In the first quarter of 2026, U.S. households were carrying $18.8 trillion in debt, and about 4.8% of those balances were already in some stage of delinquency, according to the New York Fed. For the businesses owed that money, the problem is rarely one bad quarter. It is a steady flow of overdue accounts that internal teams cannot work fast enough to keep up with.

Phone-only follow-up does not perform the way it once did. People screen calls, skip voicemails, and pay on their own schedule through text, email, and self-service links. And the clock works against you: the longer an account sits unworked, the lower the odds of ever recovering it.

That gap is what revenue recovery services are built to close. This guide breaks down what these programs actually cover, how the recovery lifecycle works at each stage of delinquency, what a strong managed program should include, and the exact questions to ask before you choose a partner.

Contents

- 1 What Are Revenue Recovery Services?

- 2 Why Internal AR Teams Struggle to Keep Up

- 3 How the Revenue Recovery Lifecycle Works

- 4 Types of Revenue Recovery Services and What Each Model Covers

- 5 What a Managed Recovery Program Should Actually Include

- 6 Compliance Is Built In, Not an Add-On

- 7 How to Evaluate a Revenue Recovery Partner

- 8 How First Credit Services (FCS) Approaches Revenue Recovery

- 9 Conclusion

- 10 FAQs

- 10.1 1. What is the difference between revenue recovery services and debt collection?

- 10.2 2. How much do revenue recovery services typically cost?

- 10.3 3. At what delinquency stage should a business bring in a recovery partner?

- 10.4 4. Will outreach from a recovery partner damage our customer relationships?

- 10.5 5. Do revenue recovery partners report to the credit bureaus?

- 10.6 6. How long does it take to see results from a managed recovery program?

What Are Revenue Recovery Services?

Revenue recovery services are managed programs that help a business collect revenue it has earned but not received. That lost revenue shows up in a few forms: failed or declined payments, delinquent receivables, billing and invoicing errors, and accounts that have aged toward write-off. A recovery partner runs the outreach, sets up payment arrangements, keeps everything compliant, and reports results back to you.

The term covers a lot of ground, and providers specialize in different slices. Some focus on healthcare claims, others on subscription churn or retail deductions. This guide focuses on the slice most B2B businesses deal with: recovering overdue and delinquent receivables across the full lifecycle, from the first missed payment through charge-off.

The common mistake is treating this as a synonym for late-stage debt collection. It is broader than that. Recovery often starts while an account is still on your books as a receivable, before it is ever written off. Working those accounts early, while the customer relationship is still intact, is where the strongest results come from. By the time a balance is charged off and handed to a traditional agency, most of the leverage is already gone.

A real program covers four jobs, not one: a multichannel outreach strategy, flexible payment options, compliance management, and live reporting. A partner that only dials phones at 90 days and later is doing a slice of the work, not the whole job.

Why Internal AR Teams Struggle to Keep Up

Most AR teams are not failing at recovery. They are outnumbered. The accounts pile up faster than a lean team can work them, and the usual tools were built for a time when people answered the phone.

The Most Common Causes of Overdue Receivables

Overdue receivables rarely come from one source. They tend to cluster into three:

- Failed payments. Expired cards, ACH declines, insufficient funds. These are not customers refusing to pay. Most never knew the charge bounced. This is what subscription businesses call involuntary churn, and a single well-placed reminder, sent through the right channel, clears many of them in minutes.

- Billing disputes. An unclear line item, a surprise balance, or an unresolved insurance claim freezes an account until someone explains it. Until that confusion clears, no amount of follow-up moves the money.

- Accounts no one had time to work. A stretched team triages the largest or loudest balances and lets the rest drift.

That last one is the quiet killer. Meanwhile, the default tool, the outbound phone call, keeps losing ground because people no longer pick up unknown numbers the way they did a decade ago.

What Happens When Recovery Is Delayed

Delay is not a neutral holding pattern. Accounts roll.

A 30-day balance becomes 60, then 90, and each step down the line is harder to collect than the one before it. That migration is the roll rate, and it compounds quietly across a portfolio while attention sits elsewhere. It also drags your DSO (Days Sales Outstanding) higher, which means cash you have already earned stays locked up longer.

The reason is mechanical:

- The original relationship cools, and contact details go stale

- The customer’s limited funds get claimed by whichever creditor is making the most noise

- Simple, low-cost outreach gives way to formal, lower-yield processes

A balance you could have cleared with a friendly text at day 20 may need a formal collections process by day 120. The cost of waiting is real even when it never shows up as a line item on a report.

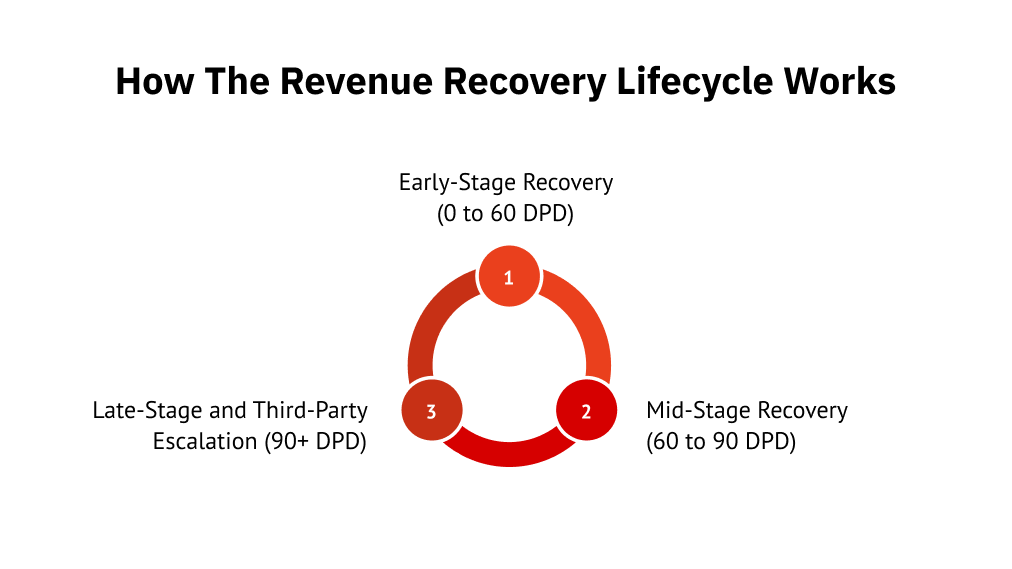

How the Revenue Recovery Lifecycle Works

Recovery is not one job. There are three, and they change with the age of the account. What works on day 20 is wrong at day 100, and the partners that recover the most are the ones who match the approach to the stage. Here is how each one works.

Early-Stage Recovery (0 to 60 DPD)

This is the window where recovery is easiest and where most of the money is still winnable. The account is fresh, the relationship is intact, and the customer still thinks of the balance as something they owe you, not a debt in collections.

At this stage, the first-party model applies. Outreach goes out under your brand, so the customer feels like they are still dealing with you:

- SMS reminders and email payment links do most of the work

- A self-service portal lets people pay or set up a plan without talking to an agent

- The tone stays friendly because this is a nudge, not a demand

Pro Tip: Treat failed payments as a service problem, not a collections problem. A large share of 0 to 30 DPD balances are just bounced cards. A quick, branded reminder fixes them and protects the relationship at the same time.

Mid-Stage Recovery (60 to 90 DPD)

By 60 days, the easy wins are gone, and risk climbs. Outreach gets more structured, and the conversation moves toward arrangements rather than simple reminders:

- Payment plans and settlement offers come to the front

- Follow-ups are sequenced across channels, not repeated on a single one

- Escalation triggers flag accounts drifting toward charge-off

This is usually where internal teams hit their ceiling. The volume of structured, multi-touch follow-up that 60- to 90-day accounts demand is exactly what a stretched AR desk cannot sustain, which is why outsourcing tends to get evaluated right here.

Late-Stage and Third-Party Escalation (90+ DPD)

Past 90 days, an account typically crosses into third-party territory. The agency works under its own name, and the full weight of the FDCPA applies to every contact.

Accounts land here for specific reasons:

- A payment arrangement broke down

- The balance crossed your charge-off threshold

- Internal and first-party efforts are exhausted

Recovery rates are lower this late; that is just the nature of aged debt. But on a large portfolio, even single-digit recovery percentages add up to real dollars, which is why late-stage and portfolio recovery work still earns its place.

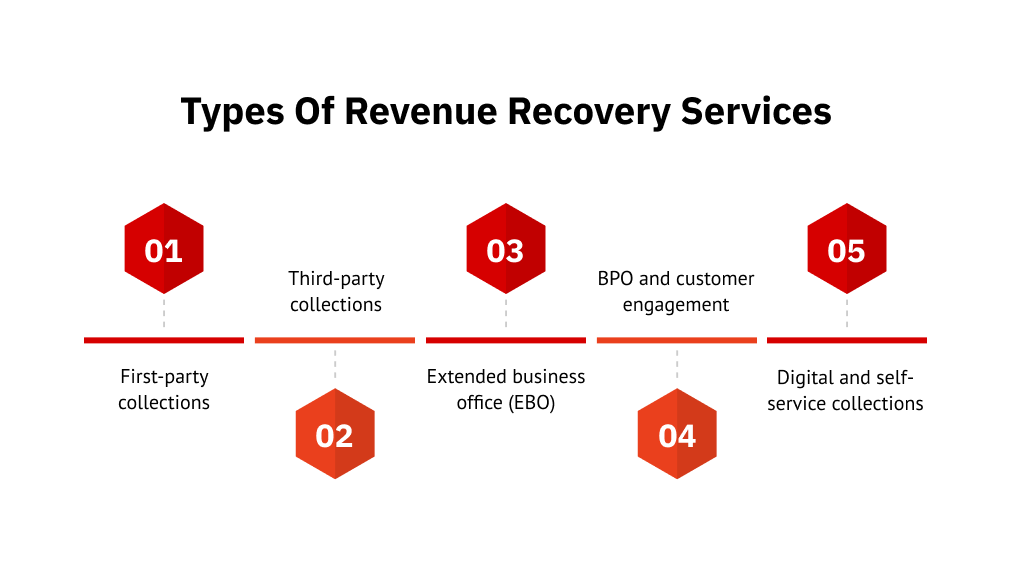

Types of Revenue Recovery Services and What Each Model Covers

“Revenue recovery” is an umbrella term. Under it sit several distinct service models, and most strong programs combine a few of them rather than relying on one. Here is how they compare:

| Service type | What it covers | Best for | Pricing model |

| First-party collections | Early-stage outreach under your brand: reminders, payment links, portal access | 0 to 90 DPD, relationship-sensitive accounts | Usually retainer plus contingency |

| Third-party collections | Formal late-stage recovery under the agency’s own name, FDCPA applies | 90+ DPD, charged-off or escalated accounts | Contingency: no recovery, no fee |

| Extended business office (EBO) | Outsourced AR and billing follow-up that runs before write-off, as an extension of your team | High-volume billing ops, healthcare patient balances | Retainer or per-account |

| BPO and customer engagement | Call center, support, and back-office work for accounts stalled by disputes or billing questions | Accounts blocked by a service issue, not refusal to pay | Retainer or per-seat |

| Digital and self-service collections | Digital-first outreach plus a white-labeled portal for self-service payment | At any stage, scaling recovery without adding headcount | Typically bundled into the program |

One distinction worth holding onto: EBO and digital outreach often work accounts before charge-off, while third-party collections is a post-write-off function. They are not interchangeable, and a partner should be clear about which stage each service touches.

First-Party vs Third-Party Collections, and Which One Applies

The practical difference is whose name the customer sees.

- First-party: the customer believes they are still dealing with you. Used at 0 to 90 DPD, when the relationship is worth protecting and a softer touch still works.

- Third-party: an external agency operates under its own identity. Used once internal and first-party efforts are exhausted, or the account has crossed charge-off.

The friction shows up at the handoff. When first-party and third-party live with two separate vendors, account context and payment history get lost in the transfer, and the customer ends up re-explaining their situation to a stranger. Running both under one partner keeps that history attached to the account, so the escalation feels continuous rather than like starting over.

What a Managed Recovery Program Should Actually Include

The lifecycle tells you when recovery happens. These are the operational pieces that decide how well it works. If a program is missing one of them, that gap shows up directly in your recovery rate.

Omnichannel Outreach Calibrated to Consumer Behavior

A real program runs SMS, email, outbound calls, and a digital payment portal, not one or two of them. Digital-first sequencing drives higher contact rates, with calls held back for complex resolution rather than used as the default. The channel mix should shift to match how each person responds. Someone who pays from a text link should not keep getting calls.

AI-Driven Account Segmentation

Not every account deserves the same effort, and batch outreach wastes capacity on the ones least likely to pay. Segmentation sorts accounts by DPD bucket, payment history, and behavioral signals so the highest-probability balances get worked first. From there, the system decides the best time, channel, and message tone per account, instead of pushing everyone through the same fixed sequence.

Self-Service Payment Portal

Most people would rather resolve a balance on their own time than talk to an agent. A good portal lets them:

- Check the balance and pay in full at any hour

- Set up a weekly or monthly payment plan

- Accept an offer or discount without a phone call

It should be white-labeled under your brand, so the customer never sees the vendor’s name. The payoff is lower friction, higher completion, and recovery that scales without adding headcount.

Real-Time Reporting for Clients

You cannot hold a partner accountable to numbers you cannot see. A client dashboard should show, at minimum:

- Recovery rate by DPD bucket

- Contact rate and channel performance

- Payment plan adherence

The reporting should be live or near-live, not a monthly PDF that arrives after the decisions are already made. A partner that can only show you last month’s results is a partner you cannot course-correct with.

Compliance Is Built In, Not an Add-On

In recovery, compliance is not paperwork you file at the end. It governs every message you send, and a single mishandled contact can cost more than the balance you were chasing. A few rules set the floor:

- FDCPA governs third-party collector conduct

- Regulation F extends those rules to SMS and email, including frequency and content limits

- TCPA covers consent for automated and text contact

On top of that sit industry overlays. Healthcare client data pulls in HIPAA, payment handling pulls in PCI DSS, and state-level UDAAP rules add their own requirements that often run stricter than federal ones.

Here is the part that matters when you evaluate a partner. Any provider can say they are compliant. A serious one can show you how each rule is wired into the workflow: how consent is captured, how opt-outs propagate across channels, how violations get escalated. If compliance lives in a policy document instead of the system itself, it is a claim, not a control. FCS treats this as core to the program’s design rather than a box checked after the fact.

5 Compliance Questions to Ask Before You Sign

- How do you capture and document consumer consent for SMS and digital outreach?

- What is your process for handling opt-out requests across every channel?

- Do you carry errors and omissions insurance?

- How are compliance violations escalated and reported to us?

- What certifications or audits have you completed in the last 12 months?

How to Evaluate a Revenue Recovery Partner

You are not just buying recovery dollars. You are handing a vendor direct contact with your customers, under your brand or alongside it. The evaluation should weigh both.

8 Questions to Ask Before You Sign

- What are your recovery rate benchmarks at 30, 60, and 90-plus DPD for portfolios in my industry?

- What compliance certifications do you hold, and when were you last audited?

- What channels does your outreach include, and is digital the default or the exception?

- Do you offer both first-party and third-party recovery, or only one model?

- What does my reporting access look like, and how often is it updated?

- What is your onboarding timeline, and what do you need from my team to go live?

- Can you share anonymized case studies or references in my industry?

- What is your pricing model: contingency, retainer, or hybrid?

The answers to questions 1 and 7 are the tell. A partner with real industry experience can talk about benchmarks and examples specific to your vertical. A vague answer here usually means you would be their experiment.

Pricing Models Explained

There is no single right structure. The model should match the stage and quality of the accounts you are placing.

- Contingency only: no recovery, no fee. Lowest risk for you, most common in third-party programs where accounts are already distressed.

- Retainer plus contingency: a flat monthly cost plus a performance percentage. Common when the program includes first-party or BPO components that run continuously, not just on placement.

- Per-account flat fee: less common, but useful for clean, high-volume early-stage portfolios where outcomes are predictable.

A quick rule: the earlier and healthier the accounts, the more a flat or retainer model can make sense. The more distressed the placement, the more contingency protects you.

Red Flags to Watch For

- Guaranteed recovery rates quoted with no benchmark context or industry qualification. Nobody can promise a number without seeing your accounts.

- No documentation of certifications, audit history, or a compliance training program.

- Phone-only outreach with no digital portal or self-service payment option, which signals a playbook built for a decade ago.

How First Credit Services (FCS) Approaches Revenue Recovery

Most of this guide has been about what to look for. Here is how FCS lines up against it.

First Credit Services runs recovery as a managed service, which it calls a service-as-a-software model. You do not staff or operate the program yourself. FCS runs it on your behalf, which keeps the lift on your side light and means you are not standing up a collections function in-house just to see results.

It covers first-party and third-party recovery under one relationship, so the handoff problem from earlier never shows up. Account context and payment history stay attached as a balance moves from a friendly branded reminder to formal escalation. Nobody has to re-explain their situation.

The engine behind it is UCEP, the Unified Consumer Engagement Platform. It handles:

- AI-driven contact strategy: the best time, channel, and tone for each account

- Omnichannel outreach across SMS, email, phone, and chat

- White-labeled self-service portals that run under your brand

- Configurable payment plans and offers

After years of running these programs, the priority stays consistent: resolve balances early and under your brand while the relationship is intact, and escalate formally only when an account genuinely needs it.

Conclusion

Revenue recovery is won early. The accounts easiest to collect are the ones still close to the original sale, worked under your brand, through the channels your customers actually use. By the time a balance is aged and handed off cold, most of the value is already gone.

So the partner you want is one that covers the whole lifecycle, first-party through third-party, keeps compliance inside the workflow instead of in a policy file, and shows you live performance you can act on. Get those three right, and recovery stops being a scramble at charge-off and starts being a system.

See where your recovery program stands. Talk to First Credit Services about working accounts earlier, under your brand, across the full delinquency lifecycle.

FAQs

1. What is the difference between revenue recovery services and debt collection?

Debt collection usually means late-stage work on charged-off accounts. Revenue recovery is broader. It works across accounts across the full lifecycle, often before write-off, while the customer relationship is still intact.

2. How much do revenue recovery services typically cost?

It depends on the model. Third-party work is usually contingency, a percentage of what is recovered. First-party and BPO programs often run on a retainer plus contingency. Clean, high-volume early-stage portfolios sometimes use a flat per-account fee.

3. At what delinquency stage should a business bring in a recovery partner?

Earlier than most teams do. Many engage around 60 to 90 DPD, when structured multi-channel follow-up outpaces internal capacity. Bringing a partner in during early-stage recovery captures balances while they are still easiest to collect.

4. Will outreach from a recovery partner damage our customer relationships?

Not if it runs first-party. Branded, digital-first outreach reads like a reminder from you, not a collections call. The risk rises only when accounts escalate to third parties, which is exactly why early resolution matters.

5. Do revenue recovery partners report to the credit bureaus?

Third-party collectors can report delinquent accounts to the bureaus, subject to FDCPA and furnisher rules. First-party and early-stage outreach typically does not. Confirm a partner’s reporting policy before you place accounts.

6. How long does it take to see results from a managed recovery program?

Most programs show early-stage activity within the first few weeks of onboarding, once data is integrated and outreach is live. Clear recovery trends usually emerge within the first 60 to 90 days.