")

Digital collections are built for the channels consumers already use: mobile, email, SMS, payment links, and self-service portals.

According to the Pew Research Center’s 2025 Mobile Fact Sheet, 91% of U.S. adults own a smartphone. For high-volume recovery teams, that changes what effective debt collection looks like. Consumers expect timely reminders, simple payment options, and the ability to resolve balances without waiting for an agent.

Still, buying the best debt collection software is not always the right answer. Many businesses do not want to manage workflows, compliance, agents, reporting, and campaign optimization on their own.

That is where managed recovery providers with in-house digital debt collection software become valuable. They use their own collections management software, automated workflows, and recovery teams to collect accounts on behalf of clients.

In this blog, we’ll compare the top providers using this managed, software-powered recovery model.

Contents

- 1 Standalone Software vs Managed Digital Collection Providers

- 2 Comparing Top Managed Recovery Providers Using In-House Digital Collection Technology

- 2.1 1. UCEP by First Credit Services: Best for Managed Omnichannel Recovery

- 2.2 2. Heartbeat by Trueaccord: Best for AI-Led Digital Collections

- 2.3 3. IC System Client Portal: Best for Agency-Led Recovery Visibility

- 2.4 4. Collect And Receive by Indebted: Best for Digital-First Recovery

- 2.5 5. Firstsource Digital Collections Infrastructure: Best for Enterprise Recovery At Scale

- 3 What To Look for in a Provider with In-House Digital Collection Technology

- 4 How to Choose the Right Software-Powered Recovery Provider

- 5 Choose Software-Powered Recovery Without Adding Software Workload

- 6 FAQs

- 6.1 1. What is digital debt collection software?

- 6.2 2. Is digital debt collection software always sold as SaaS?

- 6.3 3. What is the difference between standalone and managed digital debt collection software?

- 6.4 4. Which providers use their own digital debt collection technology?

- 6.5 5. Does FCS sell UCEP as standalone software?

- 6.6 6. What should buyers look for in a digital collections provider?

Standalone Software vs Managed Digital Collection Providers

Standalone digital debt collection software is usually licensed by your business. Your team operates the platform, sets workflows, manages outreach, monitors compliance, reviews reports, and handles account resolution.

Software-as-a-Service (SaaS) works similarly. You access cloud-based software, but your internal team still runs the process. However, service-as-Software (SaS) is different.

In this model, the provider uses its proprietary platform to deliver the service outcome for you. You get the benefits of automation, digital outreach, reporting, and workflow intelligence without having to manage the software, campaigns, staffing, or compliance operations yourself.

A managed digital collection provider usually handles:

- Digital outreach

- First-party and third-party workflows

- SMS, email, phone, chat, and portal engagement

- Consumer self-service

- Compliance controls

- Agent escalation

- Client reporting

In simple terms, standalone software gives you the platform. A managed SaS provider gives you the platform, the team, and the recovery operation behind it.

Comparing Top Managed Recovery Providers Using In-House Digital Collection Technology

The providers below are not just standalone software vendors. They are managed recovery companies that use proprietary, in-house, or internally operated digital collection technology to support recovery on behalf of clients.

Some have named proprietary platforms, whereas others combine client portals, digital workflows, analytics, and recovery operations into a managed service model. Here’s a brief comparison:

| Provider | In-house technology | Model | Best for |

| First Credit Services | UCEP | Service-as-Software managed collections | Businesses that want omnichannel recovery without running software internally |

| TrueAccord | HeartBeat | Digital-first collection agency | Businesses focused on AI-led digital engagement and self-service repayment |

| IC System | Client portal and digital collection tools | Managed collections with client visibility | Organizations that want an established agency with digital tools and reporting access |

| InDebted | Collect and Receive | Digital-first recovery and first-party workflows | Enterprises evaluating AI-led collections across outsourced and first-party models |

| Firstsource | Digital collections infrastructure | Enterprise digital collections and BPO | Large creditors needing outsourced digital recovery at scale |

Now, let’s look at how each provider uses in-house digital collection technology in practice.

1. UCEP by First Credit Services: Best for Managed Omnichannel Recovery

First Credit Services is an omnichannel debt collection and BPO company offering first-party collections, third-party collections, and customer engagement services. Its proprietary Unified Consumer Engagement Platform (UCEP) is used in a service-as-software model. It means FCS operates the technology for clients instead of asking them to manage the platform.

UCEP also helps FCS coordinate digital outreach, payment options, and reporting across high-volume account portfolios.

Key Features

- Service-as-Software model: FCS runs UCEP as part of its managed digital collections service. Clients get software-powered recovery without having to manage the daily software workload.

- Omnichannel outreach: UCEP supports SMS, email, phone, chat, and portal-based communication. This helps FCS reach consumers through the channels they are more likely to use.

- Consumer self-service portal: Consumers can access payment links, review balances, make payments, set up plans, schedule callbacks, or use chat. This reduces friction and improves account resolution.

- First-party and third-party coverage: FCS can support early-stage first-party collections and later-stage third-party collections. This gives businesses a more connected recovery lifecycle.

- White-labeled first-party experience: For first-party collections, consumers can see the client’s brand instead of FCS branding. This helps protect customer relationships during sensitive recovery stages.

Where UCEP Fits Best?

UCEP is useful when collection performance is being limited by fragmented follow-up, inconsistent account handling, or delayed escalation. Instead of treating digital outreach as a separate add-on, FCS uses UCEP to support a more organized recovery process from placement to resolution in the following ways:

- Prioritizes account movement: UCEP helps accounts progress through defined recovery paths rather than sit in manual queues for too long.

- Reduces handoff gaps: It supports a smoother flow between digital engagement, agent follow-up, payment activity, and escalation.

- Improves consistency at scale: High-volume portfolios can be managed with greater structure, so outcomes do not depend solely on individual collectors’ capacity.

Best for: Mid-sized to enterprise businesses that want managed digital collections, omnichannel outreach, reporting, and first-party or third-party recovery support.

2. Heartbeat by Trueaccord: Best for AI-Led Digital Collections

TrueAccord is a digital-first debt collection agency that uses AI, machine learning, and consumer-friendly engagement to support recovery. Its HeartBeat engine helps determine when to contact consumers, which channel to use, what message to send, and what repayment option to offer.

TrueAccord is built around digital engagement rather than call-heavy collections. It focuses on self-service repayment, personalized communication, and scalable recovery.

Key Features

- HeartBeat decision engine: HeartBeat uses machine learning and data-driven logic to personalize outreach. It helps optimize contact timing, channel, cadence, and message type.

- Digital-first communication: The model prioritizes digital channels over traditional phone-heavy outreach. This can help reduce friction for consumers who prefer self-service.

- Personalized repayment journeys: Consumers can receive customized engagement based on behavior and account context. This supports a more tailored repayment experience.

- Self-service payment options: TrueAccord emphasizes online repayment and flexible payment experiences. This helps consumers resolve accounts without needing an agent every time.

- Scalable collection workflows: Its technology supports high-volume consumer engagement. This is useful for businesses managing large pools of delinquent accounts.

What to evaluate: If you need broader BPO support, complex voice workflows, or both digital collections and customer engagement outsourcing, check how much of the model is digital-first versus agent-led.

Best for: Businesses looking for a digital-first agency with AI-led outreach, automated engagement, and self-service repayment.

3. IC System Client Portal: Best for Agency-Led Recovery Visibility

IC System is a long-standing debt collection services provider with experience in managed recovery. It combines traditional agency operations with a client portal, reporting, account management tools, analytics, and online access.

Its client portal allows businesses to submit accounts, manage inventory, generate reports, and view statements.

Key Features

- Secure client portal: Clients can submit accounts, manage inventory, and access reports. This helps centralize placement and account visibility.

- Managed collection services: IC System handles recovery execution as a service provider. This helps businesses avoid managing every collection activity internally.

- Reporting access: Clients can generate reports and view account status information. This supports better visibility into recovery activity.

- Analytics-supported recovery: IC System references analytics and collection tools that support account handling. This helps guide recovery activity beyond manual follow-up.

- Established agency experience: The company has decades of experience in collections. This can matter for organizations that value process maturity and operational history.

What to evaluate: If you need a highly digital-first consumer experience, review its SMS, email, portal, automation, and self-service payment depth. Also, check how digital outreach connects with agent activity.

Best for: Organizations that want an established collection agency with client tools, reporting access, and managed recovery support.

4. Collect And Receive by Indebted: Best for Digital-First Recovery

InDebted is a digital-first debt recovery company that uses technology to support customer-centered collections. Its solutions include Collect for outsourced recovery and Receive for AI-native first-party collections.

InDebted focuses on digital engagement, automation, self-service, and modern consumer experiences across collection workflows.

Key Features

- Collect for outsourced recovery: Collect is designed for organizations that want InDebted to manage debt recovery. This supports a more hands-off collection model.

- Receive for first-party workflows: Receive is positioned as AI-native first-party debt collection software. It supports enterprises that want earlier-stage digital collections.

- AI-led engagement: The platform uses AI to support customer communication and recovery workflows. This can help personalize outreach at scale.

- Digital self-service: InDebted emphasizes consumer-friendly digital repayment. This helps reduce reliance on phone-based collections.

- Global operating footprint: InDebted operates across multiple regions. This can be useful for enterprises with cross-market recovery needs.

What to evaluate: Clarify whether you need managed collections or first-party software-led workflows. If you want the provider to manage execution, evaluate Collect. If your team wants more internal control, review Receive.

Best for: Enterprises evaluating AI-led digital collections across outsourced and first-party recovery models.

5. Firstsource Digital Collections Infrastructure: Best for Enterprise Recovery At Scale

Firstsource is a business process management provider that offers digital debt collection and recovery services for banks, financial institutions, credit card issuers, auto finance companies, and other large creditors.

Its digital collections infrastructure combines self-service experiences, analytics, compliance support, and outsourced recovery operations.

Key Features

- Enterprise digital collections: Firstsource supports outsourced digital debt collection across large portfolios. This makes it suitable for creditors with high volumes of delinquent accounts.

- Self-service debt management: Its digital collections solution offers consumers discreet, convenient ways to manage repayments. This can reduce reliance on call-heavy recovery.

- Data-driven recovery: Firstsource highlights a data-driven approach using proprietary technology. This supports targeting, personalization, and performance management.

- Compliance and risk controls: The company includes compliance oversight, complaint management, monitoring, and risk controls in its digital collections model. This matters for regulated creditors.

- BPO delivery capacity: Firstsource brings large-scale outsourcing infrastructure and digital collections. This can support creditors that need staffing, operations, analytics, and technology together.

What to evaluate: If you are a mid-sized business or need a more focused recovery partner, check whether Firstsource’s enterprise model fits your account volume, budget, onboarding needs, and desired level of customization.

Best for: Large creditors, banks, lenders, and enterprises that need outsourced digital debt collection, BPO capacity, self-service recovery, and operational scale.

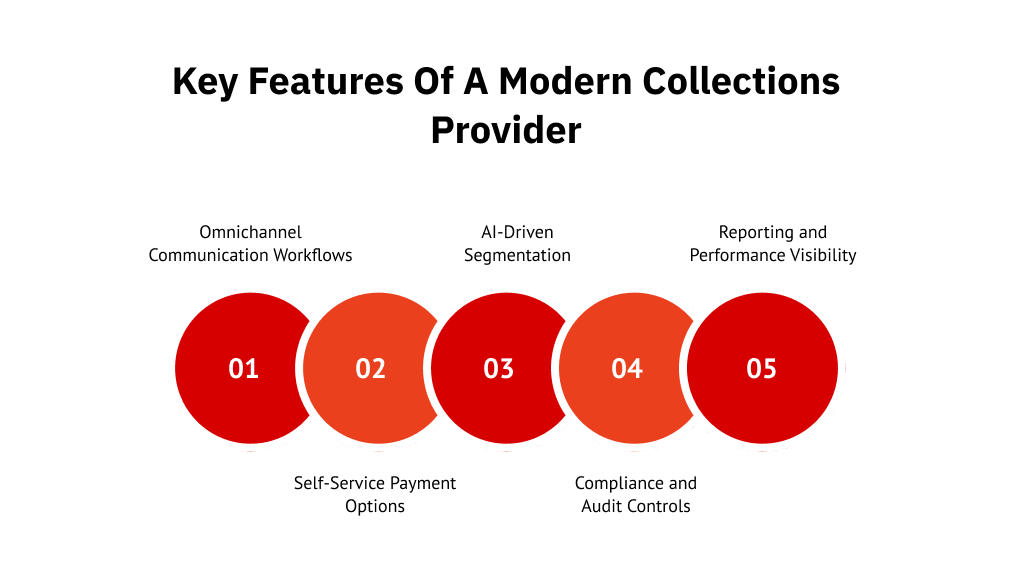

What To Look for in a Provider with In-House Digital Collection Technology

The value of digital debt collection software depends on how well the provider uses it in real recovery workflows. The right partner should not only automate outreach. It should help accounts move faster, reduce manual effort, protect compliance, and make repayment easier for consumers.

Here’s what to evaluate before choosing a provider:

1. Omnichannel Communication Workflows

Look for SMS, email, phone, chat, and portal outreach working together. Disconnected channels create inconsistent follow-up and make it harder for consumers to respond.

A strong omnichannel model helps the provider adjust timing, channel, and messaging based on account behavior. This is where FCS’s UCEP model is relevant, as it brings multiple outreach channels into a single managed workflow.

2. Self-Service Payment Options

Consumers are already comfortable paying digitally. According to McKinsey’s 2024 Digital Payments Survey, digital payments are now a default behavior for many consumers. About nine in ten consumers in the U.S. and Europe made a digital payment in the past year, with U.S. adoption reaching 92%.

For collections, that matters. Consumers are more likely to act when they can review a balance, open a secure payment link, choose a payment plan, or complete payment without waiting for an agent.

3. AI-Driven Segmentation

AI can help prioritize accounts, choose outreach timing, and adjust follow-up logic. However, the important question is not whether a provider says it uses AI. It is how the AI is used, what data it reads, and how decisions are monitored.

Ask whether the system supports account prioritization, channel selection, response-based follow-up, and escalation. Also, ask how the provider prevents automation from creating compliance or customer experience issues.

4. Compliance and Audit Controls

Digital collections must support compliance from the first contact to final resolution. Look for controls around FDCPA, Regulation F, FCRA, TCPA, HIPAA, PCI DSS, opt-outs, consent, disputes, complaints, and audit trails.

For regulated industries, this matters as much as recovery performance. A provider using in-house technology should be able to show how communication rules, data access, payment security, and account activity are documented.

5. Reporting and Performance Visibility

Even if the provider runs the technology for you, your team still needs clear visibility into it. Ask what dashboards you receive and whether they show placements, contact rates, payments, disputes, recalls, channel performance, and recovery by segment.

For example, FCS provides reporting visibility while operating UCEP as a managed service. That gives clients insight into performance without requiring them to manage the backend platform themselves.

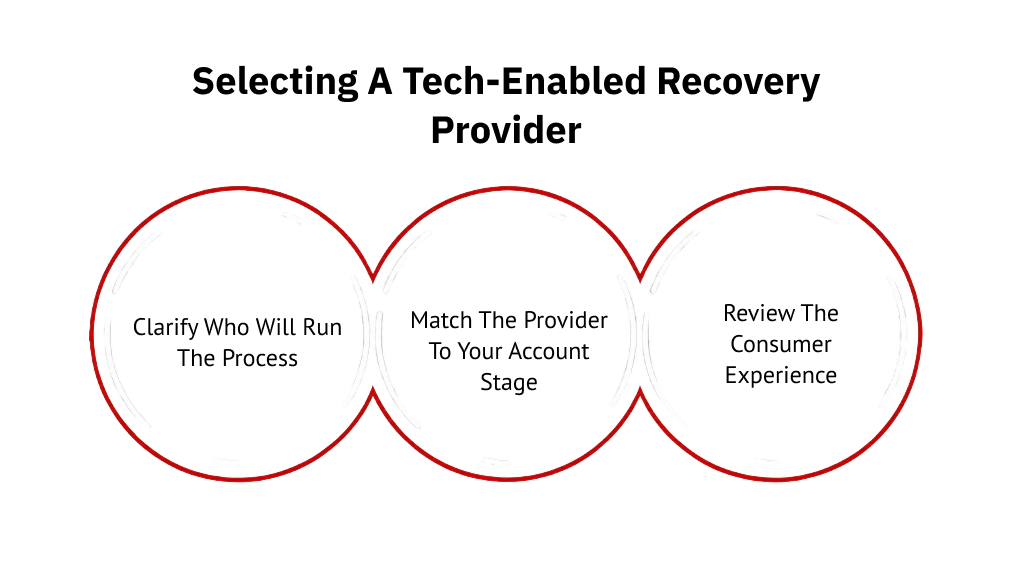

How to Choose the Right Software-Powered Recovery Provider

The right provider should match your team’s capacity and collection stage. Before choosing one, look beyond the software features and evaluate how the provider will actually support recovery.

1. Clarify Who Will Run the Process

Decide whether you need a tool your team will manage or a partner that runs the recovery process for you.

- Choose standalone software if you already have internal collectors, compliance oversight, and workflow owners.

- Choose a managed SaS provider if you want the provider to handle outreach, workflows, reporting, and escalation.

- Choose a hybrid model if you want internal visibility with external operational support.

2. Match The Provider to Your Account Stage

Early-stage accounts usually need softer, brand-sensitive follow-up. Older or harder-to-resolve accounts need stronger third-party recovery workflows. A provider like FCS can support both first-party and third-party collections, helping businesses manage recovery across multiple stages.

3. Review The Consumer Experience

Check what the consumer sees and how easy it is to act. The provider should offer clear balance visibility, secure payment options, payment plans, support channels, and respectful communication. For first-party collections, also ask whether the experience can stay aligned with your brand.

Choose Software-Powered Recovery Without Adding Software Workload

Digital debt collection software can improve outreach, payment access, reporting, and customer experience. But modernization does not always mean buying another platform for your internal team to manage.

For many businesses, the real choice is whether to run the software internally or work with a partner that already has the technology, team, workflows, and compliance controls in place.

That is where managed digital collections can make a difference. With FCS, businesses get access to UCEP, a proprietary SaS platform operated through FCS’s managed collections model.

So instead of building the recovery operation in-house, your team gets a software-powered partner to manage outreach, engagement, reporting, and escalation at scale.

Book a demo to see how FCS can manage digital collections for your business.

FAQs

1. What is digital debt collection software?

Digital debt collection software helps manage and improve debt recovery through SMS, email, payment links, portals, segmentation, reporting, automation, and compliance workflows.

2. Is digital debt collection software always sold as SaaS?

No. Some tools are sold as software-as-a-service (SaaS), in which your team licenses and operates the platform. Others use a service-as-software (SaS) model, where the provider uses its technology to manage collections for you.

3. What is the difference between standalone and managed digital debt collection software?

Standalone software is operated by your internal team. Managed digital collection providers use their own in-house technology to handle outreach, compliance support, reporting, and recovery execution.

4. Which providers use their own digital debt collection technology?

Providers with proprietary or in-house technology include FCS with UCEP, TrueAccord with HeartBeat, and InDebted with Collect and Receive.

5. Does FCS sell UCEP as standalone software?

No, FCS operates UCEP as part of its managed digital collections model. Thus, clients benefit from the platform without running campaigns, workflows, or outreach operations themselves.

6. What should buyers look for in a digital collections provider?

Look for omnichannel outreach, self-service portals, AI-driven segmentation, compliance controls, reporting visibility, payment workflows, agent escalation, and experience across the collection stages your business needs.