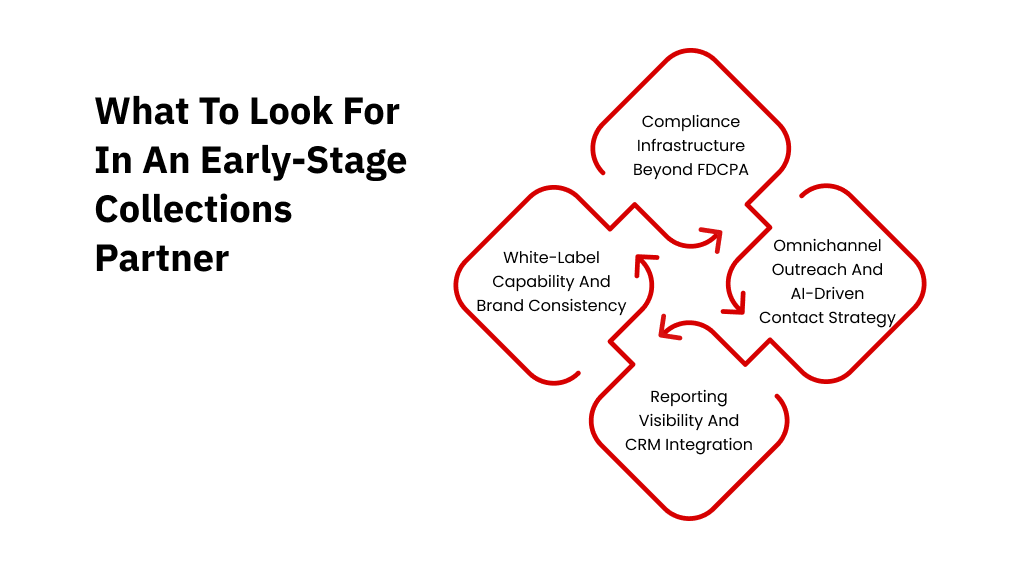

What to Look for in an Early-Stage Collections Partner

This is the section that decides your outcome. Two partners can both claim “first-party early-stage collections” and deliver completely different results. The difference is in four areas: how deep their white labeling actually goes, what their compliance infrastructure looks like beyond the FDCPA exemption, whether their outreach is genuinely omnichannel, and how much visibility you get into live performance.

White-Label Capability and Brand Consistency

White-label is the entire premise of first-party recovery, so test how far it really goes. Many vendors define “white-label” as using your name in an agent’s script. That is the shallow version. The consumer-facing experience should be fully under your brand across every touchpoint.

Evaluate the touchpoints your customer actually sees:

- Payment portal URL and design: Does it carry your branding, or does it route to a generic vendor domain?

- Email sender name and address: Does the email come from your business or from the agency?

- Agent greeting and disclosure language: Does the agent open as your brand?

Ask one direct question: Does the partner have a genuine white-label portal with custom branding, or do they just use your name in scripts? The gap between those two answers is the gap between a customer who feels handled by you and one who feels handed off.

First Credit Services runs its consumer portal as a fully white-labeled experience. Customers arrive through branded SMS or email links, then view balances and pay or set up a plan without needing an account number and without ever seeing the First Credit Services name.

Compliance Infrastructure Beyond FDCPA

The first-party FDCPA exemption is real, but it is not a compliance blank check. Treating it as one is how programs get into trouble.

Several regimes still apply in full:

- TCPA: Texting and autodialed calling require documented, current consent. Ask the partner exactly how consent is captured, stored, and honored at scale, not whether they “handle TCPA.”

- UDAAP: Unfair, deceptive, or abusive practices rules apply regardless of who is collecting or under whose name.

- State rules: Licensing, contact frequency, and disclosure requirements vary by state, and multi-state portfolios have to satisfy all of them.

Certifications tell you whether the infrastructure is real. Look for the ones your vertical demands:

- HIPAA for healthcare data

- PCI DSS for payment card handling

- SOC 2 Type II for data security controls

Then ask what their audit trail actually contains. A serious partner can show you call monitoring, script-adherence tracking, and dispute documentation on demand. First Credit Services is HIPAA, PCI DSS Level 1, and SOC 2 Type II compliant, and operates within FDCPA and TCPA frameworks with live and recorded call auditing and ongoing internal audits.

| Compliance is infrastructure, not a checkbox. See how First Credit Services structures its debt collection compliance program across call auditing, agent training, and automated monitoring. |

Omnichannel Outreach and AI-Driven Contact Strategy

Phone-only programs underperform on early-stage accounts, and the industry has shifted hard toward digital self-service. According to TransUnion’s 2025 Debt Collection Industry Report, the share of collection operations using a consumer self-service portal rose from 79% to 88% in 2024. Reaching people where they already are is the single cheapest lever in recovery.

What separates a real omnichannel program from a checklist:

- Channel breadth. SMS, email, and a self-service portal work alongside phone, not as an afterthought.

- AI-driven segmentation. The platform should decide which channel and which timing fit each account, rather than pushing everyone through one fixed sequence.

- A self-service portal as a conversion point. Give customers 24/7 access to balances, payment plans, and settlement options, and many will resolve on their own with no agent involved.

Ask whether the platform actually chooses per account, or whether “omnichannel” just means the same message sent three ways. A strong platform scores each account and picks the message, channel, and time most likely to land, so many early-stage accounts resolve through the self-service portal without an agent involved. First Credit Services is one provider that runs this kind of AI-driven, digital-first outreach across SMS, email, chat, and phone.

Reporting Visibility and CRM Integration

You cannot manage placements you cannot see. The difference between real-time dashboards and batch reporting is the difference between adjusting a live program and reading a post-mortem.

Confirm what the client actually sees, not just what gets promised:

- Contact rates, resolution rates, DPD-bucket movement, and payment conversion, updated live

- Whether reporting is real-time or a weekly file drop

- How data flows back to you: SFTP, API, or direct CRM sync, and how often

Five reporting questions to ask any vendor before you sign:

- Is the dashboard near real-time, or is it batched? On what cadence?

- Which metrics can I see per account, per placement, and per DPD bucket?

- How does account and payment data sync back to my system, and how frequently?

- Can I see attempt history and channel coverage per account?

- What does the compliance and dispute audit trail look like from my side?

If a vendor cannot answer these cleanly, you will be flying blind on the accounts you care most about.

The Lifecycle Question: What Happens When Early-Stage Recovery Isn’t Enough

Some accounts will not cure in the early-stage window, and your plan for those is a real evaluation criterion. This is where the two-vendor model quietly costs you money.

Run early-stage with one partner and third-party with another, and every escalation becomes a handoff. That handoff means:

- Duplicate onboarding, because the second vendor has to be set up from scratch.

- Lost account history, because communication logs and payment context rarely transfer cleanly.

- Compliance gaps at the seam, because consent records and dispute notes can fall through the crack between two systems.

A single-partner model removes the seam. When early-stage escalates to third-party inside one platform, the account carries its communication history, behavioral data, and payment context with it. The agency picking it up already knows which channels the customer responds to and what was already offered.

Ask this during evaluation: “If an account does not resolve, what happens to the data when it escalates?” The answer tells you whether you are buying one continuous recovery process or two disconnected ones.

First Credit Services runs both first-party and third-party collections on one platform, so accounts that need to escalate transition without rebuilding recovery context from zero.

Industries Where Early-Stage Outsourcing Has the Highest ROI

Early-stage outsourcing pays off everywhere, but three verticals see outsized returns because their economics reward early, brand-safe intervention.

Healthcare and Revenue Cycle

Patient balances are relationship-sensitive in a way few other debts are. The same person is a patient you want back, so aggressive outreach costs you more than the balance is worth. Early, respectful, compliant contact resolves balances before they harden into bad-debt write-offs, and before the account crosses into more complex territory.

For this vertical, HIPAA certification is non-negotiable. Also ask a sharper question: does the partner have real experience with insurance-coordination disputes and patient-hardship workflows? A $480 balance a patient believes their insurer should have covered needs a different conversation than a simple missed payment. First Credit Services supports healthcare revenue cycle work through its Extended Business Office services, built for that patient-sensitive early-stage window.

Auto Finance and Consumer Lending

Auto and consumer lending run high account volumes against tight DPD windows, so internal teams fall behind fast. Here, early outsourcing is an operational-efficiency play as much as a recovery play. You are buying the capacity to work every early account on time, not just the ones your team gets to.

The compliance load is heavy. TCPA consent tracking has to hold at scale, and state licensing requirements stack up market by market. A partner that already carries multi-state licensing and documented consent management removes a genuine operational burden.

Subscription and SaaS Businesses

Failed-payment recovery is early-stage collections under a different name. A card expires, or a charge fails, and the goal is to recover the revenue before the customer churns, not after. The clock is short, and the stakes are retention, not just the invoice.

Brand sensitivity peaks here. The customer has barely been delinquent, often through no fault of their own, and heavy-handed outreach destroys the relationship you are trying to keep. A dunning message that reads like a collections notice can cost you a subscriber worth far more than the failed charge. White-label, service-led outreach is the whole game.

What a Strong Early-Stage Program Looks Like in Practice

First Credit Services runs fully managed early-stage and lifecycle recovery, with both agents and digital engagement operating entirely under the client’s brand. The model is built to recover the early window at scale while keeping the customer relationship intact.

Here is how it works in practice:

- Onboarding. You provide account data and brand guidelines. First Credit Services handles integration, script development, and compliance review, with go-live typically within a few weeks.

- White-label portal. Customers arrive through branded SMS or email links. They view balances, make payments, or set up plans with no account number required and no First Credit Services branding visible anywhere.

- Flexible routing. Chat and phone can route to First Credit Services agents or to your own internal team, and that split can be adjusted during the engagement.

- The platform. UCEP orchestrates omnichannel outreach and feeds real-time activity to your dashboards, so you see contact and resolution data as it happens.

- Compliance. FDCPA-aligned practices run across all first-party programs, backed by HIPAA, PCI DSS Level 1, and SOC 2 Type II certification for regulated sectors.

First Credit Services is one example of this model in practice. It runs managed early-stage recovery under the client’s brand, routes chat and phone to its own agents or your internal team as you prefer and uses a digital engagement platform to feed live activity back to your dashboards. For regulated sectors, it holds HIPAA, PCI DSS Level 1, and SOC 2 Type II certification.

Conclusion

Early-stage collections outsourcing is the highest-leverage move available in receivables, because it works the accounts with the best odds and protects the relationships worth keeping. The real decision is which partner to trust with that window. Look for white-labeling that is genuine, compliance infrastructure that holds at scale, outreach that is truly omnichannel, and reporting that lets you manage the program live. The single-partner lifecycle model matters too, so accounts escalate without losing their history.

See what recovery looks like on your accounts.

Talk to First Credit Services about your early-stage volume, your verticals, and your compliance requirements, and get a program mapped to your portfolio.

FAQs

1. What does early-stage collections outsourcing typically cost?

Early-stage first-party programs are usually priced hourly or on low contingency rates, since these accounts are more recoverable than aged debt. First Credit Services runs collections on contingency, so you pay when it recovers.

2. Will outsourced early-stage collections report accounts to the credit bureaus?

Early-stage first-party outreach is generally about curing the account before it ages, not bureau reporting. Reporting decisions stay with you as the creditor. Confirm the policy with any partner before launch.

3. Can an early-stage partner integrate with our existing billing or CRM system?

Yes. Established partners connect through SFTP, API, or direct CRM sync. Ask how often data flows back and whether updates are real-time, because batch-only reporting limits how actively you can manage placements.

4. How do we keep control of the customer experience when outreach is white-labeled?

You set the brand guidelines, tone, and disclosure language, and approve the scripts. A genuine white-label partner runs the portal, emails, and agent greetings under your brand, so the experience stays yours.

5. What happens to disputes raised during early-stage outreach?

Disputes should be documented and routed back to you per your policy. Ask to see the partner’s dispute audit trail during evaluation, since clean documentation protects you under UDAAP and state rules.

6. Is early-stage outsourcing worth it for smaller account volumes?

It can be, if your internal team cannot work early accounts within the first 15 to 30 days. The value is contacting curable accounts on time, which matters at any volume where capacity is the constraint.