Overdue accounts become harder to recover when businesses wait until collections are the only option left.

QuickBooks’ 2025 report found that 56% of surveyed small businesses had outstanding invoices, averaging $17,500 per business. For high-volume businesses, unpaid balances can quickly strain AR teams, slow cash flow, increase delinquency, and push more accounts toward late-stage recovery.

Pre-collection services help businesses act earlier. They give customers a clear, low-friction path to resolve overdue balances before formal collections become necessary.

This guide covers what pre-collection services include, how they work, when outsourcing makes sense, and how to choose the right provider.

Contents

- 1 What are Pre-Collection Services?

- 2 Why Pre-Collection Services Matter

- 3 What Pre-Collection Services Typically Include

- 4 How Pre-Collection Services Work: The Process

- 5 Key Benefits of Using a Pre-Collections Service

- 6 What to Look For in a Pre-Collections Outsourcing Partner

- 6.1 Brand-Sensitive Communication and White-label capability

- 6.2 Omnichannel Outreach and Self-Service Payment Infrastructure

- 6.3 Compliance-Aware Workflow Controls

- 6.4 CRM and Billing System Integration

- 6.5 Managed Execution, Not Just Software

- 6.6 Reporting and Recovery Performance Visibility

- 6.7 Escalation Capability Beyond Pre-Collection

- 7 Compliance Considerations for Pre-Collection Services

- 8 Resolve Overdue Accounts Before They Escalate

- 9 FAQs

- 9.1 1. What happens during the pre-collection stage?

- 9.2 2. How do pre-collection services differ from debt collection?

- 9.3 3. How many days past due should an account be before pre-collection starts?

- 9.4 4. Are pre-collection letters legally required?

- 9.5 5. Can pre-collection services reduce charge-offs?

- 9.6 6. What recovery rates can pre-collection services achieve?

What are Pre-Collection Services?

Pre-collection services are early-stage recovery services used before formal debt collection begins. They usually apply to accounts that are 1 to 90 days past due, depending on the business model, payment terms, and escalation policy.

The outreach is softer than formal collections. It focuses on helping customers:

- Understand the balance

- Pay through a secure link.

- Update payment details

- Ask a billing question.

- Set up a payment plan.

- Resolve a dispute before escalation.

This is where pre-collection services differ from third-party debt collection. Formal debt collection usually begins after repeated non-response, serious delinquency, charge-off, or write-off.

Pre-debt collection happens earlier, when the account is still more likely to resolve through clear communication and easy payment access. In the debt lifecycle, pre-collection sits between internal billing reminders and formal collections.

Why Pre-Collection Services Matter

Pre-collection matters because recovery becomes harder as accounts age.

A recently overdue account may only need a clear reminder, a payment link, or a quick billing clarification. But once the account moves deeper into delinquency, the process becomes more expensive and harder to manage.

Thus, businesses may need more contact attempts, stronger documentation, formal escalation, and higher recovery efforts.

The cash flow risk is also significant. The PYMNTS 2025 survey found that 86% of businesses have up to 30% of monthly invoiced sales overdue. The report also noted that a 30% payment delinquency rate sits far outside the normal range of about 5%.

Such figures show that late payments are not just an AR issue. They can also disrupt operating cash flow, delay revenue visibility, and put more pressure on internal teams.

This is where early action changes the outcome.

Pre-collection services give businesses a structured receivables follow-up process before accounts become harder to recover. Instead of waiting until formal collections are necessary, businesses can use:

- Reminder-led outreach

- Secure payment links

- Self-service payment options

- Dispute clarification

- Payment-plan setup

- Brand-sensitive follow-up

However, pre-delinquency recovery also depends on tone. Customers are more likely to respond when outreach feels like account support, not an abrupt move into collections. That is why pre-collection works best when communication is clear, timely, and easy to act on.

What Pre-Collection Services Typically Include

A strong pre-collection program does more than notify customers about overdue balances. It combines these service components:

| Service component | What it does | Example use case |

| Pre-collection letters | Documents the overdue balance and next step | Patient balance reminder |

| Email and SMS | Reaches customers through faster channels | Failed subscription payment |

| Outbound calls | Supports accounts needing explanation | Higher-balance overdue account |

| Payment links | Reduces friction to payment | Card update or one-time payment |

| Self-service portal | Lets customers resolve independently | High-volume consumer accounts |

| Payment plans | Gives customers flexible options | Healthcare, utilities, lending |

| Dispute clarification | Separates billing issues from non-payment | Insurance adjustment or account mismatch |

Here is how each component works in practice:

Written Outreach and Reminder Letters

Pre-collection letters give customers a clear record of the balance, due date, payment options, and next steps. In the early pre-collection stage, these letters should feel like account notices, not formal collection warnings.

The language should be:

- Direct

- Factual

- Brand-safe

- Easy to understand

- Focused on resolution

A demand letter may be used later in the pre-collection process when earlier reminders have not resolved the account. It is more formal than a standard reminder and usually outlines the balance due, payment deadline, available resolution options, and possible next steps if the account remains unpaid.

The goal is not to threaten escalation but to give the customer one more clear chance to resolve the balance.

Multichannel Payment Reminders

Payment reminder services should not rely only on calls. Customers respond differently depending on account type, channel preference, timing, and urgency.

A strong workflow may include:

- Email reminders

- SMS reminders

- Voice outreach

- Chat prompts

- Portal links

- Callback options

Coordination is what makes multichannel outreach work. If email, SMS, calls, and portal links operate independently, the customer receives reminders but no clear path to resolution.

Every touchpoint should guide customers to one clear next step, such as paying, updating details, requesting support, or setting up a plan. This reduces delay and helps resolve the account before escalation.

Self-Service Payment Resolution

Self-service account resolution matters because many customers are willing to pay but do not want to call an agent. That’s why an effective pre-collection program should let customers:

- Open a secure payment link

- View their balance

- Pay in full

- Choose a payment plan

- Update payment details

- Schedule a callback

- Start chat

For example, FCS’s consumer portal supports branded payment experiences that allow consumers to access personalized payment links without account numbers.

Payment Plans and Flexible Arrangements

Payment plans help when customers acknowledge the balance but cannot pay in full.

For example:

- A $480 medical balance may be easier to resolve through four monthly payments.

- A utility balance may recover faster with a structured repayment plan.

- A subscription balance may resolve quickly if the customer can update a card and restart service.

The point is not to delay recovery but to create a path that the customer can complete.

How Pre-Collection Services Work: The Process

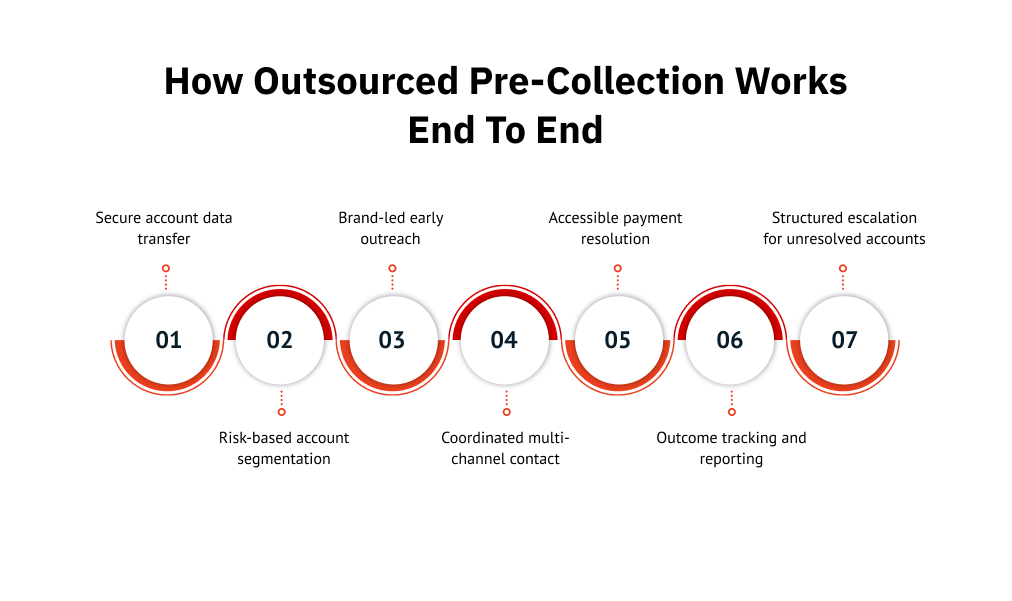

Pre-collection works best when it follows a structured operating model, such as:

Step 1: Account Intake and Data Transfer

The business sends account details to the provider, including:

- Balance amount

- Due date

- Payment history

- Customer contact details

- Account status

- Consent information

- Prior outreach notes

For instance, FCS can receive client data through SFTP, API, or CRM sync, depending on the client’s setup.

Step 2: Risk-Based Account Segmentation

Accounts should be segmented by risk, urgency, and likelihood of resolution. Key factors include:

- Days past due

- Balance size

- Payment history

- Customer type

- Contactability

- Prior response behavior

- Dispute status

This segmentation prevents every overdue account from entering the same workflow. A 7-day failed card payment may only need a quick payment update link, while a 75-day healthcare balance with prior dispute activity may require a more careful, agent-assisted approach.

Step 3: Brand-Led Outreach and Contact Sequencing

The provider launches a contact sequence using approved channels, message templates, and escalation rules. In first-party programs, this outreach can be white-labeled so customers see the business’s brand across emails, SMS links, portal pages, and support touchpoints.

A simple workflow may look like this:

| Stage | Outreach example |

| Day 3 past due | Branded email with payment link |

| Day 7 past due | SMS reminder, if consent allows |

| Day 14 past due | Payment-plan option |

| Day 21 past due | Agent-assisted call or chat |

| Day 30+ past due | Escalation review |

In white-labeled operations, early outreach stays under the client’s brand. Therefore, customers see branded reminders, payment links, and portal pages, making the experience feel like account support instead of a third-party handoff. It helps recover the balance without weakening the customer relationship.

Step 4: Payment Resolution

At this stage, the customer gets a direct path to resolution. This might include:

- Payment in full

- Payment plan setup

- Payment method update

- Callback scheduling

- Dispute submission

- Agent support

This is where early intervention collection services create value. They do not just remind customers but also remove payment friction.

Step 5: Outcome Tracking

Every outcome is tracked, including:

- Paid

- Partially paid

- Promised to pay

- Disputed

- Unreachable

- Opted out

- Wrong contact information

- Unresolved

This data helps the business understand which accounts are recoverable and which need escalation.

Step 6: Escalation for Unresolved Accounts

Accounts that remain unresolved should move into a defined next step, not sit idle. As a pre-charge-off collection service, pre-collection helps businesses identify which accounts can still be resolved through first-party outreach and which need to move into digital collections, third-party collections, or manual review.

Since FCS supports both digital and third-party collections, businesses can keep unresolved accounts within one connected recovery lifecycle. This avoids rebuilding context with a new provider at every escalation point.

Key Benefits of Using a Pre-Collections Service

Pre-collection works best when early outreach is structured, timely, and easy for customers to act on. Here are the key benefits businesses can expect.

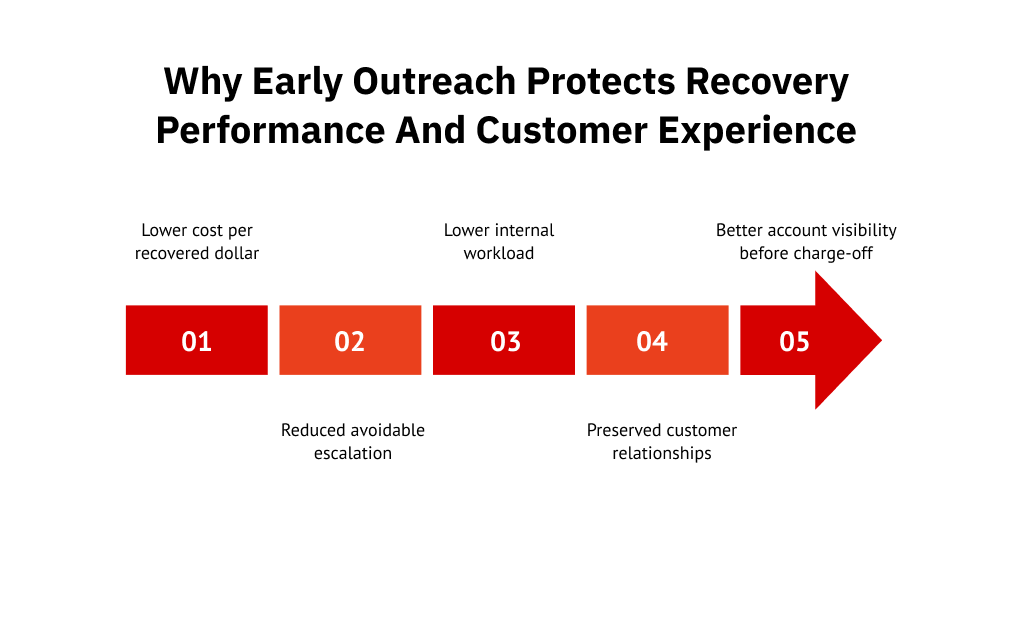

1. Higher Early-Stage Recovery Potential

Early-stage accounts are easier to recover because the balance is still recent, the customer is more likely to respond, and the issue is often simple to resolve.

Pre-collection services help businesses act during that window. A clear reminder, a payment link, a card update option, or a flexible plan can resolve the issue before it requires a heavier recovery effort.

2. Reduced Avoidable Escalation

Many accounts do not need formal debt collection. They need a clearer reminder, better timing, a working payment link, or a simple way to ask a billing question. Pre-collection helps identify which accounts can still be resolved before they move into more sensitive recovery workflows.

3. Preserved Customer Relationships

Soft collection services keep the tone helpful and service-led, so early outreach does not feel like a penalty. For example, a fitness chain recovering a missed membership payment can send a branded SMS with a secure card update link instead of moving the account straight into collections.

The customer can update their payment method, keep the membership active, and resolve the balance without feeling harsh.

4. Lower Internal Workload

AR, billing, and revenue cycle teams often spend too much time on repetitive follow-up. Pre-collection outsourcing helps reduce manual work, such as:

- Resending reminders

- Making follow-up calls

- Logging payment promises

- Answering basic balance questions

- Tracking unresolved accounts

This allows internal teams to focus on disputes, exceptions, and higher-value accounts.

5. Improved Cash Flow Visibility

A structured pre-collection program shows which accounts are moving, which are stuck, and which should be escalated.

For companies with large account volumes, FCS’s BPO and customer engagement services can manage customer contact, inbound inquiries, and operational follow-up. This can extend beyond collections into broader customer engagement workflows.

What to Look For in a Pre-Collections Outsourcing Partner

Pre-collection outsourcing works only when the partner can do more than follow up on overdue accounts. They need to protect the customer experience, maintain consistent outreach, manage payment resolution, document every outcome, and know when an account should move to the next stage.

Here are the key capabilities to evaluate before choosing a pre-collection outsourcing partner.

Brand-Sensitive Communication and White-label capability

A pre-collection agency should know how to communicate without making the account feel escalated too soon. The tone should be clear, helpful, and aligned with how your business already speaks to customers.

For example, a subscription business recovering a failed monthly payment can send a branded reminder that says, “Your payment did not go through. Update your card here to keep your account active.” That feels very different from a third-party notice about an overdue balance.

FCS white-labels its first-party outreach, so customers experience early reminders as part of the client’s account support, not as a third-party collections handoff.

Omnichannel Outreach and Self-Service Payment Infrastructure

The provider should support coordinated email, SMS, voice, chat, and portal outreach. More importantly, those channels should connect to the payment resolution process.

Look for capabilities such as:

- Secure payment links

- Mobile-friendly self-service portals

- Real-time balance visibility

- Payment plan options

- Callback scheduling

- Chat support

- Payment method updates

FCS’s digital debt collection platform facilitates this through a managed omnichannel model. Customers can receive outreach across digital and voice channels, then move directly into self-service payment experiences instead of waiting for agent-led follow-up.

Compliance-Aware Workflow Controls

A pre-collection partner should have clear processes for consent, opt-outs, communication frequency, dispute handling, documentation, account suppression, and escalation rules.

Ask practical questions like:

- What happens when a customer opts out by text?

- What happens when they dispute the balance?

- What happens when the account should pause?

The answer should describe a workflow, not just a policy.

CRM and Billing System Integration

Pre-collection depends on clean data movement. The partner should be able to receive account files securely and return outcome data in a usable format.

Common options include:

- API

- SFTP

- CRM sync

- Billing exports

- Payment updates

- Custom reporting feeds

For businesses with multiple systems, flexibility matters more than a rigid out-of-the-box setup.

Managed Execution, Not Just Software

Some vendors provide software and expect your team to run campaigns. That may not solve the real problem if your internal team is already overloaded.

FCS operates its platform on behalf of clients. Clients do not manage the administrative software directly. FCS handles integration, outreach execution, messaging, reporting, and ongoing program management.

Reporting and Recovery Performance Visibility

The provider should show recovery performance, not just outreach activity. Here you should seek useful reporting, such as:

- Accounts placed

- Accounts contacted

- Dollars recovered

- Payment plans created

- Promises to pay

- Disputes received

- Non-responsive accounts

- Channel performance

- Accounts escalated

- Recovery by days-past-due bucket

This helps leadership compare pre-collection performance against the cost of letting accounts age.

Escalation Capability Beyond Pre-Collection

Pre-collection is only one stage. If an account does not resolve, the business needs a clear next step. Ask whether the provider can manage what happens after pre-collection. If they cannot support the next recovery stage, your team may face another vendor handoff when accounts age.

Compliance Considerations for Pre-Collection Services

Pre-collection services still require compliance-aware execution. Hence, businesses should evaluate:

- FDCPA considerations

- TCPA consent rules

- SMS opt-outs

- Call frequency controls

- Email governance

- Dispute handling

- Documentation standards

- Account suppression rules

The compliance posture may differ depending on whether outreach is handled in-house, through a first-party partner, or through a third-party debt collector.

In-house teams still need accurate data, clear communication rules, and opt-out handling. Outsourced pre-collection requires tighter vendor oversight because the provider represents the customer experience and may trigger additional regulatory expectations.

FCS brings a compliance-aware approach to recovery programs. This is especially important for businesses in regulated industries or high-volume consumer outreach environments.

Resolve Overdue Accounts Before They Escalate

Pre-collection gives businesses a better way to handle early delinquency. Instead of waiting for accounts to age, teams can clarify balances, offer payment options, reduce friction, and recover revenue while the customer relationship is still intact.

For high-volume businesses, this only works when early outreach is structured. Reminders, payment pathways, self-service portals, reporting, compliance controls, and escalation rules need to work together as a single recovery process.

FCS helps businesses manage that process through digital-first outreach, first-party collections, and third-party escalation when needed.

Contact us today to build a pre-collection strategy that fits your recovery lifecycle.

FAQs

1. What happens during the pre-collection stage?

During the pre-collection stage, businesses send structured reminders, payment links, account notices, and support-led follow-ups before moving an account into formal collections.

2. How do pre-collection services differ from debt collection?

Pre-collection happens earlier and uses a softer, support-led tone. Formal debt collection usually begins after repeated non-response, serious delinquency, charge-off, or write-off. Pre-collection focuses on preventing escalation, while debt collection focuses on recovering aged balances.

3. How many days past due should an account be before pre-collection starts?

Pre-collection can begin soon after a missed due date, often within the first 1–30 days past due. Businesses should not wait too long because early outreach gives customers a better chance to pay, clarify issues, or update payment information.

4. Are pre-collection letters legally required?

Pre-collection letters are not always legally required, but they help document outreach and give customers a clear chance to resolve the balance. Requirements may vary by industry, location, account type, and provider model.

5. Can pre-collection services reduce charge-offs?

Yes. Pre-collection services can reduce charge-offs by reaching customers before accounts become seriously delinquent. Early reminders, payment links, and payment-plan options can recover accounts before later-stage collections.

6. What recovery rates can pre-collection services achieve?

Recovery rates vary by account age, industry, balance size, contact quality, and payment options. Early-stage accounts usually perform better, so businesses should ask providers for results by days past due, channel, dispute rate, and escalation rate.