A missed payment is not always the real problem. The bigger risk is what happens next.

When reminders go out late, failed payments go unaddressed, or billing questions remain unresolved, overdue accounts become harder to recover. Customers may still be willing to pay, but unclear balances, weak documentation, or limited payment options can turn a simple delay into a dispute.

The Consumer Financial Protection Bureau’s 2025 report found that 45% of debt collection complaints involved debts consumers said they did not owe. That shows how quickly poor communication can affect recovery.

Debt collection outsourcing services help businesses bring structure, compliance, and consistency to recovery. In this blog, we will cover what these services include, when outsourcing makes sense, which providers to compare, and how to choose the right recovery partner.

Contents

- 1 What Are Debt Collection Outsourcing Services?

- 2 When Should A Business Outsource Debt Collection?

- 3 Best Debt Collection Outsourcing Services To Consider

- 4 What Services Are Included in Debt Collection Outsourcing?

- 5 Risks Of Outsourcing Debt Collection and How to Reduce Them

- 6 How To Choose the Right Debt Collection Outsourcing Partner

- 7 Build A Recovery Model That Protects Revenue and Relationships

- 8 FAQs

- 8.1 1. What are debt collection outsourcing services?

- 8.2 2. Is outsourcing debt collection worth it?

- 8.3 3. What is the difference between first-party and third-party collections?

- 8.4 4. How much do outsourced debt collection services cost?

- 8.5 5. What should you look for in an outsourced collections agency?

- 8.6 6. Can outsourcing debt collection damage customer relationships?

What Are Debt Collection Outsourcing Services?

Debt collection outsourcing services help businesses recover overdue payments through a specialized external partner.

These services may include first-party collections, third-party collections, accounts receivable follow-up, and failed payment recovery. They can also cover omnichannel outreach, payment plans, dispute resolution, compliance controls, and recovery reporting.

When Should A Business Outsource Debt Collection?

You should consider debt recovery outsourcing when unpaid accounts are growing faster than your internal team can manage.

Here are the clearest signs:

1. Your Internal Team Is Spending Too Much Time On Collections

In many businesses, collections sit between finance, billing, support, and operations. One team sends reminders, another handles disputes, and someone else checks payment status. Eventually, no one owns the full workflow.

Outsourcing helps when follow-ups are inconsistent, teams are overloaded, disputes take too long to resolve, aging accounts are not prioritized, and recovery still relies on manual reminders. A collection outsourcing partner brings dedicated ownership, trained resources, and structured workflows.

2. Recovery Rates Are Declining

Declining recovery is often a timing problem. The longer an account ages, the harder it becomes to collect.

Warning signs include more accounts reaching 60 or 90 days past due, customers ignoring phone-only reminders, failed payments turning into churn, unresolved disputes, and limited visibility into recovery performance. For high-volume portfolios, even small delays can create a larger revenue gap.

3. You Need To Scale Without Hiring More Staff

Hiring more collectors, support agents, compliance staff, and reporting analysts is expensive. It also takes time to train them.

Debt collection BPO services can help manage seasonal spikes, portfolio growth, subscription billing volume, rising delinquency, and internal restructuring. Instead of adding permanent headcount, you can use an outsourced collections agency to manage volume while your team focuses on strategy, approvals, and escalations.

4. You Need Stronger Compliance Controls

Collections require careful handling of communication rules, consent, validation notices, dispute workflows, call documentation, and opt-outs.

According to the Federal Trade Commission’s 2025 report, debt collection remained one of the most reported consumer issues, with 471,142 reports filed against debt collectors. This does not mean every collection effort is risky. However, it does show why businesses need

5. You Want Recovery Without Damaging Customer Relationships

Modern outsourced collections should focus on resolution, not pressure.

Many overdue accounts are tied to confusion, expired cards, insurance delays, billing errors, missed notices, or temporary hardship.

A strong partner helps customers understand the balance, choose a payment option, ask questions, or raise a dispute. For customer-sensitive industries, this distinction matters.

Best Debt Collection Outsourcing Services To Consider

The best debt collection outsourcing service depends on your account volume, industry, compliance needs, customer experience goals, and technology requirements.

Some providers focus on digital collections, whereas some specialize in traditional agency recovery. Others combine collections with BPO, omnichannel engagement, payment portals, and customer service support.

Before reviewing each provider in detail, here is a quick comparison of their best-fit use cases, core strengths, and key considerations.

| Provider | Best Fit | Core Strengths | Consideration |

| First Credit Services (FCS) | Omnichannel collections and customer engagement | First-party, third-party, UCEP, BPO, failed payment recovery, digital portals | Best fit for full-lifecycle managed recovery |

| TrueAccord | Digital-first debt collection | AI, machine learning, digital outreach, self-service payments | More focused on digital recovery |

| IC System | Established agency collections | Long industry experience, traditional agency process, ethical collections | More traditional agency model |

| InDebted | Digital collections at scale | Global reach, cloud-based decisioning, customer-friendly payment plans | Strong fit for high-volume digital portfolios |

Now, let’s explore each service provider in detail.

1. First Credit Services: Best for Omnichannel Debt Collection and Customer Engagement

First Credit Services is an omnichannel debt collection and BPO partner designed to help businesses recover overdue revenue while maintaining customer relationships. It combines first-party collections, third-party collections, digital debt collection, failed payment recovery, portfolio recovery, and customer engagement support into a managed recovery model.

Its Unified Consumer Experience Platform (UCEP) supports digital-first outreach, self-service payments, payment plans, offers, callbacks, and chat through a consumer-facing portal. In first-party mode, the experience can be white-labeled so consumers see the client’s brand instead of FCS.

This unified approach helps businesses move beyond phone-only collections and manage recovery across digital, voice, support, and payment workflows.

Key Strengths:

- Full-lifecycle recovery: Covers early-stage, late-stage, first-party, third-party, failed payment, and portfolio recovery workflows.

- Omnichannel engagement: Uses phone, email, SMS, chat, and digital portals so consumers can respond through the channel they prefer.

- UCEP-powered digital collections: Coordinates outreach, payment journeys, payment plans, offers, callbacks, and chat in one managed engagement model.

- White-label first-party collections: Operates as an extension of your brand for customer-sensitive recovery.

- Third-party collections: Handles formal late-stage recovery when accounts require escalation.

- BPO and customer engagement: Provides call center, customer support, and back-office services for accounts tied to disputes, billing questions, or service issues.

- Compliance-focused operations: Builds recovery around compliant communication, reporting, documentation, and workflow controls.

- Industry coverage: Serves healthcare, financial services, fintech, automotive finance, health and fitness, subscriptions, utilities, and government-related collections.

FCS works best for medium-to-large businesses that need outsourced debt collection services with omnichannel workflows, customer engagement, and operational support.

It is especially relevant when your challenge is not just “we need collections,” but “we need a scalable recovery partner that can protect cash flow and customer relationships.”

Best for: Medium-to-large businesses that need full-lifecycle recovery, omnichannel collections, failed payment recovery, and managed BPO support without adding internal collection headcount.

2. TrueAccord: Best for Digital-First Debt Collection

TrueAccord is a digital-first debt collection company that uses data science, machine learning, and consumer-friendly digital engagement to support recovery. It specializes in personalized outreach, self-service repayment, and compliant digital communication.

Key Strengths:

- Digital-first recovery: Built around digital outreach instead of call-heavy collections.

- AI and machine learning: Uses data-driven workflows to personalize engagement.

- Consumer-friendly experience: Emphasizes flexible, empathetic communication and self-service options.

- Compliance-coded technology: Prioritizes compliance within its technology-led model.

- Omnichannel communication: Supports multiple channels for more flexible engagement.

While TrueAccord is strong for digital-first recovery, it may be less suitable for businesses that need collections plus operational support. Teams that need live-agent staffing, billing issue resolution, complex dispute handling, or back-office follow-up should confirm whether those services are included or require a separate partner.

Best for: Consumer debt portfolios, digital-first recovery teams, fintech lenders, and businesses that want automated, data-driven engagement.

3. IC System: Best for Established Agency Collections

IC System is a long-standing debt collection agency with deep experience in revenue recovery. Its services emphasize ethical, efficient, and consumer-friendly collections for businesses that want an established agency model.

Key Strengths:

- Long industry experience: IC System has operated in debt recovery for decades.

- Traditional agency strength: Strong fit for businesses that want proven third-party collections.

- Consumer-friendly process: Focuses on respectful communication and relationship preservation.

- Flexible programs: Offers collection programs tailored to business needs and account volume.

- Client visibility: Provides reporting and portal access for account activity and recovery tracking.

IC System is a strong option for businesses that want an established agency model. However, teams that rely heavily on SMS, email, self-service payment portals, payment-plan automation, or digital engagement journeys should review how much of that experience is built into the workflow.

Best for: Businesses seeking established agency collections, healthcare collections, government collections, and third-party recovery support.

4. InDebted: Best for Digital Collections at Scale

InDebted is a global digital collections company focused on customer-friendly debt recovery. Its approach brings together digital engagement, data-led decisioning, and self-service repayment options for businesses that want a more modern collections experience.

Key Strengths:

- Global collections infrastructure: Supports recovery across multiple regions.

- Customer-focused collections: Emphasizes flexible, supportive repayment experiences.

- Cloud-based decisioning: Uses data-driven engagement at scale.

- High-volume capability: Its website cites millions of customers supported and 130+ client partners.

- Digital self-service: Customers can manage payment plans and repayment options digitally.

InDebted fits businesses with large consumer portfolios that need scalable digital collections. However, teams that need first-party white-label outreach, voice-led escalation, agent-assisted payment support, or broader customer service coverage should check whether the model matches their recovery process.

Best for: High-volume consumer collections, global recovery teams, fintechs, BNPL providers, and digital-first repayment experiences.

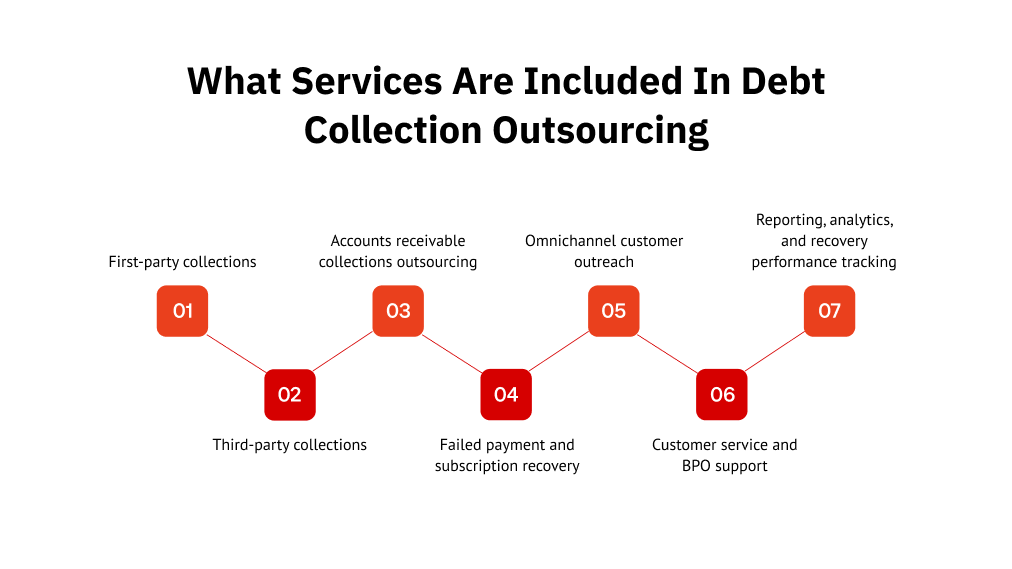

What Services Are Included in Debt Collection Outsourcing?

Debt collection outsourcing can include several service models. The right mix depends on account age, customer relationship, industry, and internal capacity. Here’s what it generally comprises:

1. First-Party Collections

First-party collections are handled as an extension of your brand. Customers typically experience the outreach as coming from your business rather than a separate agency.

This model works well for early-stage overdue accounts, failed payment recovery, subscription recovery, healthcare billing follow-up, financial services outreach, and customer-sensitive recovery.

FCS offers first-party collections for businesses that want early intervention and brand-aligned communication.

2. Third-Party Collections

Third-party collections are usually used for older, more delinquent, or escalated accounts. In this model, the agency contacts customers under its own identity.

This model works best for aged receivables, charged-off accounts, unresponsive customers, escalated debt, and portfolio recovery. For businesses at that stage, FCS can help manage third-party collections with structured outreach, compliance-focused workflows, and account-level reporting.

3. Accounts Receivable Collections Outsourcing

Accounts receivable collections outsourcing covers overdue invoices, unpaid balances, payment reminders, dispute routing, reconciliation support, and AR follow-up.

This is useful when your AR team spends too much time chasing payments instead of managing cash application, forecasting, billing accuracy, and finance operations.

4. Failed Payment and Subscription Recovery

Failed card payments, ACH failures, expired cards, billing errors, and payment authorization issues can create revenue leakage. Subscription businesses can also cause involuntary churn.

Outsourcing helps by creating structured outreach before failed payments become long-term delinquency.

5. Omnichannel Customer Outreach

Modern outsourced collections should not rely solely on phone calls, as customers respond differently based on urgency, account age, channel preference, and payment intent.

FCS’s UCEP-led model connects phone, email, SMS, chat, digital portals, and self-service payment links. Customers can view balances, pay, set up plans, accept offers, schedule callbacks, or start a chat through a personalized portal.

6. Customer Service and BPO Support

Many overdue accounts do not stall because customers refuse to pay. They stall because something in the customer journey is broken, such as a billing error, a failed transaction, an account access issue, an insurance delay, a refund question, or an unclear balance.

That is where debt collection BPO services add value. They connect collections with customer support and back-office resolution, so the partner can remove the blocker behind the missed payment rather than just send another reminder.

Risks Of Outsourcing Debt Collection and How to Reduce Them

Outsourcing can improve recovery, but only if the partner is managed well. The wrong partner can create the following risks:

| Risk | What Can Go Wrong | How to Reduce It |

| Brand damage | Poorly trained collectors frustrate customers | Choose a partner with brand-aligned scripts, QA, and customer-sensitive workflows |

| Compliance exposure | Outreach violates communication or documentation rules | Review training, audits, consent controls, and dispute workflows |

| Poor visibility | Internal teams cannot track account status | Require dashboards, reporting, and account-level transparency |

| Customer friction | Customers feel confused or pressured | Offer self-service portals, payment plans, and clear communication |

| Data issues | Incorrect balances or stale records create disputes | Prioritize secure data transfer and billing-system alignment |

| Misaligned incentives | Partner focuses only on collection volume | Track recovery quality, complaints, disputes, and customer experience |

Outsourcing reduces internal workload, but it also gives an external partner direct influence over customer communication, compliance, and recovery quality. That is why the evaluation should go beyond pricing and recovery promises. Hence, before signing a contract, review:

- Compliance policies

- Sample scripts

- Reporting examples

- Integration process

- Escalation rules

- Complaint handling

- Customer experience standards

- SLAs and performance metrics

- Pricing and fee structure

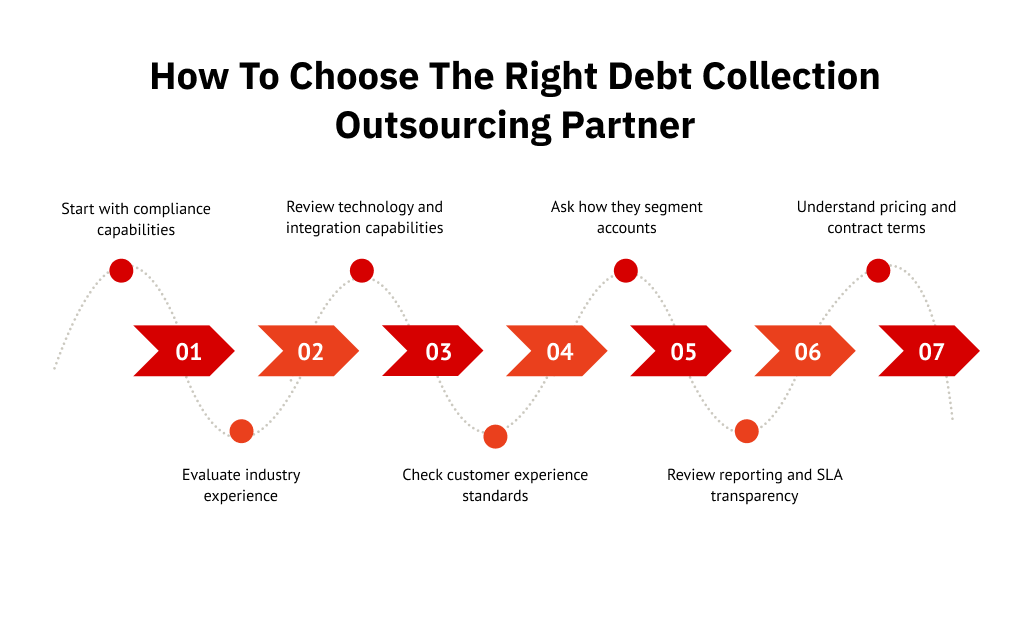

How To Choose the Right Debt Collection Outsourcing Partner

The right outsourced collections agency should match your portfolio, industry, compliance requirements, customer expectations, and internal operating model. Here’s what to consider:

1. Start With Compliance Capabilities

Look for documented controls around the Fair Debt Collection Practices Act (FDCPA), Regulation F, and the Telephone Consumer Protection Act (TCPA). The partner should also understand state licensing, call frequency rules, validation notices, dispute timelines, consent management, SMS opt-outs, call recording, and complaint handling.

Compliance should show up in scripts, workflows, training, channel rules, reporting, and escalation processes.

2. Evaluate Industry Experience

Different industries need different recovery strategies. For example, healthcare collections require sensitive billing conversations and patient-friendly workflows, while fintech collections need fast, compliant digital outreach across high account volumes.

A partner with relevant industry experience will better understand customer behavior, compliance requirements, and account segmentation.

3. Review Technology and Integration Capabilities

Ask how the partner receives account data, updates statuses, processes payments, and reports results. This shows whether their workflow can connect with your existing systems.

Look for CRM and billing integrations, API or SFTP data transfer, payment gateway support, self-service portals, dashboards, secure payments, and account segmentation. Technology matters because collections now depend on timing, channel preference, personalization, and visibility.

4. Check Customer Experience Standards

Ask how the partner handles tone, escalation, payment flexibility, disputes, vulnerable customers, complaints, and brand alignment. A strong partner should explain how they balance recovery goals with customer experience.

5. Ask How They Segment Accounts

Not every overdue account has the same reason, urgency, or recovery path. A 15-day failed payment, a disputed bill, and a charged-off account all need different handling.

Ask how the partner segments accounts by debt age, balance size, payment history, dispute status, previous contact attempts, preferred channel, and likelihood to pay. Good segmentation helps prioritize accounts, reduce unnecessary contact, and match each customer with the right recovery path.

6. Review Reporting and SLA Transparency

Ask for sample dashboards and reports before signing. You should be able to see the recovery rate, contact rate, response rate, payment conversion rate, complaint rate, dispute status, channel performance, and SLA adherence.

Without reporting, outsourcing becomes a black box.

7. Understand Pricing and Contract Terms

Pricing depends on debt age, portfolio volume, average balance, service scope, and staffing needs. Common models include contingency fees, flat fees, per-account fees, hybrid pricing, per-seat BPO pricing, and implementation costs.

Compare cost against recovery quality, compliance controls, reporting transparency, customer experience, and operational support.

Build A Recovery Model That Protects Revenue and Relationships

Debt collection outsourcing is not just a way to move overdue accounts off your team’s plate. It directly affects cash flow, compliance, customer trust, and how quickly your business can recover revenue.

The right partner should help you act earlier, reduce manual follow-up, resolve disputes faster, and give your team clear portfolio visibility. For businesses managing high-volume receivables, FCS brings digital outreach, payment options, customer support, and compliance-focused recovery into one managed model.

If overdue accounts are growing, recovery is slowing, or internal teams are stretched thin, it may be time to move beyond traditional collections. Connect with FCS today to build a smarter, customer-friendly recovery strategy.

FAQs

1. What are debt collection outsourcing services?

Debt collection outsourcing services help businesses recover overdue payments through an external partner. They can include first-party collections, third-party collections, AR follow-up, failed payment recovery, payment plans, reporting, compliance workflows, and customer support.

2. Is outsourcing debt collection worth it?

Outsourcing is worth considering when teams are overloaded, recovery rates are declining, account volumes are rising, or compliance is difficult to manage internally. It helps scale recovery without adding full-time staff.

3. What is the difference between first-party and third-party collections?

First-party collections are handled as an extension of your brand, usually for early-stage accounts. Third-party collections are handled under the agency’s name and are used for later-stage or escalated accounts.

4. How much do outsourced debt collection services cost?

Costs depend on account volume, debt age, average balance, industry, service model, and staffing needs. Common models include contingency fees, flat fees, per-account pricing, hybrid pricing, and per-seat BPO pricing.

5. What should you look for in an outsourced collections agency?

Look for compliance expertise, industry experience, omnichannel outreach, transparent reporting, CRM or billing integration, secure payments, customer-sensitive communication, clear SLAs, and flexible pricing.

6. Can outsourcing debt collection damage customer relationships?

Yes, if the partner uses poor scripts, aggressive outreach, or weak escalation workflows. You can reduce this risk with customer-friendly communication, QA controls, flexible payment options, and complaint tracking.